Download

1 / 14

150 likes | 341 Vues

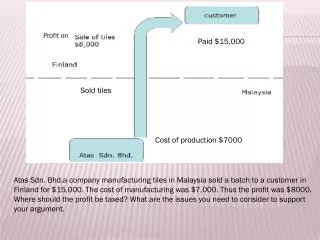

Profit on. Paid $15,000. Sold tiles. Cost of production $7000. Atas Sdn. Bhd.a company manufacturing tiles in Malaysia sold a batch to a customer in Finland for $15,000. The cost of manufacturing was $7,000. Thus the profit was $8000.

E N D

Profit on Paid $15,000 Sold tiles Cost of production $7000 Atas Sdn. Bhd.a company manufacturing tiles in Malaysia sold a batch to a customer in Finland for $15,000. The cost of manufacturing was $7,000. Thus the profit was $8000. Where should the profit be taxed? What are the issues you need to consider to support your argument.

Sale Price $15,000 AtasSdnBhd ( Branch ) Customer Sale Price $8,000 Finland ------------------------------------------------------------------------------------- Cost of production $7,000 Malaysia Atas Sdn. Bhd How much is attributed to Malaysia for taxation. What are the issues you need to consider?

Juliana Mat Jusoh 2008260974 PRESENTED BY:

ISSUE TO CONSIDERED The following considerations may be relevant when deciding whether a company is trading in or with Malaysia: The place where the contracts of sales are made. The place where the operations from which the profits arose are carried out. The place where payments are made. The place where the title to the goods passes from the seller to the buyer. Either the profit derived in Malaysia or Not? place where the contracts of sales are made. where the operations from which the profits arose

INCOME DERIVED IN MALAYSIA The Malaysian Master Tax Guide 1998 says at page 246:- “Source of business income Section 12(1) (a) provides, inter alia, that where it is necessary to ascertain the income of a business derived from Malaysia, so much of the income from the business as is attributable to operations carried on in Malaysia is deemed to be derived from Malaysia. where the operations rendered Commissioner of Inland Revenue V HK-TVB International Ltd Aneka Jasaramai Express SdnBhd V KPHDN

CIR V HK-TVB International Ltd Hong Kong Various Countries Incorporated and operated Sub licenses for TVB product solely used in customer countries Granted Sub Licenses TVB Derived in HK – Taxable Not from HK – not taxable Profit of HK57m CJ – The profits are derived from HK Provide ancillary facilities upon requested by the customer TVB staff frequency travelling to the customer countries to get the contract

AJE SdnBhd v KPHDN MALAYSIA SINGAPORE Fully operated in S’pore and did not sold return ticket Granted by S’pore authorities operate the buses Ticket Agent Sold Ticket AJE Incorporated in Malaysia Profit – Net after deducting operation cost Customer CJ – Ticket from S’pore are not derived from Malaysia Travelling to Malaysia using AJE bus Operation cost and income was treated separately in AJE Account

SITUATION 1 SITUATION 2 Profit on Paid $15,000 Sale Price $15,000 AtasSdnBhd ( Branch ) Customer Sold tiles Sale Price $8,000 Cost of production $7000 Finland ---------------------------------------------------------------- Malaysia AtasSdnBhd Cost of production $7,000 Both situation the operation and production are in Malaysia Profit are derived in Malaysia

INCOME DERIVED IN MALAYSIA Sales of Goods Act 1957 Sale and agreement to sell Sec 4. (1) A contract of sale of goods is a contract whereby the seller transfers or agrees to transfer the property in goods to the buyer for a price. There may be a contract of sale between one part owner and another. 5. (1) A contract of sale is made by an offer to buy or sell goods for a price and the acceptance of such offer. Contract Status Where contract was signed or where product was sold

SITUATION 1 SITUATION 2 Profit on Paid $15,000 Sale Price $15,000 AtasSdnBhd ( Branch ) Customer Sold tiles Sale Price $8,000 Cost of production $7000 Finland ---------------------------------------------------------------- Malaysia AtasSdnBhd There are 2 contract involved in this situation 1 – Atas HQ & Atas Branch – profit RM1K 2 – Atas Branch & Customer – Profit RM7K There are direct contract between Atas HQ & Customer in Finland – profit RM8K Cost of production $7,000

AJE SdnBhd v KPHDN MALAYSIA SINGAPORE Fully operated in S’pore and did not sold return ticket Granted by S’pore authorities operate the buses Ticket Agent Sold Ticket AJE Incorporated in Malaysia Profit – Net after deducting operation cost – No specific agreed price Customer Travelling to Malaysia using AJE bus CJ - Contract are in S’pore because the only contract involved are between ticket agent & Customer

Commissioner of Taxation of Western Australia v D & W Murray Ltd LONDON AUSTRALIA Co. was incorporated in UK - HQ Shipping the goods London Co. Branch Sold the goods Sold in Australia The Income are derived in Australia because the contract are between Branch in Australia and Australia Customer

Based on TVB – The solid income from the customer in various country are derived in HK– therefore the profit of RM8K received direct from Finland are deemed to be derived in Malaysia CONCLUSSION Profit on Paid $15,000 SITUATION 1 Sold tiles PROFIT RM8K Cost of production $7000

According to AJE & Murray – The profit of RM7k received from the contract between Atas Branch and Finland Customer are deemed not to be derived in Malaysia • The Profit of RM1k from the contract of Atas HQ and Atas Branch are deemed to be derived in Malaysia • There are others factor to be considered to determined either taxable profit is RM1k or RM7k CONCLUSSION SITUATION 2 PROFIT RM7K Sale Price $15,000 AtasSdnBhd ( Branch ) Customer PROFIT RM7K Sale Price $8,000 Finland ---------------------------------------------------------------- Malaysia AtasSdnBhd Cost of production $7,000