Download

1 / 65

650 likes | 905 Vues

Asset Prices and Interest Rates. In this section, you will learn:. the classical theory of asset prices, which uses present value to determine the price of an asset that provides a stream of payments to its owner how asset-price bubbles and crashes work, and examples of both

E N D

In this section, you will learn: • the classical theory of asset prices, which uses present value to determine the price of an asset that provides a stream of payments to its owner • how asset-price bubbles and crashes work, and examples of both • two ways to measure bond returns/yields • about the relation of bond terms and yields, and how to use this relationship to predict future interest rates

INTRODUCTION:Valuing income streams • Assets provide future income to their owners. • Coupon bonds provide fixed coupon payments until maturity, then face value upon maturity • Stocks pay dividends while owned, then proceeds of the sale when sold • To determine the price of an asset, must figure out the value of these income streams. • To do this, we use the concepts of present value and future value…

Future value • The future value of a dollar today is the number of dollars it will be worth at some future time. • Example: i = interest rate in decimal form = 0.06$100 today is worth… $100 x (1+0.06) = $106.00 in one year $100 x (1+0.06)2 = $112.36 in two years $100 x (1+0.06)5 = $133.83 in five years

Future value • Notation: FV = future value = the value of an amount in the future PV = present value = the value of the amount in the present n = number of years in the future • Formula for future value: $FV = $PV x (1 + i)n

Present value • The present value of a dollar in the future is the number of dollars it is worth today. • Solve $FV = $PV x (1 + i )n for $PV: • Formula for present value: • Example: present value of $100 to be received in one year $FV $100 1 + 0.06 (1 + i)n $PV = = $94.34 =

NOW YOU TRY:Present Value Assume i = 0.04 for borrowing and saving. What’s the present value of $500 to be received in… a. one year? b. two years? c. twenty years?

ANSWERS:Present Value The present value of $500 to be received in… a. one year: b. two years: c. 20 years: = $480.77 $500 $500 $500 (1 + 0.04)20 1 + 0.04 (1 + 0.04)2 = $462.28 = $228.19

NOW YOU TRY:Present Values and Interest Rates What is the present value of $500 to be received in two years if the interest rate is: a. i = 0.04 b. i = 0.08 c. i = 0.12

ANSWERS:Present Values and Interest Rates Present value of $500 to be received in two years: a. If i = 0.04, b. If i = 0.08, c. If i = 0.12, = $462.28 $500 $500 $500 (1 + 0.04)2 (1 + 0.08)2 (1 + 0.12)2 = $428.67 = $398.60

Present values and interest rates • A higher interest rate reduces the present value of future money. • When the interest rate is higher, you don’t need to save as much today to end up with a particular amount in the future.

NOW YOU TRY:Valuing a series of payments • A share of Google stock will pay a dividend of $5 in one year, $8 in two years, and $10 in three years. The interest rate is i = 0.05. • Find the present value of each payment. • Add them up to get the present value of the series of payments.

NOW YOU TRY:Valuing a series of payments PV of $5 in one year = $5/(1.05) = $4.76 PV of $8 in two years = $8/(1.05)2 = $7.26 PV of $10 in three years = $10/(1.05)3 = $8.64 The PV of the series of payments is the sum of these amounts: $4.76 + $7.26 + $8.64 = $20.66

Formula for valuing a series of payments • The series of payments is: $X1 in one year, $X2 in two years, … $XT in T years • The present value of this payment series equals $X2 $X1 $X3 $XT (1 + i)1 (1 + i)2 (1 + i)3 (1 + i)T + + + … +

Payments forever • A perpetuity is a bond that pays interest forever but never matures. • If the payment is $Z each period, the PV equals $Z $Z $Z $Z (1 + i)1 (1 + i)2 (1 + i)3 i + + + … =

Payments that grow forever • The payment is $Z in one year, then grows at rate g forever. • PV of this payment stream equals $Z(1+g)1 $Z(1+g)2 $Z $Z (1 + i)1 i – g (1 + i)2 (1 + i)3 + + + … =

The Classical Theory of Asset Prices • Classical theory of asset prices says asset price = p.v. of expected asset income • If asset’s price is below p.v. of expected income, everyone will buy, driving the price up. • If asset’s price is above p.v. of expected income, current owners will sell, driving the price down. People determine asset values using expectations/forecasts when future income is unknown.

