Download

1 / 90

920 likes | 1.11k Vues

Treasury Offset Program: How Federal and State Partnerships Can Cost Effectively Maximize Debt Recoveries National Association of State Auditors, Comptrollers, and Treasurers NASACT/TOP Training Webinar September 18, 2013. Opening Remarks. Speaker Ronda Kent Bureau of the Fiscal Service

E N D

Treasury Offset Program: How Federal and State Partnerships Can Cost Effectively Maximize Debt Recoveries National Association of State Auditors, Comptrollers, and Treasurers NASACT/TOP Training Webinar September 18, 2013

Opening Remarks SpeakerRonda Kent Bureau of the Fiscal Service U.S. Department of the Treasury SpeakerAlyssa Riedl Bureau of the Fiscal Service U.S. Department of the Treasury ModeratorR. Kinney Poynter Executive Director NASACT SpeakerCarol Marshall Collection Division State of Minnesota SpeakerJames Keifer Compliance Administration District of Columbia

Bureau of the Fiscal Service MissionWe exist to promote the financial integrity and operational efficiency of the federal government through exceptional accounting, financing, collections, payments, and shared services. VisionWe will transform financial management and the delivery of shared services in the federal government.

Debt Management Services (DMS) MissionWe exist to identify, prevent, collect and resolve debt owed to government agencies. VisionWe will transform government financial management as the provider of choice for shared services related to improper payments, receivables management, and delinquent debt collection.

The Role of DMS • Assist federal and state agencies in the collection of delinquent child support obligations, supplemental nutrition assistance program (SNAP) debts, income tax debts, unemployment insurance compensation debts, and other federal and state debts. • Provides access to the Do Not Pay program for the purpose of preventing, identifying and recovering federally-funded improper payments.

Debt Collection Legal Authorities • The Federal Government’s administrative debt collection activities are governed by a number of Federal laws, including: • Federal Claims Collection Act of 1966, Debt Collection Act of 1982, Debt Collection Improvement Act of 1996 and other laws, codified primarily in 5 U.S.C. 5514 and 31 U.S.C. 3701 et seq • Internal Revenue Code, Title 26 of the United States Code • Bankruptcy Code, Title 11 of the United States Code • Privacy Act of 1974, 5 U.S.C. 552a • Other statutes that apply to specific agencies, debt types or payment types • Treasury regulations, OMB policies, agency-specific regulations

Debt Collection Legal Authorities • Among other things, debt collection laws govern: • Type of due process required for various debt collection remedies • Example: 60 days notice required before a tax refund may be offset; 30 days notice required for most other debt collection actions • The amounts allowed to be collected through each mechanisms: • Example: TOP can offset 100% of a tax refund payment, but no more than 15% of a Federal salary payment; veterans benefit payments are exempt from offset • When debts may not be referred to Treasury for TOP • Example: Debts that are subject to a stay under the Bankruptcy Code are not eligible for referral

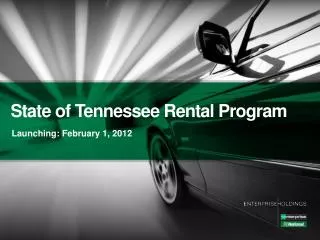

Debt Collection Programs • DMS collects delinquent debts for federal and state agencies (non-tax and tax) primarily through two programs: the Treasury Offset Program (TOP) and the Cross-Servicing Program. • DMS has collected a total of $6.87 billion as of August 2013 (an increase of +13.68% as compared to the same period in FY2012) • Treasury Offset Program - $6.72 billion as of August FY2013 • Cross-Servicing Program - $153.5 million as of August FY2013 • Cumulative collections over $60 billion since inception (1997)

TOP FY2013 Debt Collection Breakdown of $6.87B as of August 31, 2013

The State of Mississippi $7.4 Million in Unemployment Fraud Recouped in Seven Days – WLBT: Mississippi News Now WLBT, the Jackson, Mississippi, NBC affiliate aired a report in February 2012 concerning the increased collection of unemployment debts from those individuals collecting unemployment benefits fraudulently. WLBT reported that the Mississippi Department of Employment Security had collected $7.4 million in its first week participating in TOP. This means that Mississippi was able to recoup 12% of their UIC debts in just the first seven days of using the program.

