Chapter 10 Swaps

FIXED-INCOME SECURITIES. Chapter 10 Swaps. Outline. Terminology Convention Quotation Uses of Swaps Pricing of Swaps Non Plain Vanilla Swaps. Terminology Definition. Agreement between two parties They exchange interest payments Computed on a “notional” principal

Chapter 10 Swaps

E N D

Presentation Transcript

FIXED-INCOME SECURITIES Chapter 10 Swaps

Outline • Terminology • Convention • Quotation • Uses of Swaps • Pricing of Swaps • Non Plain Vanilla Swaps

TerminologyDefinition • Agreement between two parties • They exchange interest payments • Computed on a “notional” principal • Principal is not exchanged • Classic swap • One side pays a fixed rate • Counterpart pays floating rate • Floating rate is usually Libor • Rate is reset at every payment date

TerminologyStandard Swaps • Plain vanilla contracts • Exchanging a fixed leg whose payments depend on a fixed rate for a floating leg whose payments depends on a floating rate … • … in which the notional principal remains constant throughout the life of the contract … • … and where the maturity of the variable-rate index is identical to the payment frequency of the floating-leg flows.

07/01/01 01/01/02 07/01/02 01/01/03 100,000*F 100,000*F -100,000*E(01/01/01) -100,000*E(07/01/01) -100,000*E(01/01/02) -100,000*E(07/01/02) TerminologyExample • Example • Current date: 01/01/01 • 6-months Euribor swap with 2 years maturity, fixed rate F and notional amount 100,000 euros • Schedule of payments • where E(t) is the 6 months Euribor rate at month t payed at month t+6

ConventionBuyer and Seller • Every 6 months, and prorated for the period, the borrower • Receives the 6-month Euribor observed 6 months earlier multiplied by the notional • Pays a fixed rate F every year multiplied by the notional • In this example, the swap is structured so that the buyer receives the floating leg and pay the fixed leg • Of course, the opposite swap may be structured in which the buyer receives the fixed leg and pays the floating leg

ConventionPrincipal Amount • Principal amount • A swap is composed of two legs a fixed leg whose payments depends on a fixed rate and a floating leg whose payments depends on a floating rate • The notional, or principal, amount allows one to calculate the exact amount of the different payments on the two legs of the swap • Example • Consider a 3-year swap exchanging the 1-year Libor for the fixed 5% • The notional principal is $10 million • Payments on the two legs are annual • Then each year, the amount paid on the fixed leg is equal to 5%x10 million = $500,000 • The amount received on the floating leg is the 1-year Libor multiplied by $10 million

ConventionRates • Maturity date: date of termination of the swap contract • Frequency • Payments on the fixed-leg take place either annually or semi-annually (e.g., in the US) • Payments on the floating leg match the maturity of the reference rate (e.g., 4 times a year if the reference rate is a 3 months rate) • Rate and payments • The floating rate for each period is fixed at the start of the period • The first interest payment of the swap is known in advance by both parties • Note that even if both parties pay and receive interest payments, at a payment date only the net difference between the two interest payments change hands

Pricing of SwapsBasic Principles • Exchange of a fixed-rate (F) for a floating-rate (V) security • Initially, both have the same value • Otherwise it would not be a fair deal • Later on, prices can differ depending on the evolution of the term structure • Fixed-rate notes have longer duration => a rise in interest rates tends to lower the value of the fixed-leg more than that of the variable leg • This raises the value of the swap to the buyer and lowers the value of the swap to the seller • Value of the swap (party that pays fixed):

Pricing of SwapsPricing the Fixed Leg • We assume no risk of default and perfect knowledge of the term structure • Value of F: present value of future payments (discounted at the spot rate) • Problem with V: we know next payment but payments after that are unknown • Trick: those payments will be at the prevailing market rate

Pricing of Swaps Pricing the Floating Leg • We assume that the notional is also exchanged • Then, the floating will pay notional plus market rate • The present value of notional plus market rate is: => Notional • The price of a floating rate note on each and every coupon date is equal to par

