12.15 Track B Issuer Presentation

230 likes | 327 Vues

12.15 Track B Issuer Presentation. The HiTo model. Table of content. Introduction The HiTo Model Tap Issuances The Balance Principle Standardization Risk Management Conclusion. Introduction. Background: 2001 the “Partnership for Prosperity” agreement between Mexico and the US.

12.15 Track B Issuer Presentation

E N D

Presentation Transcript

Table of content • Introduction • The HiTo Model • Tap Issuances • The Balance Principle • Standardization • Risk Management • Conclusion

Introduction • Background: • 2001 the “Partnership for Prosperity” agreement between Mexico and the US. • 2004 Soros and VP created Absalon to introduce the Danish system to Mexico. • In 2006 HiTo S.A.P.I. de C.V. was created. • Mission: • HiTo is a private entity providing intermediary services to financial institutions in Mexico active in the origination and servicing of high quality residential mortgage loans, with the objective to make housing affordable and available for all Mexicans. • Shareholders: • Geomex Investor • Hipothecaria Crédito y Casa • Sociedad Hipothecaria Federal • FMO • Autonomy Capital • INVEX • Hipotecaria Vertice • Condesa Financiera

The HiTo model • HiTo’s service • HiTo will offer a securitization service based on the Danish Mortgage System. • The HiTo Model relies on three pillars: (i) Tap Issuances (ii) The Balance Principle (iii) Standardization • Who will benefit from this model? • Borrowers. • Lenders. • Investors. • The Economy.

Tap Issuances • Tap Issuances • Tap issuances allow for the securitization of a mortgage five days after it is originated. • Each mortgage is directly funded with bonds of similar tenor, amortization schedule and interest rate profile. • Each individual bond has a nominal value of MX$10.00 and has a callable bullet structure. • Amortization is done by drawing bonds in stead of amortizing the nominal value. • Bond series are tapped weekly for a three year cycle. • Program • HiTo will establish different programs for different products; i.e. a 2030 final maturity 8% coupon, a 2025 final maturity 7% coupon etc. • Each program is set for a certain amount and initially all bonds are kept in the treasury account of the trust. • The bonds will be gradually issued to investors during weekly issuances to finance individual mortgages according to predefined eligibility criteria and risk metrics.

Tap Issuances • Market Risk • Tap issuances eliminate the need for warehousing and thereby eliminate the market risk. • MCIs only need five days of working capital, and could deploy their equity more efficiently. • The elimination of market risk will lead to a significant reduction in required economic capital under BASEL regulations.

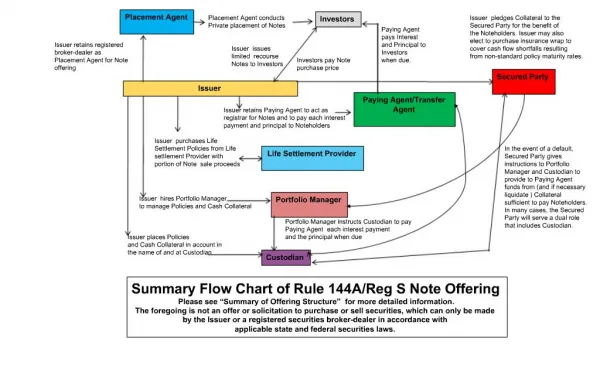

HITO Capital Center Own brand HiTo Brand Layer 1 trust Layer 2 trust Layer 2 trust Layer 1 trust Layer 2 trust Layer 2 trust Layer 1 trust Layer 2 trust Layer 2 trust The HiTo securitization process 3. Creates private and public bonds 2. Transfers mortgage 4. Public bond registration BMV/CNBV MCI Indeval 1. Accepts mortgage Capital market 5. Sale of bonds according to FPA Debtor MCI HITO 6. Transfer of funds

The Balance Principle • Balance Principle • The balance principle matches the assets and liabilities of the borrower with regard to duration and sensitivity to interest rate changes. • Home owners have the option to prepay their mortgage in cash or bonds. • When interest rates drop, prepayment in cash results in a lower monthly payment and same outstanding loan amount. • When interest rates rise, prepayment with bonds results in a lower outstanding loan amount and same monthly payments. • Credit Risk • The Balance Principle strongly reduces the credit risk. • In a normal economic cycle the LTV decreases faster. • In a crisis it preserves the equity of the homeowner.

Normal Economic cycle • The upper line (pink) curve reflects the value of a mortgage backed bond given a simulated fluctuating interest rate pattern. • When interest rates fall mortgages are prepaid in cash and refinanced at a lower rate (circles). • When interest rates rise (arrows) HiTo mortgages are prepaid with bonds. • This reduces the outstanding amount, and thereby the LTV faster than for a traditional level payment mortgage.