NOW YOU TRY:Pricing a bond Use the classical theory to determine the price of a Ford Motor Company bond with these characteristics: • Bond matures in 2 years • Face value (paid upon maturity) = $10,000 • Two coupon payments of $250 paid in 1 and 2 years, respectively • i = 0.07

ANSWERS:Pricing a bond First, determine PV of each payment: paymentpresent value 1st coupon $250/(1.07)1 = $ 233.64 2nd coupon $250/(1.07)2 = $ 218.36 face value $10,000/(1.07)2 = $8,734.39 $9,186.39 Price of bond equals sum of PV of all payments

Formula for price of a coupon bond • Notation:F = face value, C = annual coupon payment, T = years to maturity • Bond price equals

Formula for price of a stock • D1 = dividend expected in one year,D2 = dividend expected in two years, etc. • Stock price equals

NOW YOU TRY:Pricing a stock with growing dividends • The interest rate is 5%. • IBM stock pays annual dividends that start at $10 next year and grow 3% every year thereafter. • Find the price of IBM stock.

ANSWERS:Pricing a stock with growing dividends • Use the formula for the present value of a series of payments that grows forever: • Set i = 0.05, g = 0.03, and $Z = dividend next year = $10 • Answer: the price of IBM stock equals $Z(1+g)1 $Z(1+g)2 $Z $10 $Z 0.05 – 0.03 (1 + i)1 i – g (1 + i)2 (1 + i)3 + + = $500 + … =

The Gordon Growth Model • due to Myron Gordon (1959). • D = dividend next year,g = expected growth rate of dividends,i = interest rate D i – g Stock price =

What determines expectations? • The classical theory assumes rational expectations – people optimally use all available information to forecast future variables like dividends. • Example: auto stocks in a recession • If economy enters a recession, auto sales fall sharply. • People will lower their forecasts of automakers’ future earnings. • Automakers’ stock prices fall.

What is the relevant interest rate? • The more uncertain people are about an asset’s future income, the riskier the asset. • People prefer “safe” future dollars to risky ones, so the interest rate used to price assets must be adjusted for risk. Notation: isafe = safe (risk-free) interest rate = risk premium, a payment that compensates for risk i = i safe + = risk-adjusted interest rate • The riskier the asset, the greater the risk premium.

NOW YOU TRY:Flucuations in asset prices 1. In the context of the classical theory, think of an event that would cause a change in the price of Verizon Communications Inc. stock. 2. Would this event also change the price of Verizon Communications Inc. bonds?

ANSWERS:Flucuations in asset prices 1. Examples of things that would affect the price of Verizon Communications Inc. stock: • Verizon comes out with a new phone that everybody wants to buy. Expected earnings rise, causing stock price to rise. • An increase in the perceived riskiness of holding communications stocks, which increases the risk premium and risk-adjusted interest rate and lowers Verizon’s stock price. • The safe interest rate rises, reducing the present value of Verizon’s future earnings.

ANSWERS:Flucuations in asset prices 2. Would any of these things also change the price of Verizon Communications Inc. bonds? • The bond price will not change in response to news about Verizon’s future earnings, because income bondholders receive is fixed. (Exception: news that leads people to worry Verizon will default will raise the risk premium and risk-adjusted interest rate, causing bond price to fall.) • The bond price will change in response to a change in the safe interest rate, which alters the present value of future bond income.

Monetary policy and stock prices If the Fed unexpectedly raises the Fed Funds rate, • isafe rises, reducing present value of future dividends and hence stock prices • consumption and investment spending fall, lowering expected earnings and stock prices • risk premiums rise if people are uncertain about how badly companies will be hurt, which increases risk-adjusted interest rate and reduces stock prices • If the Fed’s move was expected, stock prices would have adjusted in advance.

Monetary policy and stock prices • Research by Bernanke and Kuttner:During the sample period 1989-2002, each 0.25 percent surprise increase in FF rate caused stock prices to fall 1 percent on average.

DISCUSSION QUESTION:Volatility of stocks vs. bonds • Based on what we’ve learned so far in this chapter, which do you think would be more volatile, stock prices or bond prices? Justify your answer.

Volatility of stock and bond prices • Stock prices tend to be more volatile than bond prices: • both are affected by changes in interest rates • but stock prices are more affected than bond prices by news that changes expected future earnings • What about short-term bonds vs. long-term bonds?

Volatility of short- vs. long-term bonds • Long-term bonds are more volatile than short-term bonds due to effect of interest rate changes.

Asset-price bubbles • Bubble: a rapid increase in asset prices not justified by interest rates or expected income. • If people believe a stock’s price will rise, they will buy the stock, causing the price to rise. • Any asset can experience a bubble, including houses, currencies, precious metals, and even tulip bulbs.

