Public Purpose Doctrine

This document explores the Public Purpose Doctrine, highlighting its constitutional basis and implications for taxation and property rights. It emphasizes that taxation should be used equitably for public purposes only, as stated in state constitutions. Key provisions include the prohibition of tax credits or loans to individuals without public vote and the requirement for just compensation in property taking for public use. Further, it discusses programs like Wilson's in Connecticut, which support inventors through government corporations, ensuring financial aid is fairly allocated.

Public Purpose Doctrine

E N D

Presentation Transcript

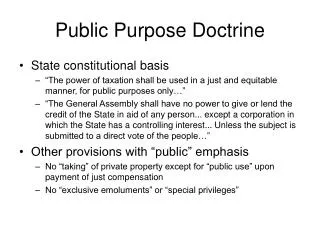

Public Purpose Doctrine • State constitutional basis • “The power of taxation shall be used in a just and equitable manner, for public purposes only…” • “The General Assembly shall have no power to give or lend the credit of the State in aid of any person... except a corporation in which the State has a controlling interest... Unless the subject is submitted to a direct vote of the people…” • Other provisions with “public” emphasis • No “taking” of private property except for “public use” upon payment of just compensation • No “exclusive emoluments” or “special privileges”

Public Purpose: approaches • Wilson (CT): • Structure of program • Fund: to support inventors, activities • Special gov’t corporation • