Download

1 / 44

440 likes | 573 Vues

May 26, 2011. ESTATE TAX LEGISLATION UPDATE PLANNING AND POSSIBILITIES. The 7 th Annual Dallas CPA Society Education Conference. Michael J. Baldwin R. Thomas Groves, Jr. Sam K. Hildebrand. Introduction. What a decade this has been!

E N D

May 26, 2011 ESTATE TAX LEGISLATION UPDATE PLANNING AND POSSIBILITIES The 7th Annual Dallas CPA Society Education Conference Michael J. Baldwin R. Thomas Groves, Jr. Sam K. Hildebrand

Introduction • What a decade this has been! • TRA 2010 marks a paradigm shift (at least temporarily) • Outline of presentation • Brief overview of TRA 2010 • Effect on Estates of 2010 Decedents • Portability • Planning Ideas and Opportunities

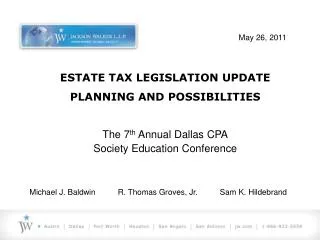

History of Estate Tax 90% $6,000,000 80% $5,000,000 70% $4,000,000 60% Unified Credit Exemption Amount 50% Top Estate Tax Rate $3,000,000 40% 30% $2,000,000 20% $1,000,000 10% 0% $ 0 Repealed - 1802 Re-enacted - 1862 Repealed - 1870 Re-enacted - 1898 Repealed - 1902 Re-enacted - 1916 T/R Increased - 1941 First FET Enacted – 1797 Sunset - 2013 C/B Enacted - 1976 Modified - 1993 Modified - 1997 Modified - 2001 Enacted - 2010 C/B Repealed - 1980 Modified - 1981 January 2011 4

The Economic Growth and Tax Relief Reconciliation Act of 2001 (“EGTRRA”) • EGTRRA basics • Sunset on EGTRRA • 2010, the year to Die

The Tax Relief, Unemployment Insurance Reauthorization, and Job Creation Act of 2010 (“TRA 2010”) • The Baucus Bill • The Great Compromise

Say Hello To The Estate Tax And Goodbye To Carryover Basis! (TRA 2010 – SEC. 301) • Remarkable Legislation • Repeal of the Repeal • End of Carryover Basis • Decedents Dying in 2010 • Extensions to file/pay/disclaim

Essential Terms • Increase in Applicable Exclusion Amount of $5,000,000 • Applicable Exclusion Amount Indexed to Inflation • Maximum Estate Tax Rate Equal to 35% • Reunification of Estate and Gift Tax Exemptions • Generation Skipping Transfer Tax Rate in 2010 • Portability • Two Year Extension

Estate Tax or Modified Carryover Basis? • The Default Regime: Estate Tax and FMV at Death Basis Adjustment Applies for 2010 Decedents • The Elected Regime: Modified Carryover Basis Election for 2010 Decedents

Modified Carryover Basis - Overview • General Rule. Property “acquired from a decedent” has a basis equal to the decedent’s adjusted basis or, if less, the fair market value of the property on the date of the decedent’s death • $1.3 Million Basis Increase

Modified Carryover Basis – Overview (cont.) • Adjustments to $1.3 Million Basis Adjustment • NOLs and Capital Loss Carryovers • IRC Section 165 Losses as if Property Had Been Sold at Decedent’s Death • Non Resident Non Citizen Decedents

Modified Carryover Basis – Overview (cont.) • $3 Million Basis Increase – Qualified Spousal Property • Only Property Owned by Decedent at Death Qualifies for the $1.3 Million and $3 Million Adjustments • Jointly Owned Property • Revocable Trusts • Powers of Appointment • Community Property

Modified Carryover Basis – Overview (cont.) • Property Not Qualifying for Basis Increase • Allocating Basis Increases • On Return Required by IRD §6018 • Revocable Only with Consent of Secretary • Basis Increases Only for “Property “Acquired from the Decedent” • No Basis Increases for IRD • Long Term Gains Holding Period

To Elect or Not to Elect – Factors to be Considered • Will the Election Change the Amounts of the Bequests? • “Easy” Cases • Complicated Cases

To Elect or Not to Elect – Factors to be Considered (cont.) • Example

To Elect or Not to Elect – Factors to be Considered (cont.) • Example (cont.)