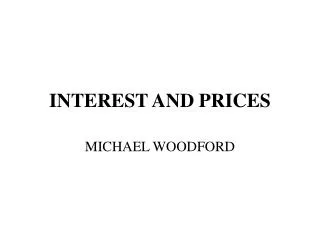

The Housing Bubble of the 2000s Low interest rates and relaxed lending standards helped fuel a surge in house prices. Case-Shiller 20-City Index, 2000 = 100 When the bubble burst, a wave of mortgage defaults helped create the financial crisis.

Using the P/E ratio to identify bubbles • Price-earnings (P/E) ratio: the price of stock divided by earnings per share • Suppose expected earnings are similar to recent earnings. Then, a high P/E means price is high relative to expected earnings. • In the classical theory, this would require falling interest rates. If rates are not falling, must be a bubble. • Problem: expected earnings may be different than recent earnings

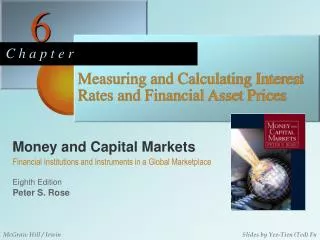

1990-2003: The Tech Boom and Bust A likely bubble in stocks, especially tech stocks DJIA (left scale) NASDAQ(right scale)

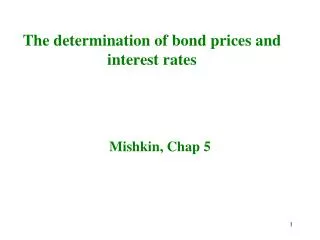

2003-2010: Recovery, Financial Crisis, Aftermath Dow Jones Industrial Average Stock prices fell sharply during the financial crisis

Asset-price crashes • Crash: a rapid drop in asset prices not justified by interest rates or expected income. • Crashes often follow bubbles. • When a crash starts, panic sets in, more people sell, and prices plummet.

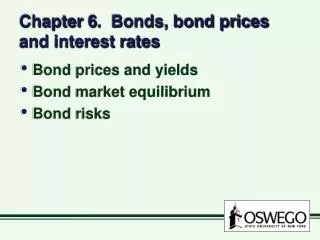

1929: The First Big Crash % change in DJIA on 10/28/1929: –13% 9/30/1929 to 3/30/1933: –84% Dow Jones Industrial Average

1987: The Second Big Crash Dow Jones Industrial Average Stock prices fell 23% on October 19, 1987.

Crash prevention • Margin requirements: limits on the amount people can borrow to buy stocks • a response to the 1929 crash • intended to reduce bubbles • Circuit breakers: requirements that temporarily halt trading if prices fall sharply • a response to the 1987 crash • intended to reduce panic selling, giving people time to calm down and assess the value of their stocks

Measuring interest rates on bonds • What is “the interest rate” on the following bond? $4721.09 = price to purchase bond today $5000.00 = face value paid upon maturity in 2 years $100.00 = annual coupon payment (starting in one year) • One measure of the interest rate is theyield to maturity (YTM): the interest rate that equates the price of a bond with the present value of payments from the bond.

Measuring interest rates on bonds • For the bond on the previous slide, the YTM is the interest rate that solves this equation: • Directly solving for YTM is generally not possible (except for zero-coupon bonds), so must either • use financial calculator, or • pick an interest rate, plug it in and see if it works; if not, try a different interest rate

NOW YOU TRY:Determining Yield to Maturity • In our example, the YTM is the value of i that solves this equation: • Plug i = 0.04 into the right hand side. • If the result equals the left hand side, you have found the YTM. • Else, adjust i up or down by 0.01 and try again. • Continue until you find YTM.

ANSWERS:Determining Yield to Maturity • First, try i = 0.04: • At i = 0.04, p.v. of payments > bond’s price, so YTM must be greater than 0.04. Try 0.05. • At i = 0.05, p.v. of payments = bond’s price, so YTM = 0.05.

The Rate of Return • Return on an asset: the capital gain or loss on an asset you own plus any payment you receive • Capital gain: the increase in your wealth from an increase in the asset’s price • Capital loss: the decrease in your wealth from a decrease in the price

The Rate of Return • Return on an asset: the capital gain or loss on an asset you own plus any payment you receive Return = (P1 – P0) + X, where P0 = price paid for asset, P1 = market price after one year, X = payment • Rate of return: return as a percentage of price

Rate of Return vs. Yield to Maturity • The most relevant interest rate is • YTM if holding the bond to maturity • Rate of return if selling the bond before maturity