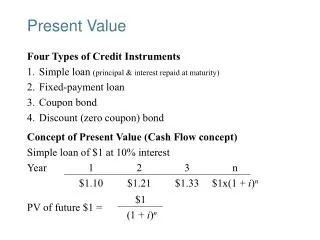

Present Value

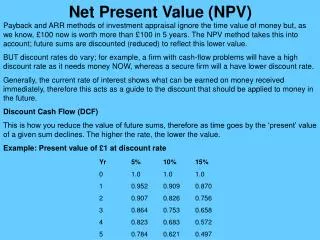

Present Value. Professor XXXXX Course Name / Number. FV n = PV x (1+r) n. Future Value depends on: Interest Rate Number of Periods Compounding Interval. Future Value. The Value of a Lump Sum or Stream of Cash Payments at a Future Point in Time. FV 4 = $262.16. FV 3 = $245.

Present Value

E N D

Presentation Transcript

Present Value Professor XXXXX Course Name / Number

FVn = PV x (1+r)n • Future Value depends on: • Interest Rate • Number of Periods • Compounding Interval Future Value The Value of a Lump Sum or Stream of Cash Payments at a Future Point in Time

FV4 = $262.16 FV3 = $245 FV2 = $228.98 FV1 = $214 Future Value of $200 (4 Years, 7% Interest ) PV = $200 0 1 2 3 4 End of Year What if the Interest Rate Goes Up to 8% ?

FV4 = $272.10 FV3 = $251.94 FV2 = $233.28 FV1 = $216 Future Value of $200 (4 Years, 8% Interest ) PV = $200 0 1 2 3 4 End of Year Compounding – The Process of Earning Interest in Each Successive Year

The Power Of Compound Interest 40.00 20% 30.00 25.00 20.00 15% Future Value of One Dollar ($) 15.00 10% 10.00 5.00 5% 0% 1.00 0 2 4 6 8 10 12 14 16 18 20 22 24 Periods

Present Value Today's Value of a Lump Sum or Stream of Cash Payments Received at a Future Point in Time

FV1 = $214 FV2 = $228.98 FV3 = $245 FV4 = $262.16 PV = $200 Present Value of $200 (4 Years, 7% Interest ) Discounting 0 1 2 3 4 End of Year What if the Interest Rate Goes Up to 8% ?

FV1 = $216 FV2 = $233.28 FV3 = $252 FV4 = $272.10 PV = $200 Present Value of $200 (4 Years, 8% Interest ) Discounting 0 1 2 3 4 End of Year

The Power Of High Discount Rates 1.00 0% 0.75 Present Value of One Dollar ($) 0.5 5% 10% 0.25 15% 20% 0 2 4 6 8 10 12 14 16 18 20 22 24 Periods

FV and PV of Mixed Stream(5 Years, 4% Interest Rate) Compounding - $12,166.5 FV$6,413.8 $3,509.6 $5,624.3 $4,326.4 $3,120.0 -$10,000 $3,000 $5,000 $4,000 $3,000 $2,000.0 0 1 2 3 4 5 End of Year $2,884.6 PV$5,217.7 $4,622.8 $3,556.0 $2,564.4 $1,643.9 Discounting

Future Value and Present Value of an Ordinary Annuity Compounding FutureValue $1,000 $1,000 $1,000 $1,000 $1,000 0 1 2 3 4 5 End of Year Present Value Discounting

Future Value of Ordinary Annuity(End of 5 Years, 5.5% Interest Rate) $1,238.82 $1,174.24 $1,113.02 $1,055.00 $1,000.00 $1,000 $1,000 $1,000 $1,000 $1,000 0 1 2 3 4 5 End of Year How is Annuity Due Different ?

