Comprehensive Guide to Uniform, Gradient, and Geometric Series in Cash Flow Analysis

This guide covers the fundamental concepts of uniform, gradient, and geometric series related to cash flow analysis. It explains key rules and formulas for finding present value (P), future value (F), and annuities (A) in various series scenarios. Learn how to identify gradient series, solve geometric series problems, and apply combination strategies. The content includes practical examples and calculations, ensuring you grasp essential financial science applications for effective financial planning and investment strategies.

Comprehensive Guide to Uniform, Gradient, and Geometric Series in Cash Flow Analysis

E N D

Presentation Transcript

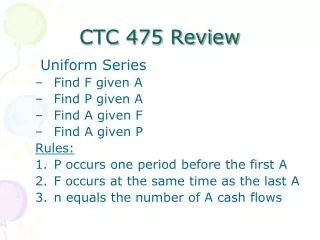

CTC 475 Review Uniform Series • Find F given A • Find P given A • Find A given F • Find A given P Rules: • P occurs one period before the first A • F occurs at the same time as the last A • n equals the number of A cash flows

CTC 475 Gradient Series and Geometric Series

Objectives • Know how to recognize and solve gradient series problems • Know how to recognize and solve geometric series problems

Gradient Series • Cash flows start at zero and vary by a constant amount G

Gradient Series Tools • Find P given G • Find A given G • Converts gradient to uniform • There is no “find F given G” • Find “P/G” and then multiply by “F/P” or • Find “A/G” and then multiply by “F/A”

Gradient Series Rules (differs from uniform/geometric) • P occurs 2 periods before the first G • n = the number of cash flows +1

Find P given G How much must be deposited in an account today at i=10% per year compounded yearly to withdraw $100, $200, $300, and $400 at years 2, 3, 4, and 5, respectively? P=G(P/G10,5)=100(6.862)=$686

Find P given G How much must be deposited in an account today at i=10% per year compounded yearly to withdraw $1000, $1100, $1200, $1300 and $1400 at years 1, 2, 3, 4, and 5, respectively? This is not a pure gradient (doesn’t start at $0) ; however, we could rewrite this cash flow to be a gradient series with G=$100 added to a uniform series with A=$1000

Combinations • Uniform + a gradient series (like previous example) • Uniform – a gradient series

Uniform–Gradient • What deposit must be made into an account paying 8% per yr. if the following withdrawals are made: $800, $700, $600, $500, $400 at years 1, 2, 3, 4, and 5 years respectively. • P=800(P/A8,5)-100(P/G8,5)

Example • What must be deposited into an account paying 6% per yr in order to withdraw $500 one year after the initial deposit and each subsequent withdrawal being $100 greater than the previous withdrawal? 10 withdrawals are planned. • P=$500(P/A6,10)+$100(P/G6,10) • P=$3,680+$2,960 • P=$6,640

Example • An employee deposits $300 into an account paying 6% per year and increases the deposits by $100 per year for 4 more years. How much is in the account immediately after the 5th deposit? • Convert gradient to uniform A=100(A/G6,5)=$188 • Add above to uniform A=$188+$300=$488 • Find F given A F=$488(F/A6,5)=$2,753

Geometric Series Cash flows differ by a constant percentage j. The first cash flow is A1 Notes: j can be positive or negative geometric series are usually easy to identify because there are 2 rates; the growth rate of the account (i) and the growth rate of the cash flows (j)

Tools • Find P given A1, i, and j • Find F given A1, i, and j

Geometric Series Rules • P occurs 1 period before the first A1 • n = the number of cash flows

Geometric Series Equations (i=j) • P=(n*A1) /(1+i) • F=n*A1*(1+i)n-1

Geometric Series Equations (i not equal to j) • P=A1*[(1-((1+j)n*(1+i)-n))/(i-j)] • F=A1*[((1+i)n-(1+j)n)/(i-j)]

Geometric Series Example • How much must be deposited in an account in order to have 30 annual withdrawals, with the size of the withdrawal increasing by 3% and the account paying 5%? The first withdrawal is to be $40,000? • P=A1*[(1-(1+j)n*(1+i)-n)/(i-j)] • A1=$40,000; i=.05; j=.03; n=30 • P=$876,772

Geometric Series Example • An individual deposits $2000 into an account paying 6% yearly. The size of the deposit is increased 5% per year each year. How much will be in the fund immediately after the 40th deposit? • F=A1*[((1+i)n-(1+j)n)/(i-j)] • A1=$2,000; i=.06; j=.05; n=40 • F=$649,146

Next lecture • Changing interest rates • Multiple compounding periods in a year • Effective interest rates