Budget

Budget. A financial plan drawn up for an individual, a family, a business or a government. It is usually for a period of a month or a year. Done right it should be able to tell you if you spend more than you earn and how much you can afford to spend. . Credit . In the Red.

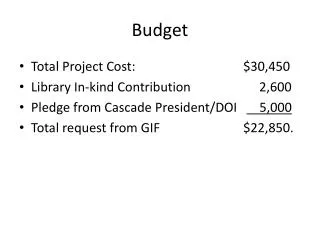

Budget

E N D

Presentation Transcript

A financial plan drawn up for an individual, a family, a business or a government. It is usually for a period of a month or a year. Done right it should be able to tell you if you spend more than you earn and how much you can afford to spend.

Credit In the Red

Money to buy goods or services that the lender will require to be paid back in the future.

A card used to borrow money or pay for purchases. You get a limit you can spend up to and you make repayments monthly. Remember! Credit cards do you not give you free money! Every penny you spend has to be repaid!

A card issued by a bank. Used in a similar way to credit cards, but the cash comes straight out of your bank account.

What you earn on money you keep in a bank account, or money you pay to borrow.

The cost of borrowing money or what you’re paid by the bank when you save. For example Borrow £1,000 at 20% APR over a year and you'll be charged £200 interest (20% of £1,000). Conversely it can be the money you earn when you save money.

Stands for annual percentage rate and it’s the official rate for borrowing over a year. It includes any fees you pay as well as the cost of borrowing.

Compound Interest

Compound interest is a key issue when it comes to saving and borrowing; in essence it’s the interest paid on interest. For example: • Suppose you had £100 in a savings account which paid 10% annual interest (if only!). After year one you'd have £100 plus £10 interest (10% of £100), a total of £110. Yet after year two, you'd earn another £10 interest (the interest on the original £100), plus a further £1 of interest earned on the £10 interest from the first year. So now you've a total of £121. • By year three, you'd be earning interest on the interest from year two, and interest on the interest on the interest from year one (gulp). And that's basically what compounding is all about.

Minimum Repayments

Unlike mortgages and loans, with credit cards you choose how much you pay back per month, the more you pay the faster the debt clears. The only restriction is that there's always a prescribed minimum repayment; the lowest amount you must repay each month to avoid a fine. Rather than a fixed amount, it is usually 2% or 3% of the outstanding debt, with a £5 minimum. However the danger with minimum repayments is that as the amount of debt decreases so does the minimum repayment

A balance transfer is when one credit card repays debts on other credit or store cards; so you now owe it the money instead, hopefully at a special cheap rate.

An agreement between a lender and a borrower. The borrower agrees to repay the money borrowed over a period of time – with or without interest.

Overdraft £0.00

An arrangement with a bank which allows customers to withdraw more funds from a current account than they have in the account. It is a form of lending.

A bank account which pays interest. It is not designed as a day-to-day bank account.

A store card works like a credit card, but can only be used in the store that issued it. Usually these types of cards have astronomically high interest and should be avoided.