The State of New YorkRecovers $51M in Fraudulently Collected Unemployment Insurance via TOPwww.governor.ny.gov “Once again, New York is at the forefront of efforts to protect taxpayer dollars through preventing and collecting fraudulently-obtained government payments. Every dollar we recover through this program becomes available to eligible unemployed New Yorkers who are most in need of this vital economic safety net. We will continue to do everything we can to collect fraudulently-obtained benefits from people who don’t deserve them, and who are in fact stealing from their fellow New Yorkers.” Andrew Cuomo, Governor State of New York

The State of Maryland State Income Tax Program “Maryland is leading the way in collecting back taxes,” said Comptroller Franchot.” Given the fiscal challenges we face, it’s critical we use all available resources to get any money owed to the state.” State Reciprocal Program “The offset program we conduct with the federal government is one of the most successful in the nation,” said Comptroller Franchot.“It keeps growing because were able to quickly certify more accounts to intercept.” Peter Franchot, Comptroller State of Maryland

Fiscal Year 2012 Annual Report to the States “We are proud of the work we do in collecting delinquent child support, in partnership with the U.S. Department of Health and Human Services, Office of Child Support Enforcement, and participating states. These funds – $2.2 billion in FY 2012 – are repaid to states or provided to meet the needs of America’s families and children.” David A. Lebryk, Commissioner Bureau of the Fiscal Service www.fms.treas.gov/debtTOP_annual_report_to_States_fy12.pdf

Treasury Offset Program (TOP) Alyssa Riedl Director, Debt Collection Program Management Directorate

Treasury Offset Program (TOP) • TOP is a centralized offset program administered by the U.S. Department of the Treasury, Bureau of the Fiscal Service, to collect delinquent debts owed to federal agencies and states. • TOP requires creditor agencies to provide debtors with due process, including proper notices and dispute opportunities, as well as the chance to repay debts over time. • TOP sends notices to debtors when payments are offset. For recurring payments, TOP sends warning notices.

TOP State Programs • State Income Tax Program (SIT)- TOP offsets federal tax refund payments to payees who owe delinquent state income tax obligations. • State Reciprocal Program (SRP) -TOP offsets federal vendor and other non-tax payments to payees who owe delinquent debts to state agencies. In return, states offset payments to payees who owe delinquent debts to federal agencies. • Unemployment Insurance Compensation (UIC) Debts- In partnership with the U.S. Department of Labor, TOP offsets federal tax refund payments to payees who owe delinquent unemployment insurance compensation debts due to fraud or a person’s failure to report earnings. • Child Support Program- States submit delinquent child support obligations to the Office of Child Support Enforcement (OCSE), which in turn submits the debts to TOP for collection through the offset of federal tax refund and other eligible payments. • Supplemental Nutritional Assistance Program - The Department of Agriculture-Food and Nutrition Service (FNS), in collaboration with state offices administering the Food Stamp Program, submit food stamp recipient debts to Treasury for offset of tax refund, federal vendor, salary, federal retirement, Social Security, Railroad Retirement, and state payments.

Treasury Offset Program State Programs TOP Database KEY SRP - State Reciprocal Program UIC - Unemployment Insurance Compensation Child Support Debt Unemployment Insurance Compensation Debt Child Support Child Support SRP UIC Federal Tax Refund Payments State Income Tax Debt Federal Non-Tax Payments (Vendor, Travel, Misc.) SRP State Income Other State Debt SRP State Programs State Payments (Vendor, State Tax Refunds, Other) Federal Non-Tax Debt Federal Programs SRP 18

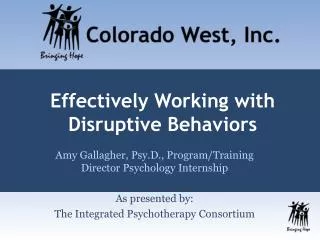

TOP State Delinquent Debt CollectionsFY 2008 - 2013 (in millions)

Why Join SRP? What are the Benefits? • Ability to collect millions of dollars in unpaid debt annually • Access to federal non-tax payment offsets for the UIC and state tax programs • Recovery of valuable funds for federally sponsored programs • Opportunity to maximize your states’debt collection potential

