Download

1 / 31

470 likes | 925 Vues

Project Appraisal, NPV and IRR . Corporate Finance 3. Project appraisal: net present value and internal rate of return. Theoretical justifications for using discounted cash flow techniques in analysing major investment decisions Time value of money Opportunity cost of capital

E N D

Project Appraisal, NPV and IRR Corporate Finance 3

Project appraisal: net present value and internal rate of return • Theoretical justifications for using discounted cash flow techniques in analysing major investment decisions • Time value of money • Opportunity cost of capital • Calculate net present value and internal rate of return • The relationship between net present value and internal rate of return • Two potential problems that can arise with internal rate of return

Value creation and corporate investment • The purpose of allocating money to a particular division or project is to generate cash inflows in the future, significantly greater than the amount invested • The time value of money: investors have alternative uses fot their funds and they therefore have an opportunity cost if money is invested in a corporate project • The investor’s opportunity cost: the sacrifice of the return available on the best forgone alternative • Investments must generate at least enough cash for all investors to obtain their required returns. If they produce less than the investor’s opportunity cost then the wealth of shareholders will decline

Investment appraisal: objective, inputs and process Exhibit 2.2 Investment appraisal: objective, inputs and process

The time value of money • Compensation is required to induce people to make a consumption sacrifice • Compensation will be required for at least three things: • Time • Impatience to consume • Pure rate of interest • Inflation • Risk

The time value of money: example • Mrs Ann Investor • Considering a £1,000 one-year investment and requires compensation for three elements of time • A return of 4 per cent is required for the pure time value • Inflation 10 per cent over the year • To compensate the investor for impatience to consume and inflation the investment needs to generate a return of 14.4 per cent, that is: (1 + 0.04) (1 + 0.1) – 1 = 0.144 • The figure of 14.4 per cent is the risk-free return (RFR) • Required return = RFR + Risk premium (Time value of money)

Project Alpha, simple cash flow Exhibit 2.3 Project Alpha, simple cash flow

1 (1 + i)n Project Alpha, simple cash flow • F = P (1 + i)n • Where F = future value • P = present value • i = interest rate • n = number of years over which compounding takes place • Deposit £100 in a bank account paying interest at 8 per cent per annum, after three years: • F = 100 (1 + 0.08)3 = £125.97 • How much must I deposit in the bank now to receive £125.97 in three years? F P = or F × (1 + i)n 125.97 P = = 100 (1 +0.08)3

Project Alpha, discounted cash flow Exhibit 2.4 Project Alpha, discounted cash flow

Net present value and internal rate of return: Hard Decisions plc • Proposal 1: Clean up and sell – Mr Brightspark’s figures • Clearing the site plus decontamination, payable t0 –£5m • Sell the site in one year, t1£12m • Profit £7m • Point 1 • The opportunity cost for our shareholders of buying shares in this firm is 15 per cent • Opportunity cost of capital

The investment decision: alternative uses of firm’s funds Exhibit 2.5 The investment decision: alternative uses of firm’s funds

Opportunity cost and discounted cash flow • Point 2 • Immediate sale value would be £6m • Opportunity cost • Proposal 1: Clean up and sell – Year t0 cash flows • Immediate sale value (opportunity cost) £6m • Clean-up, etc. £5m • Total sacrifice at t0£11m

Hard Decisions plc • Point 3 • Comparing the initial outlay directly with the final cash flow on a simple nominal sum basis: • F = P (1 + k) • where k = the opportunity cost of capital: • 11 (1 + 0.15) = £12.65m

