Download

1 / 18

180 likes | 322 Vues

Integrating Budgetary and Financial Reporting in a Unified Chart of Accounts (UCoA). Mark Silins, PFM Advisor Moscow, Russian Federation Treasury Community of Practice 25 October 2019. Unified Chart of Accounts Underpins Interoperability across all PFM systems. Budget Preparation.

E N D

Integrating Budgetary and Financial Reporting in a Unified Chart of Accounts (UCoA) Mark Silins, PFM Advisor Moscow, Russian Federation Treasury Community of Practice 25 October 2019

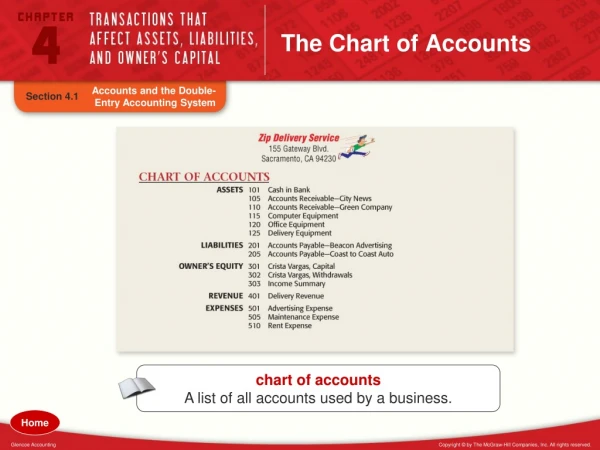

Unified Chart of Accounts Underpins Interoperability across all PFM systems Budget Preparation E-Procurement FMIS Debt Management Banking System MDA Accounting Systems Cash Management Revenue Management Systems Data Warehouse (Reporting) Unified Chart of Accounts (ensures data integrity across PFM systems)

Cashflow – A common approach for budgetary reporting (GFSM 86) Approach • Recurrent Revenues • Capital Revenues • New borrowing • Grants • Sale of non-financial and financial assets • Recurrent Spending (including debt interest) • Capital Expenditures • Debt principal • Acquisition of non-financial and financial assets Receipts Expenditures Receipts Less Expenditures Cash based budgetary balance

Even a cash based budget also directly impacts a government’s balance sheet and net worth • Classifying flows correctly according to the economic nature is the first step • This is why a structure which accords with generally accepted accounting concepts is so important • Next add specific stocks as capacity allows • This requires that you devise the segment to accommodate the additional elements in the future • Ensure that you devise the economic segment to allow detailed reporting across all your accounting requirements Cash Modified cash Modified accrual Full accrual Increasing comprehensiveness of reporting, budget, financial, statistical and macrofisal Cash-only balance sheet Cash plus Payment liabilities Full balance sheet less Physical assets Full balance sheet

The convergence of Budget, Financial, Statistical and Macrofiscal Reporting using a GFSM2014 Structure • This structure supports: • a well formulated budget • It allows daily monitoring of the fiscal position • It supports cashflow management and forecasting • It supports statistical reporting • It supports IPSAS cash and accrual and modified accrual • The use of general accounting concepts as a (GFSM 2014) structure is logical and comprehensive for economic management and reporting Revenues Expenses- Recurrent Spending Non Financial Assets – Capital Spending Financial Assets – Financing of the budget Liabilities- Financing of the budget Equity/Net Assets

Relationship between a Cash-Based Budget Classificationand Economic Chart of Accounts Using accounting concepts for the template ofthe economic structure • The BC is usually comprised of elements of various segments of the CoA (administrative, program, economic) Economic Accrual based CoA Cash based budget classification Source of Funds Organization Project Location Program Function Cash based budget Classification • The economic segment may contain accrual concepts which includes cash. The economic nature of transactions do not change under cash or accrual accounting – the difference is generally a timing issue • Budgets always indicate at least the following: revenues, recurrent expenditures, capital expenditures and financing sources e.g. financial assets and liabilities Accrual based CoA

The Elements – Budgetary Reporting and Cashflow Statement (IPSAS 2) For cash financial assets only Yes if contingent liabilities included in the budget Receipts Reporting Expenditure Reporting

The Elements – Modified Accrual and Macrofiscal Reporting For modified balance sheet only Yes if contingent liabilities included in the budget Expenditure Reporting Receipts Reporting

The Elements – Full Accrual And Statistical Reporting For Entire Balancesheet Yes for all off balance reporting and disclosures Receipts Reporting Expenditure Reporting

How to create an Integrated Segment? • GFSM Approach • Croatian Approach • PULSAR Approach • General Accounting Approach

GFSM Approach – Balancesheet Non-Financial Asset Account Sub-account Approach Class Approach

Moldovan Approach – Sub-accounts in Assets and Liabilities Sale of buildings

General Accounting Approach The challenge here is ensuring that the final cash transactions are recorded directly (not indirectly) against the cash based budgetary appropriations – this is a major reason countries choose one of the other approaches

Budgetary Cashflow Reporting The accounting issue is that the cashflow does not occur directly against the budget accounts under accrual. However, every properly designed FMIS should be able to report as per the table below, which requires direct, not indirect reporting

Benefits of the New Economic Segment • All of the examples provide the opportunity to record the various elements of transactions separately for the different reporting requirements • The goal should be to minimize the different structural requirements while still meeting these requirements • A big issue is getting all parties to understand that they are just a part of a bigger picture and the PFM reporting framework – this issue often results in a narrow view on reporting which trends to exclude other requirements and impose unnecessary duplication on the CoA and other reporting structures • However an integrated economic segment for a UCOA: • uses a single structure for entity financial reporting, state budget reporting and final accounts, economic reporting for the macro-fiscal reporting and for statistical reporting • Supports cash, modified cash, modified accrual or full accrual reporting • aligns government reporting with private sector reporting which will facilitate better ability to track exchanges between the two sectors • Decision makers will always see the same general structure in use across all types of reporting reducing confusion and enhancing understanding • Entities will only need to record transactions once in their own system – and this can be passed electronically to FMIS (if different MDA systems exist).