Mastering DCF Analysis for Finance: A Comprehensive Guide

Learn essential concepts of Discounted Cash Flow Analysis (DCF), including forecasting revenue, calculating discount rates, and determining fair values. Gain insights into predicting future cash flows, operating costs, tax rates, and net investments. Discover how to assess the cost of equity and debt, calculate the Weighted Average Cost of Capital (WACC), and derive enterprise and fair values. Enhance your financial analysis skills with practical examples and alternate formulas.

Mastering DCF Analysis for Finance: A Comprehensive Guide

E N D

Presentation Transcript

UofT Engineering Finance Association Finance 101 DCF Analysis Kelvin Xu Slides prepared by: Asthon Wu, Garrett Kuhlmann

Introduction UTEFA • Need to learn theory of DCF before learning how to use the spreadsheet • The Forecasting Period & Forecasting Revenue Growth • Forecasting Free Cash Flows • Calculating the Discount Rate • The Fair Value

Background UTEFA • Projects how much money a company will make in the future • Determines a fair price based on this projection • “Time value of money” • Several approaches: free cash flow to equity, dividend discount model, cash flow to firm

The Forecast Period UTEFA • Need to determine how far into the future to project cash flows (the forecast period)

Revenue Growth Rate UTEFA • One of the most important assumptions one can make about the company’s future cash flows • Consider future of company and market • What does the company predict? • Is the market expanding or contracting?

Example UTEFA • Company predicts revenue to grow by 20%, but has been growing consistently at 10% in the past

Free Cash Flow UTEFA • The actual amount of cash a company has left from its operations to enhance shareholder value • Development of new products, or paying dividends

Alternate Formula UTEFA

Operating Costs UTEFA • COGS, SG&A, R&D • Look at historic operating cost margin • Can decrease due to efficiency improvements • Can increase due to price adjustments to stay competitive

Example UTEFA • Operating cost margin of 70% for three years • Company says cost cutting will push down operating cost margin to 60% over 5 years • Make an educated prediction

Tax Rates UTEFA • Many companies do not actually pay corporate tax rate due to tax breaks • Look at average tax paid over past few years as a prediction for future tax rates

Net Investment UTEFA • E.g. NetInv-2 = NetInv-3 = 10% of revenues • CAPEX-1 = $10M with Dep = $3M • => NetInv0 = $7M = 7% of revenues

Change in WC UTEFA • Cash required for day-to-day business operations • Increases as sales revenue grow

FCF UTEFA

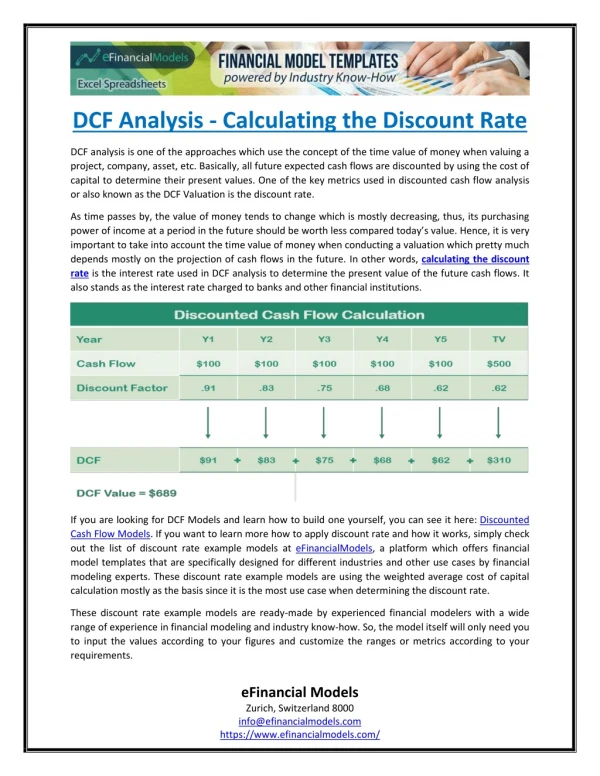

Discount Rate UTEFA • We need to discount the projected free cash flows to find out what they are worth today • This discount rate is different for every company • We discount the cash flows at the Weighted Average Cost of Capital (WACC)

Discount Rate UTEFA • Re = cost of equity Rd = cost of debt E = market value of the firm's equity D = market value of the firm's debt V = E + D E/V = percentage of financing that is equity D/V = percentage of financing that is debt Tc = corporate tax rate

Cost of Equity (Re) UTEFA • Investors generally wish to receive a premium for investing their money in the company • Use Capital Asset Pricing Model to find this value • Re = Rf + β(Rm – Rf)

Cost of Equity (Re) UTEFA • Re = Rf + β(Rm – Rf) • Beta may be found on any finance website and is a measure of how correlated the companies stock price is with the market • Rf is the Risk Free Rate • Rm is the rate of return on the market

Cost of Debt (Rd) UTEFA • Rd may usually be found on a companies financial statements • Tells the investor what rate the company borrows at • If it is not in the financial statements, it may be estimated from similar companies

WACC UTEFA • Suppose The Widget Company has a capital structure of 40% debt and 60% equity, with a tax rate of 30%. The borrowing rate (Rd) on the company's debt is 5%. The risk-free rate (Rf) is 5%, the beta is 1.3 and the risk premium (Rp) is 8%. The WACC comes to 10.64%.

Terminal Value UTEFA • To forecast the companies growth into the future, we use the Gordon Growth Method: • Terminal Value = Final Projected Year Cash Flow X (1+Long-Term Cash Flow Growth Rate) (Discount Rate – Long-Term Cash Flow Growth Rate)

Terminal Value UTEFA • Assume that the company's cash flows will grow in perpetuity by 4% per year. At first glance, 4% growth rate may seem low. But seen another way, 4% growth represents roughly double the 2% long-term rate of the U.S. economy into eternity. • Widget Company Terminal Value = $21.3M X 1.04/ (11% - 4%) = $316.9M

Enterprise Value UTEFA • We have forecasted five years of short term growth, plus found the terminal value of the company • Now we need to piece it all together to find the total value of the company

Enterprise Value UTEFA • Discount all the free cash flows using the WACC to find the Net Present Value (NPV) of the flows • EV = ($18.5M/1.11) + ($21.3M/(1.11)2) + ($24.1M/(1.11)3) + ($19.9M/(1.11)4) + ($21.3M/(1.11)5) + ($316.9M/(1.11)5) EV = $265.3M

Fair Value UTEFA • Need to account for the debt that a company has • As investors, we are only purchasing equity of a company so we subtract the debt that the company has on its balance sheet • Fair Value of Widget Company Equity = Enterprise Value – Debt

Fair Value UTEFA • After we find the fair value for the company, divide that number by the amount of shares outstanding to find the share price • Say the Widget Company had no debt, and 2 million shares outstanding: • 265.3 M/2 M = 132.65$ per share fair value