Pricing of Swaps Example • Today is 1/1: remaining life of 9 months • Receives 10% a year • Semiannually paid coupons • On 3/31 and 9/30 • Pays 6-month LIBOR • Notional principal of $1,000 • Next payment based on LIBOR at 6% • Term structure • r3m = 5% • r9m = 7%

Pricing of Swaps Example (continued) • Fixed: • Floating: • Value: 1047.44 - 1017.51 = 29.93

QuotationSwap Rate • For a given maturity, the convention for Quotes in the market is for the swap market maker to set the floating leg at Libor and then quote the fixed rate, called the swap rate, that makes the value of the swap equal to zero • The swap rate is then the value of the fixed rate that makes the swap's fixed leg equal to its floating leg because the value of the swap is very simply the difference between the sum of the discounted cash-flows of one leg and the sum of the discounted cash-flows of the other leg (see above)

QuotationExample • Example • Consider a seven year 3-month Libor swap quoted by a market maker • Floating-rate payer: pays 3-month Libor and receives fixed rate of 6% • Fixed-rate payer: pays fixed rate of 6.05% and receive 3-month Libor • The bid price quoted by the market maker is 6% to pay the fixed-rate and the ask price to receive the fixed rate is 6.05%

QuotationSwap Spread • A swap is also quoted as a swap spread • The swap spread of a swap with a given maturity is equal to the difference between the fixed rate of the swap and the benchmark treasury bond yield of the same maturity • It is expressed as a number of basis points • Example: a seven year 3-month Libor swap • A market maker quotes 45-50 • Means that he is willing to enter a swap paying fixed 45 points above the seven-year benchmark bond yield and receiving the Libor • And receiving fixed 50 basis points above the seven-year bond yield and paying the Libor

Uses of SwapsMotivation • Swaps may be used to • (1) Optimize the financial conditions of a debt • (2) Convert the financial conditions of a debt • (3) Create new synthetic assets • (4) Hedge a bond or another fixed-income security against any change of the yield curve • (1) and (3) are discussed below • (4) is related to dynamic hedging • (2) To finance their needs • Most of the firms issue long-term maturity fixed bonds because of the large liquidity of these bonds • A treasurer may anticipate a decrease of rates and wish to transform its debt at a fixed rate into a floating-rate debt to take profit of the future decrease of rates • Enter a swap in which the firm will pay the floating and receives the fixed

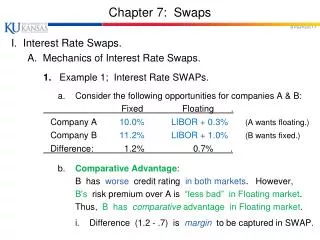

Uses of Swaps (1): Comparative Advantage • A would prefer floating and B fixed • A has “comparative advantage” at fixed • 200 basis points better than B for fixed • 50 basis points better than B for floating • A borrows at fixed and B at floating • They enter a swap

Uses of Swaps Comparative Advantage (Cont’) • Terms of the swap • A will pay 6-month Libor • B will pay 8% • After the swap • A pays: Libor + 8% - 8% = Libor • B pays: 8% + Libor + 1% - Libor = 9% • Advantage • A saves 50 basis points (pays Libor instead of Libor +.5%) • B saves 100 basis points (pays 9% instead of 10%) • Other agreements are possible

Uses of Swaps (3):Create New Assets • Swaps may be used to create new assets that do not exist in the market • The transaction is called an asset swap • Example • A firm with a rating BBB has issued bonds with a 10% fixed coupon and maturity 4 years • An investor likes the coupon paid by this firm but in the same time anticipates a rise of short-term rates • May create a synthetic bond of this firm that delivers a 1-year Libor coupon plus a margin • For that, buy the 10% fixed coupon bond with maturity 4 years and enter a swap where the investor receives 1-year Libor and pays the fixed • Assume the swap rate for such a swap quoted by the market is 6% (default-free rate) • The synthetic bond delivers 1-year Libor + 4%

Uses of Swaps Institutional Aspects • Value: over 17 trillion • Very efficient market with low spreads • Mostly commercial banks • Mostly unregulated • No secondary market • Need the counterpart to close • Risk of default is asymmetric