Download

1 / 79

790 likes | 1.25k Vues

Budget Development and Monitoring Process. Presentation Team Members:. Julie DeWall. Maryann Cullins. Jennifer Woods. Sonya Terrazas. Trudy Burke. Presentation Team Members:. Julie DeWall. Maryann Cullins. Jennifer Woods. Sonya Terrazas. Trudy Burke. What we will cover. Background

E N D

Presentation Team Members: Julie DeWall Maryann Cullins Jennifer Woods Sonya Terrazas Trudy Burke

Presentation Team Members: Julie DeWall Maryann Cullins Jennifer Woods Sonya Terrazas Trudy Burke

What we will cover • Background • Budget Development • Policies & Procedures • Budget Assumptions • Budget Monitoring • Budget Reductions or Additions • Budget Carryover • Budget Variances • Top 10 Recommendations • Summary

What we will cover • Background • Budget Development • Policies & Procedures • Budget Assumptions • Budget Monitoring • Budget Reductions or Additions • Budget Carryover • Budget Variances • Top 10 Recommendations • Summary

Bass Lake Joint Union Elementary School District Based on Interview with: Jan Chevoya Director of Business Services

Jan’s Background: • 20 Years School Business Experience • Began as Account Clerk at Yosemite High School • Previously worked at Mariposa Unified and C.O.E. • Last 10 years at Bass Lake Joint Union Elementary • Some college, no Business Degree • Previously held Adult Education Teaching Credential

District Enrollment and ADA • Enrollment 1,100 (including Mountain Home School Charter with enrollment of 100) • Declining Enrollment for past several years • 2,400 ADA

Student Demographics • Previously predominantly Caucasian population • Hispanic population increasing • Approximately 50 English Learners, requiring CLAD (Cross-cultural, Language and Academic Development) certification for teachers

District Funds • General Fund $8,000,000 Budget • Other Funds: Charter School, Bond, Child Development, Cafeteria, Deferred Maintenance, School Facilities, Developer Fees, Pupil Transportation Equipment, and Special Reserve

What we will cover • Background • Budget Development • Policies & Procedures • Budget Assumptions • Budget Monitoring • Budget Reductions or Additions • Budget Carryover • Budget Variances • Top 10 Recommendations • Summary

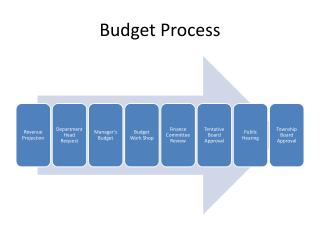

Budget Calendar Timeline • Budget development begins in November • Development continues up to June Board Meeting

Budget Development • 0.5 FTE (1/2 of Jan’s time) dedicated to budget development and administration/monitoring process

Budget Development • “Hands-on” by Jan ONLY (“nobody touches my budget!”)

Budget Development • (Budget Process CENTRALIZED!!)

Budget Development • Starts with number of students per class/per school

Budget Development • Works with Superintendent

Budget Development • Creates budget and distributes to site administrators for review and revision

Budget Development • Software Used for Budget Process • Excel Spreadsheets • QSS Financial System • SACS Software

What we will cover • Background • Budget Development • Policies & Procedures • Budget Assumptions • Budget Monitoring • Budget Reductions or Additions • Budget Carryover • Budget Variances • Top 10 Recommendations • Summary

Policies and Procedures • Board policies are in place, and they include the roles of the board and staff in preparing and approving an appropriate budget along with basic timelines and processes • The board policies are older policies and being a small school district, the board has left most of the timelines and development process up to the Director of Business Services and the Superintendent.

Policies and Procedures • The budget is given to the board in June for review and approval • Distributes budget and adjustments to Board monthly • Includes budget and enrollment projections for the subsequent two years along with monthly cash flow reports

What we will cover • Background • Budget Development • Policies & Procedures • Budget Assumptions • Budget Monitoring • Budget Reductions or Additions • Budget Carryover • Budget Variances • Top 10 Recommendations • Summary

Budget Assumptions • Presentation of Budget and Assumptions A letter is written to the board from the Director of Business Services (Jan) This letter outlines all of the following Budget Assumptions.

