Download

1 / 34

340 likes | 637 Vues

Outline Exchange Rates Foreign exchange market Asset approach to exchange rates Interest parity condition Empirical tests Covered interest parity. Exchange Rates The (spot) exchange rate (E) is price of one currency in terms of another for immediate trade (on the spot).

E N D

Outline • Exchange Rates • Foreign exchange market • Asset approach to exchange rates • Interest parity condition • Empirical tests • Covered interest parity

Exchange Rates • The (spot) exchange rate (E) is price of one currency in terms of another for immediate trade (on the spot). • The conventional way of reporting this in economics is home currency per unit of foreign. In the U.S. this is $ per unit foreign currency. – Example, yesterday E$/€ = 1.21 $/€, called direct (“American”) terms – Sometimes you will hear quoted the other way around, often called indirect (“European”) terms. E.g., 0.82 €/$. • Exchange rates are important for trade because they allow you to compare the cost of imports to that of domestic goods in common terms. – Example: You visit Rome and see an Armani suit for €1000. What is that in US currency? Consider units: you want to convert € to $ so you need to multiply by an exchange rate expressed in $/€ (check: multiply units and cancel). €1000 * 1.21 $/€ = $1210

Appreciations and depreciations • Our definition of E = home per unit foreign currency ($/€) • Definition can make it confusing to talk about changes in E, called appreciations and depreciations. – Appreciation: increase in value of the given (home) currency relative to another. – Depreciation: decrease in value of the given (home) currency relative to another. • Say the $/€ rate changed from 1.21 to 1.50. Now how much would the suit would cost in $ terms? – Dollars are not buying as many euros now, so the dollar has depreciated or weakened (against the euro). • If E$/€ rises we say that the dollar has depreciated (€ has appreciated) • If E$/€ falls we say that the dollar has appreciated (€ has depreciated)

The foreign exchange market: actors • Commercial banks: a company has a bank debit its account, change into foreign currency, and make payment by depositing in its foreign bank. – Inter-bank trading: bank enters foreign exchange market to execute multiple trades—very large transactions. • Corporations: some corporations enter market directly. Increasingly common. • Non-bank financial institutions: Deregulation allows them to compete in the market. E.g. pension funds. • Central banks: sometimes intervene to increase or decrease the supply of their currency or purposefully affect E. – Official interventions are relatively small, because there is so much private money involved. Is central bank a big enough player to affect E?

The foreign exchange market: character • Volume is enormous: over a trillion dollars a day. – US GDP is about $10 trillion in the whole year. • Concentrated in certain key financial cities: where? – London largest, also NY, Tokyo, Frankfurt and Singapore. • Highly integrated globally: one major market is usually open, so people can trade around the clock. • Quotes in different centers are same, by arbitrage: – If NY offers more €/$, than Frankfurt, people take $, sell in NY for €, sell these in Frankfurt for $ and end up with profit. – Computers monitoring such openings and ready to take advantage of them. So gaps close up very quickly. • Vehicle currency. Most transactions in $ – Even if want to change £ for ¥, US is large in world economy; many people willing to trade dollars for £ and ¥, rather than the opposite sides of a direct £-¥ trade. – € and Yen also used as vehicles, but less so.

Spot and forward rates • The exchange transactions talked about so far take place “on the spot.” Hence E is spot exchange rate. – Transactions that take place basically immediately. – In practice not right away because it typically takes two days for settlements, i.e. for the checks to clear. • The forward exchange rate (F) is the price for a currency trade for some date in future. – A way of hedging against the risk of E changes. – Example. Electronics wholesaler orders Sony TVs from Japan, will be billed and have to pay in ¥ in 90 days. – Could wait for the bill, then buy the ¥ to pay Sony, but who knows what will happen to yen-dollar E in meantime. – Risk: If ¥ appreciates against the $, the store will have to pay a higher $ price for the TVs. – To avoid risk, can contract now for currency to be delivered 90 days hence at set price, the forward exchange rate F¥/$.

Theories of exchange rate determination • Two main theories we study here. – The asset approach: interest rate parity – The monetary approach: purchasing power parity • Each tells a logical but somewhat different story of how E is determined. • Discuss the stories, the empirical evidence on how well each explains E movements, and how the two theories might be integrated. The asset approach • We have noted that most foreign exchange holdings are in form of bank deposits, an asset, and these can be analyzed in the same way as any other asset.

