Assessing CB's Liability: Audit Standards, Tax Advice, and Financial Misstatements

This comprehensive analysis evaluates CB’s liability concerning audited financial statements and tax advice to GEL. Key areas of focus include material misstatements, compliance with GAAS, and the accuracy of cash flow forecasts. By assessing professional standards, including due care and audit opinions, we will identify and prioritize accounting issues, and quantifying necessary adjustments. The legal implications based on the findings and the adequacy of conducted work will be thoroughly explored to conclude whether CB is liable and whether standards were met, including risk assessment and audit approach employed.

Assessing CB's Liability: Audit Standards, Tax Advice, and Financial Misstatements

E N D

Presentation Transcript

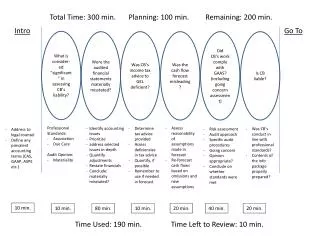

Total Time: 300 min. Planning: 100 min. Remaining: 200 min. Intro Go To What is consider-ed “significant” in assessing CB’s liability? Were the audited financial statements materially misstated? Was CB’s income tax advice to GEL deficient? Was the cash flow forecast misleading? Did CB’s work comply with GAAS? (including going concern assessment) Is CB liable? • Professional Standards: • Association • Due Care • Audit Opinion: • Materiality • Assess reasonability of assumptions made in forecast • Re-forecast cash flows based on omissions and new assumptions • Identify accounting issues • Prioritize • address selected issues in-depth • Quantify adjustments • Restate financials • Conclude: materially misstated? • Determine tax advice provided • Assess deficiencies in tax advice • Quantify, if possible • Remember to use if needed in forecast • Was CB’s conduct in line with professional standards? • Contents of the info package properly prepared? • Risk assessment • Audit approach • Specific audit procedures • Going concern • Opinion appropriate? • Conclude on whether standards were met • Address to legal counsel • Define any prevalent accounting terms (CAS, GAAP, ASPE etc.) 10 min. 10 min. 80 min. 10 min. 20 min. 40 min. 20 min. Time Used: 190 min. Time Left to Review: 10 min.