Download

1 / 6

110 likes | 136 Vues

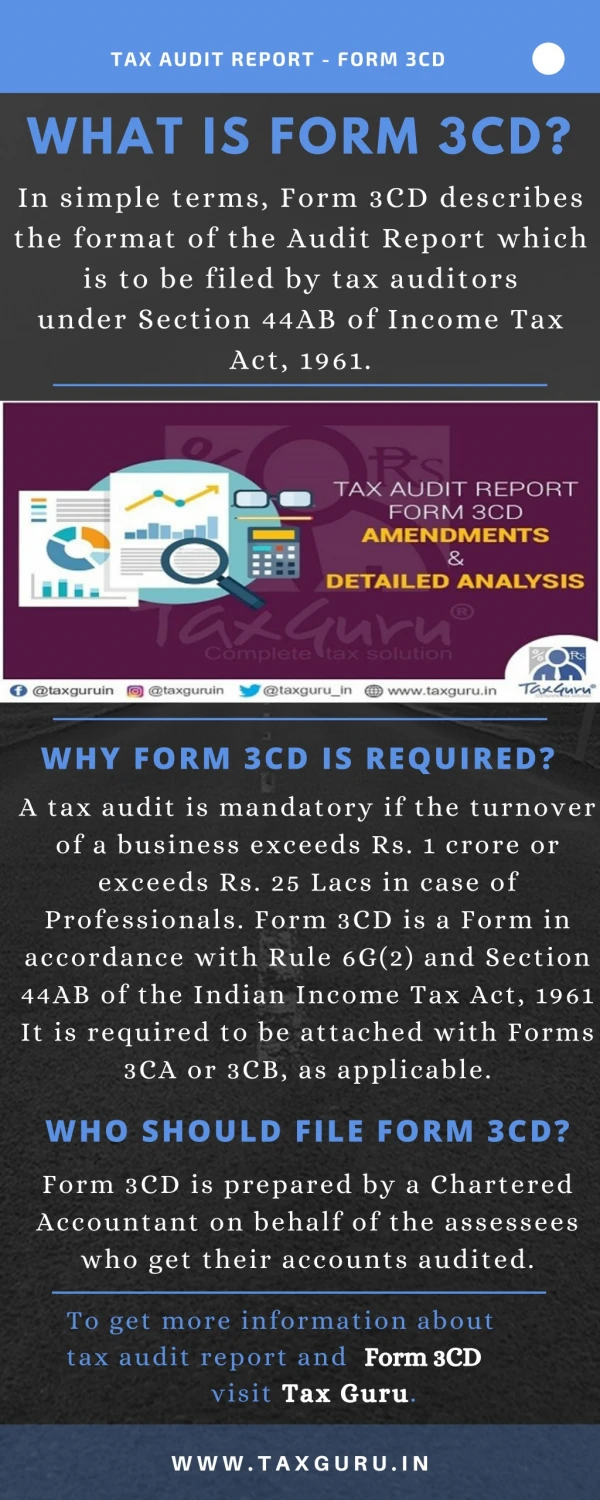

"Dear Friends The Clause 44 of the Form 3CD is effective for Assessment Year 2022u201323 i.e. for the Financial Year 2021u201322 because the compliance of this clause wa"<br>TaxGuru is a platform that provides Updates On Amendments in Income Tax, Wealth Tax, Company Law, Service Tax, RBI, Custom Duty, Corporate Lawu00a0, Goods and Service Tax etc.<br>To know more visit https://taxguru.in/income-tax/illustrative-clause-44-form-3cd-applicable-financial-year-2021-22.html

