Download

1 / 21

210 likes | 404 Vues

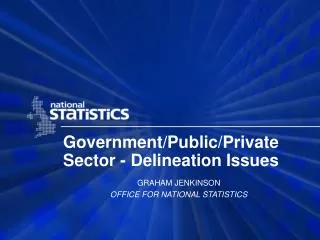

Government/Public/Private Sector - Delineation Issues. GRAHAM JENKINSON OFFICE FOR NATIONAL STATISTICS. More CONTROL Less. Public Sector. Private Sector. Non- Market ie Sales <50% of costs Market ie Sales >50% of costs. General government Examples: HM Treasury

E N D

Government/Public/Private Sector - Delineation Issues GRAHAM JENKINSON OFFICE FOR NATIONAL STATISTICS

More CONTROL Less Public Sector Private Sector Non- Market ie Sales <50% of costs Market ie Sales >50% of costs General government Examples: HM Treasury Kent County Council Non-profit institutions - NPISH Example - Oxfam (includes households) Public corporations - both real and quasi - non -government. Examples: Post Office London Underground Private market: Financial and non-financial corporations Example: British Airways

Important issues: • UK examples • EU focus on general government Focus on improving SNA • but also greater harmonisation with IPSAS

Many Issues identified Agree - the priorities

Recommendation 1 The definition of control in the SNA be extended to include the power to receive a benefit (other than from tax) The proposed change will result, correctly, in the classification of pension funds for public sector employees in the private sector

Recommendation 2 The treatment of foreign subsidiaries of public corporations cannot be harmonised. But recommend that separate records of domestic and foreign subsidiaries should be maintained in the financial accounting data so that the correct economic statistics can be derived.

Recommendation 3 Elaborations from IPSAS of the definition of control should be added to the text of SNA In general, more elaboration of the definitions of control is needed in both the SNA and the IPSASs to ensure uniform treatment

Recommendation 4 Common standards should be developed on the treatment of Special Purpose Vehicles jointly for both SNA and IPSASs - to fill the current vacuum Recommendation 5 Guidance should be added to SNA on the statistical treatment of public - private joint ventures (Units cannot be partitioned in SNA.)

Recommendation 6 Clarify SNA treatment of corporations jointly controlled by several public sector entities Consider clarify of IPSASs on this point (Corporations owned by governments of more than one country?)

Recommendation 7 • Further clarification of the status of non-profit institutions in both the SNA and the IPSASs • (Issue is interpretation of the requirement to “control and mainly finance” in current SNA.)

Recommendation 8 SNA should explain more fully the concept of economically significant prices so that it can be applied more uniformly. Recommendation 9 Research and clarify how entities of the public sector are classified (A relaxation of the IPSAS definition of a GBE would improve harmonisation.)

Recommendation 10 To facilitate the compilation of economic statistics, it is desirable to maintain financial accounting data in sufficient detail to meet the needs of economic statistics. (SNA aggregates, IPSAS and GFS consolidate - should SNA change?)

How to package all this? Clear it is a clarification of SNA Not a fundamental change

Two big issues: Better definition of control together with indicators of control Better definition of economically significant prices with supporting examples Other issues are relatively minor

Public sector boundary: • Change the definition of control in the SNA to include: the power to receive a benefit from the controlled entity (1) explanation that the power to control must be presently exercisable and that regulatory powers do not imply control (3) use of a decision tree (-)

Clarification and elaboration of the SNA of: • Definition of an institutional unit (9) • classification of non-profit institutions (7) • distinction between foreign and domestic operations of public corporations (2)

Guidance in the SNA on how to evaluate and classify : • special purpose vehicles (4) • public joint ventures (6) • public-private joint ventures (5)

Clarification and elaboration in the IPSASs of: • definition of the reporting entity (9) • classification of non-profit institutions (7)

Guidance in the IPSASs on how to evaluate and to classify: • special purpose vehicles (4) • public joint ventures (6) • public-private joint ventures (5)

General government sector: • Clarification and elaboration in the SNA of concept of market/non-market production (8) economically significant prices (8)