Determinants of demand for assets • What are the determinants of the demand for a financial asset? The expected rate of return. – bank savings account: the interest rate (certain). – stocks & bonds: dividends, capital gain (uncertain) • In addition to return, some savers care about two other features: risk and liquidity. – Risk: Even if a stock has a higher expected payoff than a saving account, uncertain payoff means it may be less desirable. – Liquidity: how easy it is to convert the asset to cash if you want to buy a different one or use your savings for consumption. • In the theory, we do not emphasize risk and liquidity for now. We start by assuming that main issue in deciding which asset to buy is the expected return.

Asset Returns The Rate of Return – percentage increase in value it offers over some time period The Real Rate of Return – it is measured in terms of some representative basket of products that savers regularly purchase. The expected real rate of return is considered by savers when deciding which assets they will hold.

Which asset is more profitable? To compare the expected rate of return on two deposits we need two pieces of information: • The currency interest rate: the amount of the currency an individual can earn by lending a unit of that currency for one year – tells how dollar and euro deposit values will change over a year - Deposits pay interest because they are really loans from the depositor to the bank. When a corporation or financial institution deposits a currency in a bank , it is lending that currency to the bank rather than using it for some expenditure. • The expected change in the $/€ exchange rate: to see which deposit will offer a higher expected return. - If I use dollars to by a euro deposit, how many dollars will I get back after a year?

Foreign currency assets and returns: example • In words: $100 to invest in $ or € (risk-free) account. R$ = annual interest on $ account = 2.9%. R€ = annual interest on a € account = 5%. Spot E$/€ = 1.0. Expected E in 1 year, Ee$/€ = 0.98 • In pictures: • In this example, interest parity holds. The investor is indifferent between holding each risk-free deposit.

Interest parity condition • Expresses in mathematics what we saw in words and pictures: interest parity holds when risk-free deposits earn same expected return in each location. • Def: The expected rate of appreciation of the euro against the dollar is the percentage increase in the dollar/euro exchange rate over a year = rate of depreciation of the dollar against the euro = (Ee$/€ – E$/€ ) / E$/€ The rule is: The dollar rate of return on euro deposits is approximately the euro interest rate + the rate of appreciation of the euro against the dollar (or the rate of depreciation of the dollar against the euro). (how to derive: page 339, footnote 7)

Interest parity condition • Expected net return on the euro deposit = (€ interest rate) + (expected appreciation of euro)* = R€ + (Ee$/€ – E$/€ ) / E$/€ • Expected net return on the dollar deposit = ($ interest rate) = R$ • By equating the two returns we derive the (uncovered) interest parity condition (UIP): R$ = R€ + (Ee$/€ –E$/€ ) / E$/€ If R$ - R€ - (Ee$/€ –E$/€ ) / E$/€ > 0 – dollar deposits yield higher expected rate or <0 euro deposits yield higher expected rate . • UIP is one theory of exchange market equilibrium.

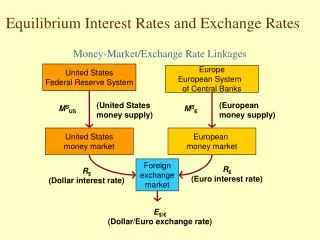

The equilibrium condition: The foreign exchange market is in equilibrium when deposits of all currencies offer the same expected rate of return. The condition is interest parity .

Foreign exchange market equilibrium: intuition • Recall that expected return on euro deposit = R€ + (Ee$/€– E$/€ ) / E$/€ • This shows that all else held constant a change in today’s spot exchange rate E$/€ will affect the expected euro return. • Appreciation of a country’s currency today raises the expected domestic currency return on foreign currency deposits, given the expected level of the exchange rate in the future Ee$/€ . • Why? Example where Ee$/€ = 1.05 and R€ = 0.05. – If E$/€ = 1.05 expected return on € deposit = 0.05 – If E$/€ = 1.03 expected return on € deposit ~ 0.07 – If E$/€ =1.00 expected return on € deposit ~ 0.10 • Locally, this appears approximately linear.

Figure 13-3 The Relation Between the Current Dollar/Euro Exchange Rate and the Expected Dollar Return on Euro Deposits (Ee$/€ = 1.05 and R€ = 0.05) An appreciation of the $ against euro raises the expected returns on euro deposit in $ terms.

