Finance management

Finance management. Finance management. Why do we discuss? Introduction and Objectives Basic finance literacy Budgeting Accounting ,Cost Accounting and Cost Containment Investments Some general tips on day to day matters. Why should we discuss?. Profession vs. Business

Finance management

E N D

Presentation Transcript

Finance management • Why do we discuss? Introduction and Objectives • Basic finance literacy • Budgeting • Accounting ,Cost Accounting and Cost Containment • Investments • Some general tips on day to day matters Satish

Why should we discuss? • Profession vs. Business • Every medical practice, small or big, is a business • Huge investments – expected returns • An entrepreneur- by default • Profit - a dirty word? • Survival and growth • Self employed - look after your own finances and control them • Problems: doctors tend to be ignorant & careless about finances, sitting ducks, frauds Satish

Objectives • To create awareness • To stimulate to further learning • To develop a vision • To develop an ability to plan and control with clinical precision • To equip our selves to ask right questions to CA • To develop a healthy practice with patients as beneficiaries Satish

Financial management – definition • It is the art and science of managing money • The most essential requirement of any organized business or activity • The process of procuring and judicious use of resources with a view to maximize the value of the firm • Interdependence with other areas of management Satish

Basic finance literacy • Income and expenditure statement • Cash flow: outgoing, incoming • Balance sheet: final accounting item (what the practice is worth) • Budgeting: a process of estimation of income and expenditure • Assets • Liabilities • Capital Satish

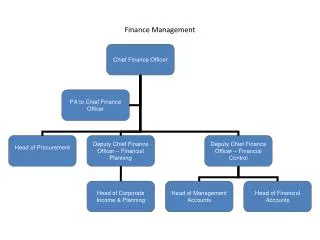

Balance Sheet A statement of assets, liabilities and capital on a given date Assets: • Fixed: land, building, equipments etc • Current: Cash in hand or in bank, stocks, debtors Liabilities • Long term: Loans > 1 yr • Current/ short term: overdraft, taxes Capital= Assets -Liabilities Satish

Some core issues • Budget • Accounting • Cost Accounting • Break even point • Cost benefit analysis • Cost reductions and containment • Day to day activities Satish

Budget • An important instrument of the financial management used as aid in planning, programming and control • A budget may be defined as a financial and quantitative statement, prepared and approved prior to defined period of time, of the policy to be pursued during that period for the purpose of achieving the given objective. Satish

Budget: advantages It is a tool for - • Quantitative expression of the planning • Evaluation of financial performance in accordance with plans • Controlling costs • Optimizing the use of resources • Directing the total efforts in to the most profitable channels Satish

Planning & preparing budget • Well in advance • An opportunity to plan expansion or improving services , hence involve staff and all departments • Plans must be realistic Satish

Types of budget Importance :Understanding of various types of budget can indirectly help us understand various methods of finance management • Project budget : probable expenditure and likely revenue for a specific project • Departmental budget Satish

Types of budget • Operating revenue budget- related to volume of work anticipated • Operating expenditure budget: recurring expenditures for operation and maintenance of services e.g. salaries and wages, supplies, support utilities, maintenance • Capital budget ( non recurrent ): meant for growth ( new facilities), replacement of obsolete. Needs are many – prioritize • Cash budget : provision for anticipated cash expenditures , for planning the cash flow e.g. salaries, bills etc. Satish

Accounting • An art of recording , classifying and summarizing data in a significant manner and interpreting the results • Data may be in form of money transactions and events which are, in part at least , of a financial character Satish

Types of accounting • Financial accounting: documentation of facts, daily transactions • Cost accounting : expenditure for a particular service • Management accounting : Analysis and interpretation of financial information for management purpose Satish

Nomenclature • Costing: to find out money spent on a service • Cost center: an allied group of activities in a hospital eg laboratory, immunization, laundry service • Cost object: anything for which separate measurement of cost is desired e.g. rooms, OT, ICU, equipment • Cost unit: a measurable detail of service rendered e.g. linen, laboratory investigation Satish

