Download

1 / 8

80 likes | 200 Vues

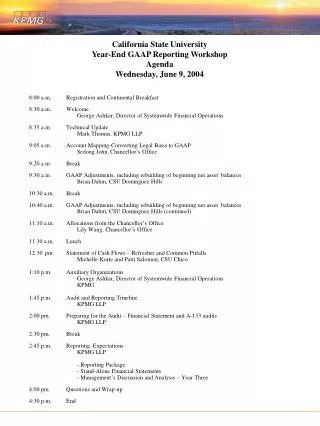

Join us for the Year-End GAAP Reporting Workshop presented by Mark Thomas from KPMG LLP on June 9, 2004. This workshop covers critical updates including GASB Statement No. 39, which clarifies the determination of component units, and the amendments in GASB Statements No. 40, 42, 43, and 44 related to deposit risks, impairment of capital assets, and postemployment benefits. Learn about the effective dates and implications for financial reporting in fiscal years 2004 through 2009. Don't miss this essential guidance for accounting professionals.

E N D

Welcome to the Year-End GAAP Reporting Workshop June 9, 2004

Technical Update Presented by Mark Thomas Partner - KPMG LLP

GASB Statement No. 39 Determining Whether Certain Organizations Are Component Units, an Amendment of GASB Statement 14 Effective: Fiscal Year 2004 • Statement of Cash Flows is not required • Elimination of Nonexchange Transactions

GASB Statement No. 40 Deposit and Investment Risk Disclosures, an Amendment of GASB Statement 3 Effective: Fiscal Year 2005

GASB Statement No. 42 Accounting and Financial Reporting for Impairment of Capital Assets and for Insurance Recoveries Effective: Fiscal Year 2006

Annual Revenues > $100 million > $10 million and < $100 million < $10 million Effective date Fiscal Year 2007 Fiscal Year 2008 Fiscal Year 2009 GASB Statement No. 43 Financial Reporting for Postemployment Benefit Plans and Other Than Pension Plans

GASB Statement No. 44 Economic Condition Reporting: The Statistical Section – an Amendment of NCGA Statement 1 Effective: Fiscal Year 2006