FV5 = $5,888.04 $1,306.96 $1,238.82 $1,174.24 $1,113.02 $1,055.00 $1,000 $1,000 $1,000 $1,000 $1,000 Future Value of Annuity Due(End of 5 Years, 5.5% Interest Rate) 0 1 2 3 4 5 End of Year Annuity Due - Payments Occur at the Beginning of Each Period

Present Value of Ordinary Annuity(5 Years, 5.5% Interest Rate) 0 1 2 3 4 5 $1,000 $1,000 $1,000 $1,000 $1,000 End of Year $947.87 $898.45 $851.61 $807.22 $765.13

Present Value of Annuity Due(5 Years, 5.5% Interest Rate) 0 1 2 3 4 5 $1,000 $1,000 $1,000 $1,000 $1,000 End of Year $1000.00 $947.87 $898.45 $851.61 $807.22

Present Value Of Perpetuity($1,000 Payment, 7% Interest Rate) Stream of Equal Annual Cash Flows That Lasts “Forever” What if the Payments Grow at 2% Per Year?

Present Value Of Growing Perpetuity 0 1 2 3 4 5 $1,000 $1,020 $1,040.4 $1,061.2 $1,082.4 … Growing Perpetuity CF1 = $1,000 r = 7% per year g = 2% per year

Compounding Intervals m compounding periods The More Frequent The Compounding Period, The Larger The FV!

For Quarterly Compounding, m Equals 4: Compounding More Frequently Than Annually FV at End of 2 Years of $125,000 Deposited at 5.13% Interest • For Semiannual Compounding, m Equals 2:

Continuous Compounding • In Extreme Case, Interest - Compounded Continuously FVn = PV x (e r x n) FV at End of 2 Years of $125,000 at 5.13 % Annual Interest, Compounded Continuously • FVn = $138,506.01

The Stated Rate Versus The Effective Rate Stated Rate – The Contractual Annual Rate Charged by Lender or Promised by Borrower Effective Annual Rate (EAR) – The Annual Rate Actually Paid or Earned

The Stated Rate Versus The Effective Rate • FV of $100 at End of 1 Year, Invested at 5% Stated Annual Interest, Compounded: • Annually: FV = $100 (1.05)1 = $105 • Semiannually: FV = $100 (1.025)2 = $105.06 • Quarterly: FV = $100 (1.0125)4 = $105.09 Stated Rate of 5% Does Not Change.What About the Effective Rate?

Effective Rates - Always Greater Than Or Equal To Stated Rates • For Annual Compounding, Effective = Stated • For Semiannual Compounding • For Quarterly Compounding

Deposits Needed To Accumulate A Future Sum • Often need to find annual deposit needed to accumulate a fixed sum of money in n years • Closely related to the process of finding the future value of an ordinary annuity • Find annual deposit needed to accumulate FVn dollars, at interest rate, r, over n years, by solving this equation for PMT:

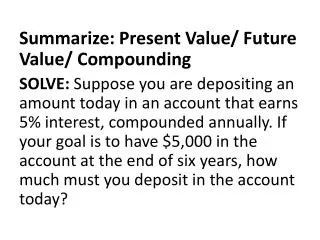

Calculating Deposits Needed To Accumulate A Future Sum • You wish to accumulate $35,000 in five years to make a home down payment. Can invest at 4% annual interest. • Find the annual deposit required to accumulate FV5 ($35,000), at r=4%, and n=5years

Calculating Amortized Loan Payments Amounts • Very common application of TV: Finding loan payment amounts • Amortized Loans are loans repaid in equal periodic (annual, monthly) payments • Borrow $6,000 for 4 years at 10%. Find annual payment. Divide PV by PVFA4,10%=3.1700

A Loan Amortization Table Loan Amortization Schedule ($6,000 Principal, 10% Interest 4 Year Repayment Period Payments End of year Beginning-of-year principal(2) End-of-year principal[(2) – (4)](5) Interest[.10 x (2)](3) Loan Payment(1) Principal[(1) – (3)](4) aDue to rounding, a slight difference ($.40) exists between beginning-of-year 4 principal (in column 2) and the year-4 principal payment (in column 4)

Much Of Finance Involves Finding Future And (Especially) Present Values Central To All Financial Valuation Techniques Techniques Used By Investors & Firms Alike