Download

1 / 26

430 likes | 1k Vues

REGULATIONS ON THE PROCESSING OF AUTHORITY TO PRINT. OBJECTIVES.

E N D

OBJECTIVES • Enhance and facilitate the processing of the Authority to Print ORs, Sis, and CIs by having a full automation of the processes involved in the application, generation, approval and issuance of the same through a web-based ATP (on-line ATP) System. • Provide for the additional requirements for the printing of official receipts, sales invoices and other commercial invoices. • Classify receipts and invoices into Principal and Supplementary Receipts/Invoices. • Regulate further the printing of all invoices by setting a validity period • Provide for the standard reports pertaining to the processing of the ATP.

ISSUANCE OF RECEIPTS OR SALES OR COMMERCIAL INVOICES All persons subject to an internal revenue tax shall, for each sale and transfer of merchandise or for services rendered valued at Twenty-five pesos (P25.00) or more, issue duly registered receipts or sale or commercial invoices prepared at least in duplicate, showing the date of transaction, quantity, unit cost and description of merchandise or nature of service.

PRINTING OF RECEIPTS OR SALES OR COMMERCIAL INVOICES All persons who are engaged in business shall secure from the Bureau of Internal Revenue an authority to print receipts or sales or commercial invoices before a printer can print the same. No authority to print receipts or sales or commercial invoices shall be granted unless the receipts or invoices to be printed are serially numbered and shall show, among other things, the name, business style, Taxpayer Identification Number (TIN) and business address of the person or entity to use the same, and such other information that may be required by rules and regulations to be promulgated by the Secretary of Finance, upon recommendation of the Commissioner.

OUTBOUND CORRESPONDENCE NUMBER (OCN) A systems-generate control number which serves as reference for every Authority to Print issued to taxpayer. On-line ATP System – an IT infrastructure that caters to the on-line processing(application, approval and issuance) of ATP and the on-line generation of printer’s periodic reports with the capability to match and process data and generate discrepancy report of dubious entries

PRINCIPAL RECEIPTS/INVOICES It is a written account evidencing the sale of goods and/or services issued to the customers in an ordinary course of business.

KINDS OF PRINCIPAL RECEIPTS/ INVOICES • VAT SALES INVOICE- it is a written account evidencing the sale of goods and/or properties issued to customers in an ordinary course of business, whether cash sales or on account (credit) which shall be the basis of the output tax liability of the seller and the input tax claim of the buyer. Cash Sales Invoices and Charge Sales Invoices falls under this definition. • VAT OFFICIAL RECEIPT-it is a proof of sale of service and/or leasing of properties which shall be the basis of the output tax liability of the seller and input tax claim of the buyer. It is a written admission or acknowledgement of the fact that money has been paid and received for the payment or settlement between persons rendering services and its customers.

NON-VAT SALES INVOICES- it is a written account evidencing the sale of goods and/or properties issued to customers in an ordinary course of business, whether cash sales or on account (credit) which shall be the basis of Percentage Tax liability of the seller. • NON-VAT OFFICIAL RECEIPTS- it is a proof of sale of service and/or leasing of properties which shall be the basis of Percentage Tax liability of the seller. It is a written admission or acknowledgement of the fact that money has been paid and received for the payment or settlement between persons rendering services and its customers.

SUPPLEMENTARYRECEIPTS/INVOICES • These are also known as Commercial Invoices. It is a written account evidencing that a transaction has been made between the seller and the buyer of goods and/or services, forming part of the books of accounts of a business taxpayer for recording, monitoring and control purposes.

ACCREDITATION NUMBER A systems-generated control number issued using the System for Accreditation of Printers to accredited printers.

All persons, whether private or government, who are engaged in business shall secure/apply from the BIR an Authority to Print principal and supplementary receipts/invoices. National Government Agencies (NGAs), Government Owned and Controlled Corporation (GOCCs) and Local Government Units (LGUs) engaged in proprietary functions shall apply for ATP in the printing of their principal and supplementary receipts/invoices.

For newly registered taxpayers, the ATP shall be secured simultaneously with the Certificate of Registration (COR). The Taxpayer-applicant shall apply for an ATP and submit the required documents, using the on-line ATP system. However, in case of systems downtime, taxpayer shall apply for ATP and submit the required documents at the RDO or concerned LT Office having jurisdiction over the taxpayer’s Head Office.

ATP SYSTEM An IT infrastructure that is part of E-Reg Taxpayer Registration Information Update (TRIU) system that cater the on-line processing of ATP and the on-line submission of printer’s periodic reports with the capability to match and process data and generate discrepancy reports of dubious entries.

ON-LINE ATP SYSTEM An IT infrastructure that caters to the on-line processing (application, approval and issuance) of ATP and the on-line generation of printer’s periodic reports with the capability to match and process data and generate discrepancy report of dubious entries.

There shall be one application for ATP per establishment (HO or branch) which shall be filed with RDO/LT Office concerned where the HO is registered. Each application shall be issued a separate STP. The principal and supplementary receipts/invoices of the HO and each of the branches must have their own independent series of serial number. Each application as well as the printed accounting document/s shall reflect the exact address of the branch, TIN and the branch code attached to the TIN.

The TIN, branch code (if applicable) and address of the HO must be reflected in the printed principal and supplementary Receipts/invoices used in the business premises of the HO. Likewise, the printed principal and supplementary receipts/invoices to be issued/used in the branches(if applicable) must reflect the TIN, branch code and address of the branch/es.

VALIDITY PERIOD The approved ATP shall be valid upon full usage of the inclusive serial numbers of principal and supplementary receipts/invoices reflected in such ATP or five(5) years from issuance of the same, whichever comes first.