Budget Assumptions Continued • Data Sources • Madera County birthrate statistics for Kindergarten enrollment projections (Uses 9% of this rate as being for Bass Lake) • Relies on Fiscal Reports from School Services of California (SSC) for up-to-date information

Budget Assumptions Continued • Beginning Balance • Makes a conservative estimate of funds carried in to new year

Budget Assumptions Continued • Revenue Limit • Uses School Services of California (SSC) “dartboard” projections for Revenue Limit COLA

Budget Assumptions Continued • Attendance The full enrollment projection sheet is included in your packet (Example of detail –that you can see is on next slide)

Budget Assumptions Continued • Attendance • Estimates individual school enrollment figures based on current year actual enrollment

Budget Assumptions Continued • Attendance Each school’s estimated Average Daily Attendance (ADA) is calculated based on the historical attendance percentages

Budget Assumptions Continued • Attendance • Estimates are based on a great level of detail and go all the way down to the classroom level • Uses as estimate for number of Teacher FTE’s

Budget Assumptions Continued • Federal Revenues • Explains anticipation of revenue increases or decreases based on anticipated awards and based on carry over or deferral of prior year revenues • State Revenues • States the projected % increase that is anticipated based on SSC (School Services of California) projections • Shows anticipated Class Size Reduction Funding per student • Gives amount per ADA for Lottery Revenues that are expected

Budget Assumptions Continued • Local Revenues • States any anticipated increases or decreases due to local contracts or awards • Other Sources • Explains any Interfund transfers which are planned to occur for the year

Budget Assumptions Continued • Total Revenues • Summarizes the effect of the budget assumptions and shows how the total revenue expected to be received compares to the prior year total

Budget Assumptions Continued • Certificated and Classified Salaries & Benefits • Explains the basis for calculations such as: • No Salary or Benefit Increases • Includes Step and Column increases & associated benefits • Shows increases or decreases in staffing used for calculations

Budget Assumptions Continued • Supplies, Operating Expenses, Buildings & Equipment , and Other Outgo • Explains the basis for calculations • Shows any textbook purchases included • Explains additional purchases to be made from prior year funds carried over • Lists any expected contributions to be given to other Funds –Child Development, Cafeteria, etc.

Budget Assumptions Continued • Total Expenditures • Summarizes the effect of the budget assumptions and shows how the total expenditures expected compares to prior year totals

Budget Assumptions Continued • Ending Balance • Shows the effect that the budget assumptions have on the ending balance • Required Reserve • Shows the effect that the budget assumptions have on the required reserve

Budget Assumptions Continued • Presentation of Budget and Assumptions SACS Financial Reporting Software forms -SACS (Standardized Account Code Structure) Reporting forms are included in the budget packet given to the board Even though these forms are not very user friendly, the board is accustomed to seeing the information in this format

Budget Assumptions Continued • Presentation of Budget and Assumptions Multi-year Projections Spreadsheets Spreadsheets are given to the board that show the prior four year’s data and the data from the new year and two subsequent years. (Copies are attached in packet)

What we will cover • Background • Budget Development • Policies & Procedures • Budget Assumptions • Budget Monitoring • Budget Reductions or Additions • Budget Carryover • Budget Variances • Top 10 Recommendations • Summary

Budget Monitoring • Budget is continuously monitored by Jan • Routine budget adjustments are brought forward to the Board monthly

What we will cover • Background • Budget Development • Policies & Procedures • Budget Assumptions • Budget Monitoring • Budget Reductions or Additions • Budget Carryover • Budget Variances • Top 10 Recommendations • Summary

Program Additions / Enhancements • Staff member presents request for new program to Superintendent • Superintendent discusses it with Jan • Jan provides budget information for, and impact of, new program • Board makes final decision

Other Budget Additions or Enhancements • Budget Transfer Request Sites fill out the request form in order to move budget between line items.

Budget Reductions • Declining Enrollment • Due to declining enrollment, budget reductions are unavoidable

Budget Reductions • Staffing • As enrollment declines, staffing is also reduced • Careful planning and monitoring of class sizes is essential to making reductions • Movement of staff between site and class locations is also needed to make successful reductions

Budget Reductions • Equipment • Most equipment purchases (other than categorical) have been eliminated from the budget

Budget Reductions • Maintenance & Operations • Most maintenance and operations purchases have also been cut from the budget. • Only essential purchases are left in budget