What have we learned? • Why interest parity must hold if the foreign exchange market is in equilibrium • How today’s exchange rate affects the expected return on foreign currency deposits Main point: the exchange rate always adjust to maintain interest parity. Next: still assume thatEe$/€ , R€ and R$ are all given.

Foreign exchange market equilibrium: some theory and a figure • UIP says, dollar return = expected euro return, or R$ = R€ + (Ee$/€– E$/€ ) / E$/€ • Condition for foreign exchange market equilibrium. • We can apply UIP as a theory of short-run (spot exchange rate determination assuming unknown and taking as given Ee$/€ , R€ and R$. • NB: to take as given R€ and R$ requires a model of interest rates set in the money market (Chapter 14). • NB: to take as given Ee$/€ requires a model of long run exchange rate determination (Chapter 15). • Graphically. In UIP equation treat Ee$/€ as unknown: – Plot RHS return = expected euro return = hyperbola in Ee$/€ . – Plot LHS return = dollar return = is a constant.

Foreign exchange market equilibrium: adjustment • How is equilibrium attained? R$ = R€ + (Ee$/€– E$/€ ) / E$/€ How does the exchange rate adjust? • If R$ > R€ - dollar deposits more attractive, so holders of dollar deposits are unwilling to sell them. Euro deposit holders offer a better price for dollars - E$/€ falls towards E1$/€ - appreciation of the dollar. This process continue until UIP holds. The rate to which the dollar is expected to depreciate in the future increases – euro deposits more attractive • If R$ < R€ - euro deposits more attractive, so holders of euro deposits are unwilling to sell them. Dollar deposit holders offer a better price for euro - E$/€ raises towards E1$/€ - depreciation of the dollar. This process continue until UIP holds The rate to which the dollar is expected to depreciate in the future is reduced – euro deposits less attractive.

Foreign exchange market equilibrium: comparative statics • We can do important applied economic analysis by considering how markets respond to shocks. • We use the figure to develop intuition. [You can confirm all the results algebraically too.] • We can consider three types of shocks to the three variables that, for the moment, we are treating as exogenous (as given): – A change in (domestic) dollar interest rates – A change in (foreign) euro interest rates – A change in expectations about the future exchange rate • These experiments with the model correspond to changes in Ee$/€ , R€ and R$.

Uncovered interest parity: does it work? • UIP is hard to test because we do not have direct data on expectations and the Ee$/€term is crucial. • Some economists have used actual future E. • Some have used survey data on expectations. • Neither fit the data very well. • Are there reasons why simple UIP might fail? R$ = R€ + (Ee$/€– E$/€ ) / E$/€ • If risk is involved, due to future E uncertainty, people may require more (less) expected return on € deposits as compensation for uncertainty. • So we would add an additional term: a risk premium. R$ + RP= R€ + (Ee$/€– E$/€ ) / E$/€

Covered interest parity: a safe bet • If exchange risk is the problem, isn’t there a way we know to get rid of that? The forward contract. Denote the forward rate: F$/€. • Instead of UIP, this leads to CIP, a risk-free version of the interest parity condition, called covered interest parity. [That is, the risk has been covered.] R$ = R€ + (Fe$/€– E$/€ ) / E$/€ • Empirical evidence supports covered interest parity. • In fact, this is how forward exchange rates are determined in free financial markets. • Dealers (now, computers) scan the current spot rate E and the forward rate F. If they see immediate risk free arbitrage opportunity, take advantage of it. Gaps are closed instantly.

Interest parity: covered versus uncovered • UIP says R$ + RP= R€ + (Ee$/€– E$/€ ) / E$/€ • CIP says R$ = R€ + (Fe$/€– E$/€ ) / E$/€ • Does theory say F is expected future value of E? • Not necessarily. Fe$/€ = Ee$/€ if CIP/UIP hold & RP = 0. • But when a risk premium is present (RP > 0), we find F equals E minus a risk term: Fe$/€ = Ee$/€ – RP • Recall the arbitrage figure: if you dislike risk, and want to exchange future euros for dollars at a risk free (guaranteed) exchange rate, then you would be willing to pay a price for that certainty: you would accept a lower $/€ rate, i.e. Fe$/€ < Ee$/€ .