MARKET FOR LOANABLE FUNDS

210 likes | 1.25k Vues

MARKET FOR LOANABLE FUNDS Suppliers are people who save money; Demanders are people who borrow money; Interest Rate is the price of loanable funds: the amount of money paid for the use of a dollar for a year; RESPONSE TO INCREASED INTEREST RATES PARTY NOW

MARKET FOR LOANABLE FUNDS

E N D

Presentation Transcript

MARKET FOR LOANABLE FUNDS • Suppliers are people who save money; • Demanders are people who borrow money; • Interest Rate is the price of loanable funds: the amount of money paid for the use of a dollar for a year;

RESPONSE TO INCREASED INTEREST RATESPARTY NOW • Save less and spend more this year. • Since a higher interest rate means that each dollar saved earns more interest, a person can save less and still have the same amount of money to spend next year; • If interest rate changed from 4% to 10%, and person saved $946 instead of $1,000, the person would still have $1,040, • and have $54 to party now.

PARTY LATER • Save the same amount this year and spend more next year; • The higher interest rate means that a person who continues to save the $1,000 this year will have more money to spend next year; • $1,100 instead of $1,040: $60 for next year’s party. PARTY HEARTY LATER • Save more this year and spend much more next year; • A person who saves more than $1,000 will have much more to spend next year; • A person who saves $1,200 will have $1,320 instead of $1,040.

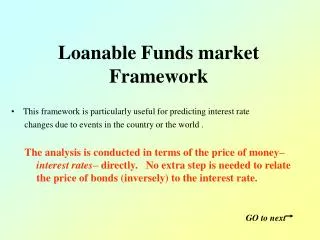

THE SUPPLY CURVE FOR LOANABLE FUNDS • Shows the relationship between interest rate and the total amount of money saved -- and available to be loaned; • To find a point on the supply curve, pick an interest rate and then add up the amounts saved by each person in the economy at that interest rate.

SUPPLY OF LOANABLE FUNDS Interest Rate (Percent) Market Supply Curve Empirical studies of saving behavior suggest that on average people save more at higher interest rates, so supply curve is positively sloped. h 6 e 4 b 2 450 500 Loanable Funds per year ($ million)

SUPPLY OF LOANABLE FUNDS • The higher the price (interest) the larger the quantity supplied; • What matters to potential savers is the net benefit from saving money; • If there were no taxes, the net benefit would be determined exclusively by interest rate; • Because taxes decrease the net benefit from savings, they decrease the amount of money saved, decreasing the supply of loanable funds.

THE MARKET DEMAND CURVE • Demand for loanable funds comes from households, firms and government; • Households borrow money to purchase expensive goods such as houses and cars; • Firms borrow money to purchase production facilities such as buildings, machines and equipment; • Governments borrow money to build facilities such as highways, schools, dams and prisons; • The federal government borrows money for the difference between tax revenue and expenditures.

THE MARKET DEMAND CURVE • The demand curve is negatively sloped; • The higher the interest rate, the smaller the amount of funds demanded.

EQUILIBRIUM IN THE MARKET FOR LOANABLE FUNDS Interest Rate (Percent) Market Supply Curve d h 6 Supply intersects demand at point e, so the equilibrium interest rate is 4%. e 4 b c 2 Market Demand Curve 450 500 720 Loanable Funds per year ($ million)

HOW DO CHANGES IN SUPPLY AND DEMAND AFFECT MARKET INTEREST RATE Increase In demand Economic growth increases the demand for all goods in the economy; Firms respond to the increase in demand by expanding their production facilities, so the demand curve will shift to the right: At each interest rate, firms will demand more funds. Increase in Supply If current workers decide to save more of their current loanable funds for retirement, the supply curve for loanable funds will shift right: At each interest rate more money will be saved.