Crisis Before “Crisis” After “Crisis” 100% LTV: 90% LTV: 90% 90% 90% 86% LTV: 141% 61% 52% LTV: 86% Loan Value House Value Bond Value Loan Value House Value Bond Value

Standardization • Standardization • HiTo transforms mortgages into standardized AAA rated bonds and MCI specific mezzanine bonds using a two-layer trust structure. • In the first layer trust the credit risk is separated from the market risk. • The first layer trust holds the mortgages and issues private bonds, the second layer trust holds the private bonds and issues public bonds. • The private bonds can either be transferred to Own Brand second layer trusts, or to HiTo Brand joined trusts. • The MCI specific mezzanine bonds bear the credit risk and could, at the sole discretion of the MCI, (i) be issued directly as mezzanine bonds in the market, (ii) be guaranteed and issued as AAA bonds in the market, (iii) be sold in a private transaction, or (iv) held by the MCI. • Liquidity • Standardization will lead to a reduction in investor research costs. • The joining of private bonds will increase the size of bond series. • This will increase liquidity and reduce the costs.

Two layer trust structure MCI First layer Trust Second layer Trust Investor 1 Mortgage Mortgage Private Bond Private Bond Public Bond Public Bond Cetes Mezzanine Investor 2 Mezzanine Cash Equity MCI Credit Risk Equity Equity Market Risk Risk Free

Own Brand A Capital Center A Capital Center C Capital Center D Capital Center B Layer 2 trust 1 Layer 2 trust 1 Layer 1 trust 1 Layer 1 trust 1 Layer 1 trust 1 Layer 1 trust 1 Layer 1 trust 2 Layer 2 trust 2 Layer 2 trust 2 Layer 1 trust 2 Layer 1 trust 2 Layer 1 trust 2 Layer 2 trust 3 Layer 1 trust 3 Layer 2 trust 3 Layer 1 trust 3 Layer 1 trust 3 Layer 1 trust 3 Layer 1 trust 4 Layer 2 trust 4 Layer 2 trust 4 Layer 1 trust 4 Layer 1 trust 4 Layer 1 trust 4 HiTo Brand Two layer trust structure HiTo 1st layer; issuing private bonds HiTo 2nd layer; issuing public bonds INVESTORS

Capital Centers CAPITAL CENTER 1st layer Trust 1 1st layer Trust 2 Residual flow center Cash Equity Mortgage Private Bond 1 Mortgage Private Bond 2 Cetes Mezzanine 1 Cetes Mezzanine 2 Cash Equity Cash Equity

Risk Management • Credit quality • The quality of the borrower (PD). • The value of the underlying mortgage (LGD). • The quality of the borrower • Loan-to-Income ratio; a higher LTI, means a higher risk. • Credit history; • Other financial obligations of the borrower. • The quality of the borrower determines the probability-of-default (PD). • The value of the underlying mortgage • The Loan-to-Value ratio; a higher LTV, means a higher risk. • The foreclosure regulations; a longer foreclosure procedure, means a lower value of the mortgage and a higher risk. • Quality and reliability of appraisal value and loan files. • The value of the underlying mortgage determines the loss-given-default (LGD). • Capital requirements according to BASEL II • (K) = LGD × N[(1 – R)^-0.5 × G(PD) + (R / (1 – R))^0.5 × G(0.999)]– PD x LGD

Expected and unexpected loss • The product of PD and LGD provides the Expected Loss (EL) which should be covered by Reserves and the credit margin. • The variance of the EL provides an estimate of the Unexpected Loss for a certain security interval, this should be covered by the Economic Capital (mezzanine + equity). Expected loss Unexpected loss AA AA+ AAA Marginal probability μ + 1σ μ + 2σ μ + 3σ Loss

Economic Capital and Margin • Risk based pricing • At the time of origination a credit score is being generated for each individual mortgage • This credit score provides the level of: • Equity • Mezzanine • Total Economic Capital • The minimum required margin • The HiTo rating will be calibrated with rating Agencies requirements

Dynamic scoring • Borrower score • Update based on payment behavior. • Update based on credit bureau score. • Adjust probability of default. • The value of the mortgage • Update based on amortization. • Updated based on price changes. • Adjust loss-given-default. • Economic Capital • Adjust the level of economic capital based on the above scores. • Adjust this level prior to the occurrence of a default.

Benefits • Borrower: • Fast and transparent origination process. • Protection of equity and lower mortgage costs. • Lender: • Elimination of market risk and a reduction of credit risk. • Reduced operational costs and risk costs. • Increased return on equity. • Investor: • Supply of large, liquid and standardized securities. • Economy: • Domestic savings invested in domestics assets. • Implied crisis protection.

Conclusion • Tap Issuances: • Tap issuances eliminate market risk. • Tap issuances increase the turn over of and return on equity. • Balance Principle: • The probability of default and loss given default is lower for HiTo Loans. • Therefore, HiTo loans have a lower risk profile than a normal loan because of the prepayment option with bonds. • Standardization: • Standardization will lead to a reduction in investor research costs and higher acceptance and demand. • Separation of credit risk and market risk in the first layer trust allow for the joined issuances of AAA rated bonds. • Large bond series will lead to a reduction of the liquidity premium and lower costs.