To Elect or Not to Elect – Factors to be Considered (cont.) • Executor MUST have a process!!

Time and Manner of Making the Modified Carryover Basis Regime Election and Basis Reporting • Modified Carryover Basis Reporting • Statutory Due Date • Statutory Information Required for Modified Carryover Basis Report • Statutory Information to be Provided to Beneficiaries • Draft Form 8939

Time and Manner of Making the Modified Carryover Basis Regime Election and Basis Reporting (cont.) • TRA 2010 §301(c): election is to be made “at such time and in such manner” as prescribed by the Secretary of the Treasury or his delegate • IRS Guidance to Date

GST and 2010 Decedents • Election of Modified Carryover Basis Regime – 2010 Decedent is Deemed “Transferor” • GST Applicable Tax Rate in 2010 is Zero • 2010 GST Exemption is $5 Million • Election Out of Automatic Allocation for 2010 Direct Skip Transfers

Extensions of Time for File Estate Tax Return, to Pay Estate Tax, to File GST Return, and to Make Disclaimers • Estate Tax – September 19, 2011 • GST Tax - no earlier than September 19, 2011 (but no tax)

Extensions of Time for File Estate Tax Return, to Pay Estate Tax, to File GST Return, and to Make Disclaimers (cont.) • Disclaimers – for decedents dying before December 17, 2010, disclaimers can be made any time until September 19, 2011 • Roadblocks • Acceptance • State Law Time Limitations • Texas Legislation

Portability What would Myth Busters say about it?

Portability(cont.) Three Important Definitions: • “Applicable exclusion amount” is the sum of (a) the basic exclusion amount and (b) for a surviving spouse, the deceased spousal unused exclusion amount (“DSUEA”?). • “Basic exclusion amount” is the estate tax exclusion amount – $5 million, indexed for inflation from 2010, but with no adjustment until 2012. • “Deceased spousal unused exclusion amount” is the lesser of (1) the basic exclusion amount or (2) the basic exclusion amount of the surviving spouse’s last deceased spouse over the combined amount of such deceased spouse’s taxable estate and such deceased spouse’s adjusted table gifts.

Portability(cont.) Example 1 Facts: • Husband 1 has a $1 million taxable estate at his death, which he left to children from a previous marriage. • Wife marries Husband 2. • Husband 2 dies and leaves his $10 million pool cleaning business to his children from a previous relationship, completely using his applicable exclusion amount. • Wife dies owning a taxable estate of $9 million.

Portability(cont.) Example 1 Results: • Wife’s applicable exclusion amount is $5 million, NOT $9 million, because Wife’s last deceased spouse was Husband 2, who had used his applicable exclusion amount. Her estate will be subject to tax on her excess $4 million. • MORAL: DON’T MARRY SOMEONE RICH IF THERE IS A CHANCE THAT HE MIGHT DIE BEFORE YOU (ESPECIALLY IF HE IS LEAVING HIS FORTUNE TO SOMEONE ELSE!)

Portability(cont.) Example 2 Facts: • Husband 1 dies and uses $3 million dollars of application exclusion amount, leaving $2 million of DSUEA to be potentially used by Wife. • Wife marries Husband 2. • Wife dies owning a taxable estate of $3 million (which she leaves to her children from the previous marriage) and having a $7 million applicable exclusion amount. • Husband 2 then dies owning a taxable estate of $9 million.