Centralization • While centralizing a state’s debt portfolio and payment streams is ideal, it is not a requirement for participation in the program. TOP works with states to find a way to make the program work for their agency. Legislation • Fiscal Service is committed to assisting states with the process of obtaining legislation. In doing so, we provide: • Sample legislation and support from the Fiscal Service legal team • a Legislative Forum for State Attorney Generals/staff Funding Technology • States face challenges in funding new technology to connect with TOP in the current economic climate. • TOP is exploring options for Fiscal Service to support states. Other

The TOP Partial Match Process • Partial match occurs when the social security number (SSN) or employer identification number (EIN) of a TOP debtor matches the SSN or EIN of a payee, but the debtor’s name does not match the payee’s name. • States can obtain a list of these matches by requesting a Debtor Locator Report (DLR) from TOP. • If your state can verify that the individual or entity receiving the payment is the same individual or entity who owed the debt, your state may add the newly identified name variation to TOP as an alias for future payment offset.

TOP Legislation/Regulation Checklist for States Essential Items: While states must abide by all the terms of the reciprocal agreement, the following are most often affected by state legislation: • Authority to offset state tax refunds- If the state issues any tax refunds, they must be subject to offset to collect federal debts. • Authority to offset other state payments - Legislative authority should be broad enough to include all state payments specified in the reciprocal agreement. • Authority for appropriate state official to submit state debts to TOP- TOP generally only accepts one or two points of connection with a state; so the authorized official(s) should be the officials that are capable of submitting the debt. • Authority for Fiscal Service to deduct a fee from offset collections- Federal law requires that Fiscal Service charge a fee to cover its costs of running the TOP program. Fiscal Service withholds a portion of each collection it makes from a federal payment for a state as its fee. States are free to add that fee amount to the debt balance, if state law authorizes it. • No authority to charge Fiscal Service a fee- Federal law does not permit Fiscal Service to pay a fee to the states when the state offsets a payment to collect a federal debt. • Due process- State law cannot require Fiscal Service or federal agencies to provide different due process from that set forth in the agreement and in 31 CFR 285.6.

TOP’s New Web ClientComing December 2013! • DMS is developing a new system to replace the current 15-year old system that will improve TOP efficiencies and increase TOP collections by enabling: • Increases in payment streams that can be offset • Increases in debt volume that can be collected by offset • Improve matching logic For TOP users this change will appear seamless, as the new TOP Web Client does not require any system changes of users.

Benefits of TOP’s New Web Client • The new web client version will include the following benefits for users: • Newly Enhanced User Screens • Ability to view debt/debtor information in one place to include: Offset Activity, Non Offset Activity, Agency Refund and Reversal Activity • Access to information on the File Receipt, Processing Status and Processing Statistics for Creditor Agencies • Ability to view captured information for bypassed payments fully matched to a debt • Capability to set bypass and override at the payment agency level Sign up online for TOP’s new Web Client training at www.fms.treas.gov/debt/training.html.

Expanding SRP Program TOP is seeking to identify new debt and payment streams from states currently in the SRP and those planning to join. Specifically, to identify: • potential debt streams that may require statutory or regulatory changes • potential payment streams that may require statutory or regulatory change

Working with States to Help Them Understand State Debts in TOP and How They AffectFederal Payments • State Debts in TOP Process: • TOP will offset a payment when the Taxpayer Identification Number (TIN) of a state agency receiving a payment is the same as the TIN of the state agency owing the debt. • TOP sends a letter notifying the payee state agency of the offset, if available. If not, TOP will use the debtor agency address. • TOP Report Designed for States • Treasury Offset Division (TOD) can provide your state with a report to help identify debts owed by state agencies, and assist you with the resolution and payment of these debts. • A written authorization from your state’s Comptroller is required for TOD to release this information at the beginning of each month.

Working with States to Help Them Understand State Debts in TOP andHow They Affect Federal Payments (2) • New Online information Provided for States: • How to resolve debts owed to the federal government • Frequently Asked Questions • A link to State Comptrollers on NASACT’s website Visit: www.fms.treas.gov/debt/TOP_state_debts.html • Working together with AGA, States and Federal Agencies to develop new pilots and solutions.

