Download

1 / 31

310 likes | 410 Vues

Discover the intricacies of global foreign exchange market transactions, including spot, outright forward, and swaps. Learn how these transactions work and their significance in the foreign currency exchange market. Explore real-life examples of spot transactions, outright forward contracts, and foreign exchange swaps. Understand how hedging with forward contracts, FRA, and Forex swaps can help mitigate risks associated with interest rates and currency fluctuations. Dive into the world of foreign exchange markets and enhance your knowledge of forex trading.

E N D

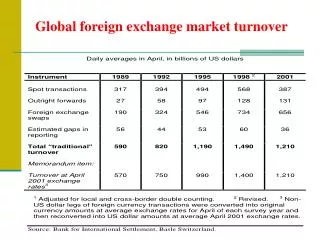

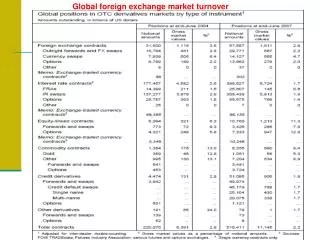

Foreign Exchange Transactions • A foreign exchange market transaction is composed of: • spot, • outright forward and • swaps. • The global daily foreign exchange market turnover by types of transaction as reported by Bank for International Settlement in 1989 through 2001 is depicted in exhibit 3.2. Average daily turnover for all currencies was $1.1369 trillion, of which 43 percent involving spot transactions, 9 percent over the counter forward transactions and 48 percent foreign exchange swaps as of April 1995.

Spot Transaction • A spot transaction involves the exchange of one currency, for example, the U.S. dollar with the Japanese yen at an agreed exchange rate to be settled in cash in two business days between two counter parties. • The spot transaction nearly accounts 40 percent of all transactions in the foreign currency exchange market. For example Kodak needs to pay £10 million to a British supplier in a spot transaction. The foreign exchange dealer in New York has quoted the pound as follows: • $1.5210-$1.5240 • Kodak pays $15.24 million U.S. dollar in two business days to settle the spot transaction at the ask rate of $1.5240. The foreign exchange dealer profit from the above spread in dollar term is $30,000.

Outright Forward • An over the counter transaction involving the exchange of one currency, for example, the British £ with the euro at the forward exchange rate determined today for the delivery to take place for cash settlement in more than two business days. • Example: Hedging with Forward Contract: Nissan manufacturing enters into a forward contract with the Bank of America today to sell 350 million yen at a forward price determined today and Nissan will deliver yen in 31 days to the Bank of America, the Bank has the following quote for 31days yen forward: • 121.32-122.40 • In 31 days Nissan delivers the yen and receives $2.8595 million at the ask price of 122.40 Ų/$.

Hedging with FRA • The forward rate agreement FRA is an over the counter instrument to hedge interest rate risk. • Example: Assuming a manufacturing firm wishes to borrow $10 million in 60 days for only 30 days. To protect himself from rising interest rate, he buys an FRA at 7.125 percent. In 60 days the 30-days rate at the spot is 9.125%. The losing party, in this case the buyer of the FRA, will receive the present value of the difference in 60 days as follows: • Cash received by the losing party= 10M [( .02 ) (30/360)] / (1+09125x30/360) = $16,540.95 • The buyer of FRA is indirectly guaranteed the rate at 7.125 percent in 60 days. However, if the actual rate exceeds the agreed rate say by 1.5 percent in 60 days the losing party, in this case the buyer of the FRA gets compensated by the present value of the difference in 60 days, since, the buyer of the FRA has to pay at the spot 1.5 percent more to acquire the capital needed. • If the rate in 60 days falls by 1.375 percent, the buyer of the FRA in 30 days will be borrowing at spot at 1.375 percent below the agreed rate and the present value of this amount has to be sent to the seller of the FRA in 60 days.

Foreign Exchange Swaps • A contract involving two counterparties to exchange, for example the U.S. dollar for the Singapore dollar in principal amount only in two business days at the prevailing spot exchange rate for cash settlement at the expiration of the contract (the short leg), and reversal of the exchange of the same two currencies at the forward rate agreed by the two parties and at a date in future say three business days known as (long leg) provided that the rate for the long leg is usually different from the rate prevailing at the conclusion of the short leg. • The above foreign exchange swap described is a spot / forward swap. When the short leg of the swaps is more than 2 business days, then the swap is the forward/forward swaps. • A FOREX Swap can also be described as the portfolio of long and short position entered simultaneously in two different dates prevailing in the future say 30 and 60 days and at the rate determined today for the respective, that is, 30 and 60 days forward rate.