E N D

ILLUSTRATIVE CLAUSE 44 OF FORM 3CD APPLICABLE FOR FINANCIAL YEAR 2021-22 AUTHOR :CA SUDHIR HALAKHANDI https://taxguru.in/income-tax/illustrative-clause-44-form-3cd-applicable-financial-year-2021-22.html Dear Friends The Clause 44 of the Form 3CD is effective for Assessment Year 2022-23 i.e. for the Financial Year 2021-22 because the compliance of this clause was kept in abeyance till 31/03/2022 but for all the reports submitted after that date the clause is mandatory. Since the audits for the Financial Year 2021-22 are under process hence we should study how to report and comply this clause and how the Assesssee under audit will submit the data under this clause. The primary duty of submission of the details is of Auditee and for verification of the information supplied under this clause can be verified form the GSTR-2A, GSTR-2B, AIS and other records available with the dealer. Most of the information required for this clause is already available with the Law makers in the form of GSTR- 2A and AIS and what is the use of this information in Form 3CD is better known to the lawmakers but since the clause is there hence the Assesssee and Auditor has to follow and comply it. Let us see an Example with certain notes: –

S.NO. Total Amount of Expenditure incurred during the year Expenditure in respect of entities registered under GST Expenditure relating to entities not registered under GST Relating to Goods or Services exempt form GST Relating to the Entities falling under Compositions Scheme Relating to other Registered Entities Total Payments to Registered Entities (1) (2) (3) (4) (5) (6) (7) 1. 22355475.00 199660.00 177040.00 19488780.00 19865480.00 2489995.00 WORKING AND CALCULATION TRADING AND PROFIT AND LOSS ACCOUNT FOR THE YEAR ENDING ON 31-3-2022 PARTICULARS Opening Stock Purchases Gross Profit Total AMOUNT 720000.00 19676875.00 2793125.00 23190000.00 PARTICUALS Sales Closing Stock AMOUNT 22345000.00 845000.00 Total 23190000.00 Salary Travelling Office Expenses Repair and Maintenance Interest Local Conveyance Festival Expenses Commission Business Promotion Depreciation Net Profit 555000.00 234500.00 365600.00 117600.00 305600.00 34500.00 132400.00 75000.00 123400.00 76560.00 772965.00 Gross Profit 2793125.00

Total 2793125.00 Total 2793125.00

CALCULATION FOR PRESENTATION IN CLAUSE 44 OF FORM 3CD Total Amount of Expenditure incurred during the year Expenditure relating to entities not registered under GST S.NO. Expenditure in respect of entities registered under GST Relating to Goods or Services exempt form GSTRelating to the Entities falling under Relating to other Registered Entities Total Payments to Registered Entities Compositions Scheme (1) (2) (3) (4) (5) (6) (7) Purchases 19676875.00 0.00 120340.00 18456000.00 18576340.00 1100535.00 Salary 555000.00 0.00 0.00 0.00 0.00 555000.00 Travelling & Petrol Expenses 234500.00 176500.00 0.00 0.00 176500.00 58000.00 Office Expenses 365600.00 5600.00 56700.00 75600.00 137900.00 227700.00 Repair and Maintenance 117600.00 0.00 0.00 45780.00 45780.00 71820.00 Interest 305600.00 0.00 0.00 0.00 0.00 305600.00 Local Conveyance 34500.00 17560.00 0.00 0.00 17560.00 16940.00 Festival Expenses 132400.00 0.00 0.00 0.00 0.00 132400.00 Commission 75000.00 0.00 0.00 75000.00 75000.00 0.00 Business Promotion 123400.00 0.00 0.00 101400.00 101400.00 22000.00

Capital Expenditure- Car 735000.00 0.00 0.00 735000.00 735000.00 0.00 Reporting Amount 22355475.00 199660.00 177040.00 19488780.00 19865480.00 2489995.00 Depreciation 76560.00 NA NA NA NA NA

One can give consolidate figures for all the expenditure under this clause or one can give Revenue and Capital Expenditure under the serial Number 1 and 2 but it should be noted there is no place in the utility to mention the expenditure under the head Revenue and Capital Expenditure with name. Hence consolidate figure can also serve the purpose. Further in case of Depreciation, In my opinion there is no need to include figure of depreciation in these figures because in that case further bifurcation is not possible but if you choose to include the figure of depreciation then use your discretion and ask the client to submit the details in such manner. This is illustrative description of the figures to be reported in the Clause 44 of Form 3CD based on certain opinion of the Author of this Article. The comments for improvement of the study are invited to make it more useful.