Increasing Communication and Soliciting Feedback with States TOP wants to hear directly from states about their challenges, experiences, best practices, and program recommendations for SRP. These are some of the new ways we are communicating with states: • Annual Report to the States • Offsets Matter – TOP’sbi-monthly news for states • Quarterly Meetings with Participating States • Industry Conferences and Meetings • Individual State Executive Meetings • Enhanced Customer Relationship Engagement (Pre and Post Implementation) View Offsets Matter online at www.fms.treas.gov/debt/offsetsmatter.html

The District of Columbia James Keifer Deputy Director, Compliance Administration

The District of Columbia • TOP participant since 1997 • Implemented the Reciprocal Offset Process in March 2013 at a cost of $401,695 • Certified 43,845 Non-income tax debts, as new offset candidates, valued at $63 million • $15.6 million collected in the first six months of participation

Debt Types Added • Previously certified with TOPfor Refund Offset were Individual Income Tax, Corporate Income Tax and Un-Incorporated Franchise Tax debts. • Non-Income Tax Debts added for Administrative Offset: • Sales and Use Tax • Withholding Tax • Personal Property Tax • Motor Fuel Tax • The District’s Ballpark Fee • Specialized Events and Specialized Sales

Working Towards … • Certifying debts for Administrative Offset for the following City Agencies: • Employment Security Administration • Central Collections Unit • Adding additional offset eligible payment sources for the State Payment Offset

Why the District of Columbia was Interested in Participating in TOP • Enhanced the District’s ability to resolve liabilities where 40% of its outstanding tax debt resides beyond its borders. The State Reciprocal Program, unlike TOP, is not limited to collecting from residents living within its legal borders, it allows collecting from debtors regardless of where they reside. • The Federal Government is the District’s largest employer. • We witnessed the pilot program successes of neighboring Maryland.

What the District of Columbia was Doing • In the fall of 2009, the District had an automated tax refund offset process to satisfy city government debts, and … • We participated in TOP • The District did not have an automated intercept program to capture internal D.C. Government payments.

What a Closer Look Found • Our internal intercept programs were inadequate. We did not have the necessary legislative support and did not have an adequate IT platform to identify and process intercepts • The Treasury Offset Program (TOP) IT platform would need a complete re-design to accommodate the additional debt types and processing schedules • The City-wide vendor payment accounting system, in its current state, was not capable of processing payment offsets.

With So Much to Consider – the District of Columbia Ran a Test • TOP suggested that we provide them a file of debts eligible under the program guidelines • In April, 2010, we submitted a limited file with a debt balance of $21 million • TOP matched our debt file against their January 2010 payment file, and the unexpected result … 1,596 payment offsets valued at $4,001,978.63 • A strong argument for DC to participate in the program

District of Columbia Addresses the Challenges • Amended the District Tax Code to permit D.C. Treasury Offsets • Developed an automated levy process to capture City contract payments to satisfy tax debts • Realizing additional collections of $2 million annually

District of Columbia Addresses the Challenges (2) • Introduced legislation to allow the District to participate in Treasury’s State Reciprocal Program. A Bill was drafted and sent to the City Council in November 2010 to amend chapter 1 of title 47 of the D.C. Official Code to provide authority for collecting debts through the United States Treasury Offset Program; authorizing the Chief Financial Officer to enter into an agreement with the Secretary of the Treasury, specifying reduction and offset of payments for collection of debt; authorizing payment of a fee to the Secretary of the Treasury; authorizing agency participation. • Used Maryland’s legislative code as a model • D.C. Code Section 47-143 became effective on April 8, 2011.

District of Columbia Addresses the Challenges (3) • Program(s) Development • Two accounting systems • Tax based processing system (TAS) • Debt management • Tax refund processing • Citywide System of Accounting and Reporting (SOAR) R*STARS • Contract Vendor payment distributions

District of Columbia Addresses the Challenges (4) • Identify all of the players • Multiple City Agencies • Multiple Administrations within each Agency • Dedicated programming resources within each Agency • Conflicting priorities and vision