Connections

2012 IPWEA Public Works Infrastructure Conference Leading Edge Infrastructure Management Session 7B – Connecting Asset Management to Financial Management Ian Mann Director CT Management Group.

Connections

E N D

Presentation Transcript

2012 IPWEA Public Works Infrastructure ConferenceLeading Edge Infrastructure Management Session 7B – Connecting Asset Management to Financial Management Ian MannDirector CT Management Group

CT Management Group is a multi-disciplinary consulting company servicing Local Government across Australia. • We can provide support to Councils in the areas of: • Asset Management • Service Planning • Financial Management • Governance • Organisational Development • Human Resource Management • Environmental Management • Contract Management • Project Management • Community Development • Emergency Management • We also provide short and long term professional placements into Councils.

Measuring Financial Performance Balance Sheet ($ ,000) Current Assets 80,000 Non-Current Assets 1,660,000 Total Assets 1,740,000 Current Liabilities 34,000 Non Current Liabilities 4,000 Total Liabilities 38,000 Equity 1,702,000 Income Statement ($ ,000) Recurrent Income 110,000 Recurrent Expenditure 96,000 Depreciation 12,000 Total Recurrent Expenditure 108,000 Surplus/Deficit 2,000

Financial Sustainability Today Looking Back Looking Forward Income Statement – Accounting Standards ($ ,000) Recurrent Income 110,000 Recurrent Expenditure 96,000 Depreciation 12,000 Total Recurrent Expenditure 108,000 Surplus/Deficit 2,000 Long Term Financial Plan – Cash Based Year 1 ($ ,000) Recurrent Income 110,000 Recurrent Expenditure 96,000 AAAC 14,000 Total Recurrent Expenditure 110,000 Surplus/Deficit 0

Value of Assets Today Looking Back (Balance Sheet) Looking Forward (LTFP) ValueB = QuantityB X Unit RateB ValueF = QuantityF X Unit RateF QuantityB = QuantityF Unit RateB = Fair Value or (Current Replacement Cost) Unit RateF = Current Replacement Cost Victoria Unit RateB = Fair Value or (Current Replacement Cost – Green Fields) Unit RateF = Current Replacement Cost (Brown Fields)

Useful Life of the Asset Today Looking Back (Balance Sheet) Looking Forward (LTFP) Useful LifeB = AgeB + Remaining LifeB Useful LifeF = AgeF + Remaining LifeF AgeB = AgeF Remaining LifeB = Remaining LifeF Remaining Life determined from condition assessment

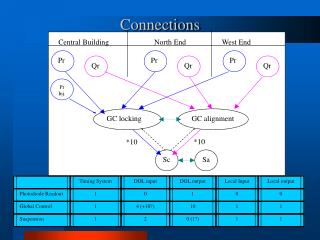

Consumption of Assets Today Looking Back (Balance Sheet) Looking Forward (LTFP) Depreciation RateB = ValueB / Useful LifeB Average Annual Asset ConsumptionF = Value F / Useful LifeF = QuantityB X Unit RateB / Useful LifeB (Fair Value or Current Replacement Cost [Brown Fields]) = QuantityF X Unit RateF / Useful LifeF (Current Replacement Cost [Brown Fields]) Victoria $ $ = QuantityB X Unit RateB / Useful LifeB (Fair Value or Current Replacement Cost [Green Fields]) Asset Value Asset Value = QuantityF X Unit RateF / Useful LifeF (Current Replacement Cost [Brown Fields]) Valuation – Fair Value Useful Life Useful Life Time Time Valuation – Current Replacement Cost

Long Term Planning Today Looking Back Looking Forward Income Statement – Accounting Standards ($ ,000) Recurrent Income 110,000 Recurrent Expenditure 96,000 Depreciation 12,000 Total Recurrent Expenditure 108,000 Surplus/Deficit 2,000 Long Term Financial Plan – Cash Based Year 1 Year 2 Year 3 Year 4 ($ ,000) ($ ,000) ($ ,000) ($ ,000) Recurrent Income 110,000 110,000110,000110,000 Recurrent Expenditure 96,000 96,00096,00096,000 AAAC 14,00014,00014,00014,000 Recurrent Expenditure 110,000 110,000110,000110,000 Surplus/Deficit 0 000 $ $ Asset Value Asset Value Valuation – Accounting Standards Valuation – Current Replacement Cost Useful Life Useful Life Time Time

Sustainable Renewal Funding Looking Back Looking Forward Income Statement – Accounting Standards ($ ,000) Recurrent Income 110,000 Recurrent Expenditure 96,000 Depreciation 12,000 Total Recurrent Expenditure 108,000 Surplus/Deficit 2,000 Long Term Financial Plan – Cash Based Year 1 Year 2 Year 3 Year 4 ($ ,000) ($ ,000) ($ ,000) ($ ,000) Recurrent Income 110,000 110,000110,000110,000 Recurrent Expenditure 96,000 96,00096,00096,000 Renewal Expenditure 11,00011,000 9,000 8,000 Recurrent Expenditure 107,000 107,000 105,000 104,000 Surplus/Deficit 3,000 3,000 5,000 6,000 $ Asset Value Valuation – Accounting Standards Today Useful Life Time

Renewal Gap Looking Back Looking Forward Income Statement – Accounting Standards ($ ,000) Recurrent Income 110,000 Recurrent Expenditure 96,000 Depreciation 12,000 Total Recurrent Expenditure 108,000 Surplus/Deficit 2,000 Long Term Financial Plan – Cash Based Year 1 Year 2 Year 3 Year 4 ($ ,000) ($ ,000) ($ ,000) ($ ,000) Recurrent Income 110,000 110,000110,000110,000 Recurrent Expenditure 96,000 96,00096,00096,000 Renewal Expenditure 4,0004,0004,0004,000 Recurrent Expenditure 100,000 100,000100,000100,000 Surplus/Deficit 10,000 10,00010,00010,000 Renewal Gap 7,000 7,000 5,000 4,000 $ Asset Value Valuation – Accounting Standards Today Useful Life Time

What can we influence? Income / Expenses ($ ,000) Recurrent Income 110,000 Recurrent Expenditure 96,000 AAAC 12,000 Total Recurrent Expenditure 108,000 Surplus/Deficit 2,000 Rates and Charges Services Provided – Levels of Service Internal Costs Number of Assets Maintenance Regime

Learnings • Have one asset register which includes all your assets • Value your assets based on best practice requirements • In Victoria recognise both Green Fields and Brown Fields • May need to retain multiple values for each asset • Remaining useful life based on condition • Review remaining life if conditions or designs change • Use condition as a basis for future asset renewal funding • Ensure that the full asset renewal needs have been recognised in the forward capital works program and Long Term Financial plan • If not then be transparent and recognise any funding shortfall

Questions Ian Mann Director CT Management Group Mob: 0429 941 435 Email: ianm@ctman.com.au CT Management Group 152 Lt Malop Street PO Box 1374 Geelong 3220