Categories of expenditures Important in understanding dynamics of costing • Capital Vs Recurring • Fixed Vs Variable Fixed : Remains unchanged despite changes in related level or volume of activity e.g. salary of permanent staff Variable – volume dependent, varies in proportion to changes in level of activity e.g. medicines, consumables, power cost Satish

3.Direct vs indirect expenditures • Direct : Clearly linked to a service • Indirect: can not be clearly linked to a particular cost object e.g. administration cost,security cost Satish

Objectives & advantages of costing • To get clear picture of financial situation • Identifying profitable and non profitable segments and taking action accordingly • To decide pricing of services and discounts • To decide for out sourcing of services Satish

Advantages of costing • Helps in entering into agreements with TPA, corporate clients etc • Helps in identifying wastages • Helps in budgeting, planning Satish

Effective cost accounting • Proper records • Proper segmentation of costs • Sound accounting practices,regularity • Record of utilization of equipments • Record and analysis of man power utilization Satish

Difficulties in cost accounting • Many inputs have to be considered e.g. labor, material, depreciation, • Every transaction has to carry a price tag • Variation in quality of service e.g. consultant to consultant, patient to patient Satish

Break - even analysis • Volume of activity at which total income just equals total variable and fixed costs • Lower break even point is more desirable e.g. bed occupancy 60% Vs 80% • Advantages: Equipment selection and purchase decision, formulating price policy Satish

Cost - benefit analysis • An economic technique and formalized way of comparing the cost and benefit of undertaking an activity / project Satish

Expenditure - containment and cost - cutting • Sound economic sense • It does not mean compromising quality • Promote awareness amongst staff • Practice cost monitoring: analyze actual expenditure against budget and standards , find reasons for variations, work on them • Cost management: establish systems with responsibility and accountability Satish

4.Strategies for expenditure control • Decrease the cost of inputs relative to outputs: materials, man power • Increase output relative to input: scheduling of procedures, automation , remove bottle - neck in the flow of services Satish

5.Cost saving areas • Streamlining of services e.g. laboratory, OT, indoor • Purchases : planning, budgeting, bargaining, group purchasing • Preventive maintenance AMC’s, back ups • Planning stage: quality manpower and machines, planned recruitment, up gradation • Good accounting practices: automation, internal audit • Energy audit Satish

Investments • We work hard to make money, but learn to make your money work for you • Daily wage earners • Save, invest, build wealth, spend, give it away • Invest some percentage in improving services, facilities • Stagnation without growth Satish

Personal investments • Required for future expansion and growth • Commitment to the financial needs of the family • Retirement planning • Building wealth. Satish

Real Estate Gold and Jewellery Government Securities Company Deposits Mutual Funds Equity ULIP Bank & company FDs Various investment avenues Satish

Some tips on day to day activities 1.Accounting • Financial memory of practice • Matter of self discipline • Meticulous record of financial transactions - legal requirement e.g. Form 3c • Employ accountant - good documentation and reports generation 2. Computerization 3. Periodic meetings with CA Satish

4. Handling cash • Staff handles lot of cash • Doctors are too busy to supervise • Easy temptation • Introduce checks and balances - ensure strict cash control • Cash collection at counter (many advantages ) • Minimize temptation for staff Satish

Tips • Deposit cash in bank daily or twice weekly • Have 2 distinct streams of cash flow Cash inflow deposit daily Cash outflow by withdrawal • Make schedule for making payments • Documentation support for all payments • Filing system: cash memos, paid bills, pending bills • Get personally involved for big transactions Satish

Tips • Reconcile bank statements • Do not allow anyone to take records home • To your staff, demonstrate your awareness about what is going on and that you are careful about money Satish

14.Handling search and seizure • Keep your cool • Call your best friends as witnesses • Know your rights • Prevention is better than cure Satish

Thanks Satish