Download

1 / 10

100 likes | 246 Vues

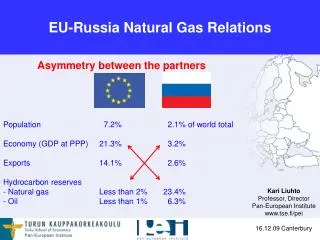

EU-Russia Natural Gas Relations. Asymmetry between the partners Population 7.2% 2.1% of world total Economy (GDP at PPP) 21.3% 3.2% Exports 14.1% 2.6% Hydrocarbon reserves Natural gas Less than 2% 23.4% Oil Less than 1% 6.3%. Kari Liuhto Professor, Director

E N D

EU-Russia Natural Gas Relations • Asymmetry between the partners • Population 7.2% 2.1% of world total • Economy (GDP at PPP) 21.3% 3.2% • Exports 14.1% 2.6% • Hydrocarbon reserves • Natural gas Less than 2% 23.4% • Oil Less than 1% 6.3% Kari Liuhto Professor, Director Pan-European Institute www.tse.fi/pei 16.12.09 Canterbury

Significant growth of EU-Russia trade … but structure remained unchanged 65% energy 40% machinery deficit increased

EU’s energy consumption - 1/5 of EU’s primary energy consumption covered by Russia Russian oil forms 29% of EU’s oil consumption = Russian oilforms 11% of EU’s primary energy consumption Russian gas forms 24% of EU’s gas consumption = Russian gasforms 6-7% of EU’s primary energy consumption Russian uranium forms 19% of EU’s uranium consumption = Russian uraniumforms 3% of EU’s primary energy consumption Source: EU 2009

Russia’s own gas dependency a risk factor Belarus: 69% Ukraine: 41% Poland: 13% !!! Primary energy consumption:refers to the direct use at the source, or supply to users without transformation, of crude energy, that is, energy that has not been subjected to any conversion or transformation process. Source: BP 2009

Share of Russian gas as primary energy consumption in EU members When the Nord Stream runs in full capacity, share of Russian gas in Germany’s PEC approaches that of Finland today Source: Noel 2008

If Russian gas exports to West do not grow, Streams replace some of gas transit via B & U annual capacity 5 bcm 55 bcm ~ 30 bcm EU’s gas consumption ~ 500 bcm EU’s gas imports ~ 300 bcm From Russia ~ 130 bcm LNG imports ~ 1/5 Pipeline gas imports ~ 4/5 (all gas piped from Russia) ~120 +25 bcm ~30-63 bcm 16 bcm Nabucco: ~ 30 bcm

Old fields depleting, new fields delayed, investments down, Russia’s own consumption grows after crisis => Russia’s export capacity ? Arctic fields are huge in size, but also demanding in terms of know-how and finance needs Russia’s own consumption (420 bcm in 2008) 300 bcm in 2020

Can Russia produce enough gas for exports in 2020 ? Conservative calculation Gazprom’s currently operational fields in 2020 300 bcm (500 bcm) - Russia’s own consumption 400-500 bcm - Exports 200-400 bcm ----------------------------------------------------------------------------------------------------------- Gap to be covered - 300-600 bcm + New fields ??? bcm (350-370 bcm) + Central Asian imports 60-??? bcm ( 90 bcm) + Independent producers 100-??? bcm ( 235 bcm) ----------------------------------------------------------------------------------------------------------- There will not be enough gas for everyone ! • Gazprom’s / RAS’ estimate • Roland Götz’ estimate

Some open issues Future of Central Asian gas - Major gas pipeline to China opened in December 2009 Future of Russia-China energy relations Russia’s future gas production - Gazprom’s financial capability to bring Arctic fields alive - More transparency in the field development Role of foreign energy companies in Russia - PSA experience & strategic sector law - Putin’s September statement and Energy Strategy 2030 - Ownership swap deals to increase (bilateralism) Role of LNG in EU (20% of EU’s gas imports -> ?) Role of shale (unconventional) gas in EU Price of gas - Future gas consumption in EU - Future of oil-gas price linkage - Role of GECF in price formulation Kaliningrad’s nuclear power unit

Reset relations with Russia Energy-dominated trade & investment do not build sustainable bridges - promote SME contacts Develop projects of mutual interest - improve Russia’s energy efficiency together Information sometimes limited and biased - support independent EU-Russia think-tanks People-to-people contacts too limited - promote EU-Russia tourism Bilateralism brings only short-term successes - EU should be more than member states’ national interests