No ATP shall be granted for the printing of principal and supplementary receipts/invoices unless the required information which shall be prescribed in a separate revenue issuance, are reflected therein. Only BIR Accredited Printers shall have the exclusive authority to print principal and supplementary receipts/invoices.

All unused/unissued principal and supplementary receipts/invoices printed prior to the effectivity of these Regulations, shall be valid until June 30, 2013. A taxpayer with expiring ATP for its invoices/receipts (principal and supplementary) shall apply for a new ATP not later than Sixty (60) days prior to actual expiry date. All unused/unissued principal/supplementary receipts/invoices shall be surrendered to the RDO where the taxpayer is registered on or before the 10th day after the validity period of the expired receipts/invoices for destruction. An inventory listing of the same shall also be submitted.

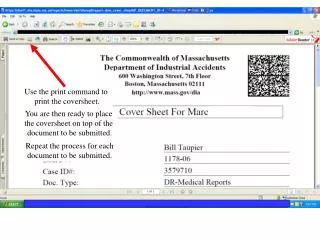

“Sample VAT OR 1.1” 10 Bklts (3x) 1001-1500 BIR Authority to Print No. 3AU000805222 Date Issued : 07-30-13: Valid until 07-30-2018 JDC PRINTING SERVICES, INC. TIN: 123-456-789-000 Printer’s Accreditation No. P08051200 Date Issued: 08-01-12 No. 1001 THIS OFFICIAL RECEIPT SHALL BE VALID FOR FIVE (5) YEARS FROM THE DATE OF ATP

“Sample VAT OR 1.2” ABC CORPORATION 76 Dilman, Quezon City VAT Reg. TIN: 144-424-024-000 OFFICIAL RECEIPT DATE ____________ Received from ____________________with TIN_______ and address at ______________________engaged in the business style of ________________________, the sum of ___________________________________________pesos (P ____) In partial/full payment for___________________. By: __________________ Cashier/ Authorized Representative No. 1001 10 Bklts (3x) 1001-1500 BIR Authority to Print No. 3AU000805222 Date Issued07-30-13 : Valid until 07-30-2018 BERTHA PRINTING SERVICES, INC. TIN: 123-456-789-000 Printer’s Accreditation No. P08051200 Date Issued 08-01-12 “THIS OFFICIAL RECEIPT SHALL BE VALID FOR FIVE (5) YEARS FROM THE DATE OF ATP”

“Sample Non-VAT OR” MA. LAURA PEDRAZA., M.D. Rm. 205 St. Luke’s Hospital, E. Rodriguez Sr.,Q.C. NON-VAT Reg. TIN: 144-424-024-000 OFFICIAL RECEIPT DATE _____________ Received from ____________________with TIN_______ and address at ______________________engaged in the business style of ________________________, the sum of ___________________________________________pesos (P ____) In partial/full payment for___________________. By: __________________ Cashier/ Authorized Representative No. 1001 10 Bklts (3x) 1001-1500 BIR Authority to Print No. 3AU000805222 Date Issued07-30-13: Valid until 07-30-2018 BERTHA PRINTING SERVICES, INC. TIN: 123-456-789-000 Printer’s Accreditation No. P08051200 Date Issued 08-01-12 “THIS DOCUMENT IS NOT VALID FOR CLAIMING INPUT TAXES” THIS OFFICIAL RECEIPT SHALL BE VALID FOR FIVE (5) YEARS FROM THE DATE OF ATP

“Sample VAT SI” 10 Bklts (3x) 1001-1500 BIR Authority to Print No. 3AU000805222 Date Issued : 07-30-13: Valid until 07-30-2018 JDC PRINTING SERVICES, INC. TIN: 123-456-789-000 Printer’s Accreditation No. P08051200 Date Issued: 08-01-12 No. 1001 THIS INVOICE SHALL BE VALID FOR FIVE (5) YEARS FROM THE DATE OF ATP

“Sample Non-VAT SI” 10 Bklts (3x) 1001-1500 BIR Authority to Print No. 3AU000805222 Date Issued : 07-30-13: Valid until 07-30-2018 JDC PRINTING SERVICES, INC. TIN: 123-456-789-000 Printer’s Accreditation No. P08051200 Date Issued: 08-01-12 No. 1001 “THIS DOCUMENT IS NOT VALID FOR CLAIMING INPUT TAXES” THIS INVOICE SHALL BE VALID FOR FIVE (5) YEARS FROM THE DATE OF ATP

JUAN DELA CRUZ Proprietor 426 Dilman, Quezon City ________ Reg. TIN: 305-410-465-000 COLLECTION RECEIPT DATE ____________ “Sample Supplementary Receipt (VAT or Non-VAT) 1.1” Received from __________________________with TIN______________________ and address at ____________________________________ engaged in the business style of __________________________________________________, the sum of ____________________________________________pesos (P_______) In partial/full payment for____________________________________. By: ____________________ Cashier/ Authorized Representative 10 Bklts (3x) 1001-1500 BIR Authority to Print No. 3AU000805222 Date Issued : 07-30-13: Valid until 07-30-2018 JDC PRINTING SERVICES, INC. TIN: 123-456-789-000 Printer’s Accreditation No. P08051200 Date Issued: 08-01-12 No. 1001 “THIS DOCUMENT IS NOT VALID FOR CLAIMING INPUT TAXES” THIS COLLECTION RECEIPT SHALL BE VALID FOR FIVE (5) YEARS FROM THE DATE OF ATP

“Sample Supplementary Receipt (VAT or Non-VAT) 1.2” No. 1001 THIS DELIVERY RECEIPT SHALL BE VALID FOR FIVE (5) YEARS FROM THE DATE OF ATP.