Portability(cont.) Example 2 Results: • Uncertain. According to the statute, Husband 2 would have an applicable exclusion amount of $7 million (his $5 million and Wife’s $2 million DSUEA) and his estate would owe $700,000 of estate tax. But, the Joint Committee on Taxation would say that his applicable exclusion amount is $9 million and his estate would not owe any estate tax. • MORAL: DON’T TEMP FATE. IF YOU HAVE A LARGE DSUEA, FIND A WAY TO USE IT AS SOON AS POSSIBLE.

Portability(cont.) Is portability important or is it a Trojan horse? • Required estate tax return for deceased spouse required • No protection from creditors of transferred assets • Loss of control over ultimate disposition of property • Loss of protection from estate tax of income and appreciation • Loss of ability to allocate GST exemption • But, transferred assets do get income tax basis adjustment on spouse’s death

Planning Ideas and Opportunities Let the giving begin!

Planning Ideas and Opportunities(cont.) • A $5 million gift tax exemption? That’s great! • But, two important drawbacks: • Loss of income tax basis adjustment • Potential recapture or claw back

Opportunity or Trap – Recapture/Clawback • Source of the Issue • Computation of Estate Tax and Adjusted Taxable Gifts • Form 706, Part 2, Line 4 • Potential Problems with Clawback • Estate Passes to Spouse or Charity • Insufficient Assets to Pay Tax • Implications Regarding Portability • Conflicts Among Beneficiaries

Opportunity or Trap – Recapture/Clawback (cont.) • Does Clawback Apply? • Gift Planning in Light of Clawback • No Worse Position with Respect to Estate Tax Amount • Benefits of Gifts Notwithstanding Clawback • Possible Permanence or Extension of $5 Million Estate Tax Exemption • Tax “Apportionment”/ Net Gifts

Planning Ideas and Opportunities(cont.) • Three ways to use the $5 million gift tax exclusion, with no forced leaks back • The Dynasty Trust • The Exclusion Trust for Spouse • The Self Settled Trust

Planning Ideas and Opportunities(cont.) • Supercharge the gift • With valuation discounts • We all know about valuation discounts • Minority interests in closely held businesses • Limited partner interests • Fractional interests in real property • The surprise – we still can use them! • With grantor trusts • Creates a tax free environment for the gifted property • Sometimes difficult to convince the client to pay tax without the income

Planning Ideas and Opportunities(cont.) • Three leaky tools to consider • Sales to Grantor Trusts • Grantor Retained Annuity Trusts • Qualified Personal Residence Trusts

Planning Ideas and Opportunities (cont.) Sale to Grantor Trust • Grantor gives seed funds Goal: If transferred asset appreciates at a greater rate than the promissory note interest rate, Grantor succeeds in passing assets to beneficiary at no gift tax cost. GRANTOR GRANTOR TRUST (2) Grantor sells appreciating asset to grantor trust in exchange for low interest bearing promissory note

Planning Ideas and Opportunities (cont.) Grantor Retained Annuity Trust GRANTOR GRANTOR RETAINED ANNUITY TRUST Goal: If the transferred asset appreciates at a rate greater than the Section 7520 rate, Grantor succeeds in passing assets to beneficiary at no gift tax cost. (1) Grantor transfers appreciating assets to GRAT in exchange for an annuity payment over a set term

Planning Ideas and Opportunities (cont.) Qualified Personal Residence Trust GRANTOR GRANTOR PERSONAL RESIDENCE TRUST Goal: Transfer home at fraction of its value and reduce Grantor’s estate further by grantor paying rent. • Grantor transfers home to QPRT in exchange for right to occupy for a set term • After set term, grantor pays rent for right to occupy

Planning Ideas and Opportunities(cont.) • Life Insurance Planning • Should life insurance trusts be terminated? • Should life insurance trusts continue and funding accelerated?

Planning Ideas and Opportunities(cont.) • Charitable Planning • IRA Charitable Rollover Extended • Conservation Easements - favorable tax treatment extended • CLATs – still a great time to create CLATs

Planning Ideas and Opportunities(cont.) • Wills and Revocable Trusts • Every will and revocable trust should be reviewed. • The issues with formula clauses • Income tax basis issues • The need for flexibility • Powers of appointment • Trust protectors