Example: An importer needs £1,000,000 in 60-days for only 30 days to pay for an outstanding obligations entered with a British supplier. The importer has few alternatives: • Buy 30-days FRA in 60-days as of today, • Wait and borrow in 60-days by paying the prevailing spot rate or • Enter into foreign exchange swap agreement. • Example: Suppose the importer sells £1,000,000 60-days forward at $1.5210/£ and simultaneously buys £1,000,000 90-days forward at $1.5278/£. This swap transaction is borrowing in disguise for 30 days at fully collateralized basis at the U.S. rate of 5.36 percent per annum. • The implied 30-days forward repo-rate as the importer is selling pounds 60-days forward with the agreement to buy it back in 90-days as follows: • (1+ repo-rate)= $1.5278/£/$1.5210/£ • The actual 30-days rate in 60 days could be higher or lower than 5.36 percent.

Foreign Exchange Market Functions • Three types of transactions take place in the foreign exchange market. Each transaction is intended to provide a particular function. For example, • A spot transaction is intended to transfer purchasing power from one party to another and vice versa. • The forward transaction is intended to transfer risk from one party to another, transferring risk is hedging that is intended to reduce the exposure to foreign exchange risk and finally • A swap transaction is essentially a financing at a fully collateralized basis.

Triangular Arbitrage • It is possible that the foreign exchange rate spot or forward delivery in the Inter-bank market to be out of sink temporarily and arbitragers try to align the currency by buying and selling the under-valued or over-valued currency. • Suppose the bid ask price for the pound/$, yen/$ and yen/£ is quoted as follows by banks in United kingdom, United States and Japan. • . Bid Offer • pound/$ .69103 .69343 • $ /yen .00794028 .00802503 • yen/£ 182.85 183.92 • The yen appears to be non-aligned as the cross-currency implied exchange rate for the bid and offer price for yen/£ respectively has to be equal to 179.70-182.24.

Exchange rate pass-through • The exporter has three options as far as how much of the increase in import price due to its own currency appreciation is willing to absorb. • 1. Absorb all of the increase in import price by cutting its profit margin and or cost, zero pass-through. • 2. Absorb none of the increase in import price and passes all of the increase to the importer, 100% pass-through. • 3. Absorb some of the increase and pass the remaining to the importer, partial pass-through, under 100%.

Exchange rate pass-through • Suppose Lexus is priced at 3.5 million yen, the current spot is 100Ų/$. Assuming yen appreciates to 90Ų/$, the dollar price of the Lexus will rise from $35,000 to $38,889 in a complete pass-through. • However, at this price Lexus might lose business to competing cars and therefore, the price in the U.S. may go up to $37,100. The price in the U.S. is only increased by 6 percent while the yen appreciated by 11.11 percent. • The pass-through is incomplete and the degree of pass through as the ratio of the change in U.S. price and the change in the exchange rate or .06/. 1111, is 54 percent.

Exchange Rate Pass-through Coefficients for Selected U.S. Manufacturing

IRP 7% $1000 1070 S=$1000/Sf 5000 F=$1070/SF 5000 SF 5000 SF 5250 5%

The forward premium or discount (F– S0)/ S0 is in direct quote and in equilibrium has to be equal approximately to interest rates differential in the Equation 3.7 as follows: • (F– S0)/ S0 ( R$ – Rf)

Example IRP • Suppose interests differential in dollars and Swiss francs is 4 percent per annum (U.S. and Swiss interest rates are 7 and 3 percent respectively) and SF is in 1.4 percent premium against dollar, with spot rate at $.633/SF and one year forward in SF is $.6419/SF. • There is deviation from parity and borrowing SF1,000,000. at 3 percent, That is SF1,030,000 • and buying US $, $633,000, with SF1,000,000 • investing dollar $633,000(1.07) = $677,310 • and finally selling $677,310 dollar forward at $.6419/SF will result in SF1,055164.35, for a risk-less arbitrage profit of SF25,164.35, that is • SF1,055164.35-SF1,030,000=SF25,164.35

Real Exchange Rate • The nominal exchange rate adjusted for the respective inflation rates in two different economies provides a measure of the economy’s real cost of producing goods for consumption and goods for export over the given period. • The real exchange rate Er is defined as the nominal exchange rate En adjusted for the inflation differentials in two economies as follows: • Er = En (Pf / P$) • Where Pf and P$ are price index in foreign currency and dollars respectively.