Download

1 / 10

100 likes | 208 Vues

This presentation by Thomas Baunsgaard provides insights into tax collections, exemptions, and necessary reforms within Tanzania's fiscal framework. It explores target improvements in tax revenue, highlights the increase of exemptions outpacing revenue growth, and outlines the government's commitment to VAT reform. The presentation discusses the aim of rationalizing tax exemptions to align with international best practices and ensure improved efficiency in the VAT system. It emphasizes the importance of limiting exemptions, enhancing compliance, and fostering a more equitable tax environment that supports business and investment.

E N D

Tax Collections, Exemptions, and Reform Thomas Baunsgaard Presentation to the DPG Main January 15, 2013

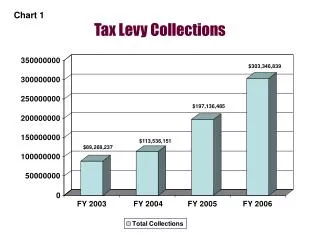

Part I. Tax revenue improvement: Providing fiscal space Source: Tanzania Revenue Authority and IMF estimates

Part II. Increase in exemptions outpaced revenue …signs of a turnaround? Source: Tanzania Revenue Authority and IMF estimates

Exemption creep in domestic VAT Source: Tanzania Revenue Authority and IMF estimates

Two-thirds of exemptions from VAT on imports and domestic transactions Source: Tanzania Revenue Authority

Other tax exemption ratios Source: Tanzania Revenue Authority and IMF estimates

Part III. VAT Reform • The Government target of a gradual reduction in tax exemptions to 1 percent of GDP (GBS PAF)… • …can only be achieved by reducing VAT exemptions • Minister Mgimwa announced a review of the VAT “to conform to international best practice” (Budget speech, June 2012) • IMF missions on VAT policy in 2011 and 2012; legal expert is working with the government on a draft VAT bill

Goal for VAT redrafting To reform the VAT into a more equal and equitable tax that is: ¶ more revenue productive ¶ easier to comply with and to administer, and ¶ provides a more business and investment friendly climate A modern broad-based VAT: Single rate; broad tax base; destination based General tax on consumption by taxing value added with credits/refunds of input tax

Aim: Rationalization of exemptions Goal: Replace extensive zero-rating and exemption schedules with simpler regime. Limit zero-rating to exports Why exempt? • On equity grounds • Basic needs (some food items) • Health & education • Land, residential property (except sales of new residential property) • Non-commercial supplies by approved non-profits • Non-commercial activities of government entities • On technical, practical grounds • Financial services, except if provided for an explicit fee

Aim: Rationalization of exemptions (cont’d) • Import exemptions • Goods for which the supply would be exempt • Goods in transshipment, containers • Donations, disaster relief goods • Imports under international agreements (treaties, financing agreements); refunds for VAT incurred domestically • To counter exemption creep, need improved VAT refund mechanism • Exemptions only through legislation – reduce discretion