MARKET EFFECTS OF AN INCREASE IN DEMAND Interest Rate (Percent) Market Supply Curve The increase in demand increases both the price ( interest rate ) and the quantity (quantity of loanable funds). f 5 I 4 New Demand Curve Initial Demand Curve 500 590 Loanable Funds per year ($ million)

MARKET EFFECTS OF AN INCREASE IN SUPPLY Interest Rate (Percent) Initial Supply Curve New Supply Curve The increase in supply decreases the price ( interest rate ) and increases the quantity (quantity of loanable funds). e 4 3 f Market Demand Curve 500 600 Loanable Funds per year ($ million)

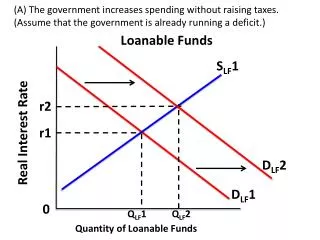

OTHER CHANGES THAT AFFECT THE EQUILIBRIUM INTEREST RATE 1. Government Spending If government increases its spending without increasing taxes, it must borrow money to finance the new spending. This deficit spending increases the demand for loanable funds and increases the equilibrium interest rate. 2. Investment subsidy If the government provides a subsidy for spending on production facilities (buildings, machines and equipment), firms will borrow more money to spend on facilities, and the equilibrium interest rate will increase. 3. Tax on interest income. A tax on interest income decreases the benefit of saving: For each dollar saved, the individual gets to keep only a part of the interest income. The decrease in the benefit of saving will decrease the supply of loanable funds, and increase the equilibrium interest rate.

OTHER CHANGES THAT AFFECT THE EQUILIBRIUM INTEREST RATE 4. Change in time preferences. If people become more patient ( more willing to delay consumption ), the supply of savings will increase and the equilibrium interest rate will decrease.

SAVINGS ACCOUNT • Can be opened in savings and loan, bank, or credit union; • The federal government insures savings accounts for amounts up to $100,000 per depositor. BOND • A promissory note issued by a corporation or government when it borrows money; • When buying a bond from a firm or government, you purchase the right to receive a fixed amount of money (the face value of the bond) at some future date and an annual interest payment; • The purchase of a bond is risky because the issuer may default on the bond; • Government bonds are less risky than corporate bonds because the government is less likely to declare bankruptcy; • The risk associated with corporate bonds depends on the health of the firm: • The more profitable the firm, the lower the risk of default.

EQUILIBRIUM INTEREST RATES FOR BANK SAVINGS ACCOUNTS AND CORPORATE BONDS Interest Rate ( % ) Interest Rate ( % ) Supply for Savings Accounts Supply for Corporate Bonds b 6 s 5 3 Demand Demand 250 100 Funds in savings accounts ( $ millions ) Funds in Corporate Bonds ( $ millions )

CORPORATE STOCKS • Corporation A legal entity that is owned by people who purchase stock in the corporation. • Corporate Stock When you buy a share ( 1 unit of ownership), you receive a certificate reflecting ownership in the corporation and gain the right to receive a fraction of the firm’s profit. • Dividends Most corporations pay part of their profits as dividends to their stockholders; they are typically paid four times a year (quarterly): the higher the profit, the larger the dividend per share of stock; Dividends are analogous to interest payments on savings accounts and bonds;

POTENTIAL BENEFITS FROM BUYING STOCK • Capital gains If the market price of the stock increases, you can sell your stock for more than you paid for it. Risk of a stock • Because a firm may turn out to be less profitable than expected, the purchase of a share of stock is risky: • dividends will be smaller than expected and the market price of the stock may decrease; • you may be forced to sell your stock for less than you paid for it.

COMPARING STOCK RATE-OF-RETURN TO INTEREST RATES OF BANK ACCOUNTS AND BONDS • Because of the laws concerning bankruptcy, corporate stocks are more risky than corporate bonds: -- when a firm goes bankrupt, it sells its assets and pays its bondholders first; -- stockholders are paid only if there is money left over after the firm pays its bondholders. • The greater risk associated with corporate stocks is reflected in higher rates of return on corporate stocks.