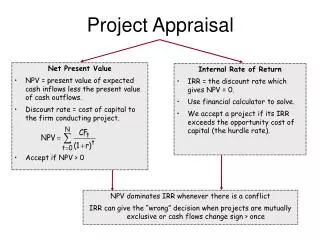

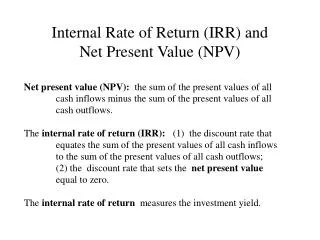

Net present value of the project CF1 NPV = CF0 + (1 + k)n where CF0 = cash flow at time zero (t0), and CF1 = cash flow at time one (t1), one year after time zero: 12 NPV = –11 + = –11 + 10.43 = –0.56m 1 + 0.15 Decision rules for net present value: NPV ≥ 0 Accept NPV < 0 Reject An investment proposal’s net present value is derived by discounting the future net cash receipts at a rate which reflects the value of the alternative use of the funds, summing them over the life of the proposal and deducting the initial outlay.

Proposal 2: Office complex – MrBrightspark’s figures Exhibit 2.6

Discount all its cash flows at the opportunity cost of capital CF1 CF2 CF3 CFn …. + + + NPV = CF0 + 1 + k (1 + k)2 (1 + k)3 (1 + k)n Exhibit 2.7

Proposal 3: Worldbeater manufacturing plant Exhibit 2.8

Proposal 3: Worldbeater manufacturing plant Exhibit 2.9

Internal rate of return Outlay = Future cash flows discounted at rate r CF1 CF2 CF3 CFn …. CF0 = + + 1 + r (1 + r)2 (1 + r)3 (1 + r)n The internal rate of return, r, is the discount rate at which the net present value is zero CF1 CF2 CF3 CFn …. CF0 + + + = 0 1 + r (1 + r)2 (1 + r)3 (1 + r)n

Proposal 1: Internal rate of return CF1 CF0 + = 0 1 + r 12 –11 + = 0 1 + r • Let us try 5 per cent: 12 –11 + = £0.42857m or £428,571 1 + 0.05 • Try 10 per cent: 12 –11 + = –0.0909 or –£90,909 1 + 0.1 • Try 9 per cent: 12 –11 + = +0.009174 or +£9,174 1 + 0.09

Interpolation for Proposal 1 A ® B 9,174 – 0 = = 0.0917 A ® C 9,174 + 90,909 IRR: ) ( 9,174 = 9 + × (10 – 9) = 9.0917 per cent 100,083 Exhibit 2.10

Internal rate of return • If k > r reject • If k < r accept Exhibit 2.11 The relationship between NPV and the discount rate (using Proposal 1’s figures)

The relationship between NPV and the discount rate for Project proposal 1 Exhibit 2.12 The relationship between NPV and the discount rate for Project proposal 1

Internal rate of return : Proposal 2 –4 –10 1 –11 + + + (1 + r) (1 + r)2 (1 + r)3 2 4 1 + = 0 + + (1 + r)4 (1 + r)5 (1 + r)6 • Try 14 per cent: • NPV (approx.) = –£0.043 or –£43,000 • At 13 per cent: • NPV = £932,000 932,000 13 + × (14 – 13) = 13.96% 975,000

Graph of NPV for Proposal 2 Exhibit 2.14 Graph of NPV for Proposal 2

The accuracy of the IRR calculated Exhibit 2.16 The accuracy of the IRR calculated may depend on the size of the gap between the discount rates used in the interpolation calculation

Proposal 3: IRR CF1 CF3/r CF0 + + = 0 1 + r (1 + r)2 • Try 19 per cent: • –10 5/0.19 • –11 + ––––––– + –––––––– = –£0.82m • 1 + 0.19 (1 + 0.19)2 • Try 18 per cent: • –10 5/0.18 • –11 + ––––––– + –––––––––– = £0.475m • 1 + 0.18 (1 + 0.18)2 • 475,000 • 18 + –––––––––– × (19 – 18) = 18.37% • 1,295,000

Problems with internal rate of return • Multiple solutions Internal rates of return are found at 11.56 per cent and 288.4 per cent

Problems with internal rate of return 2 • Ranking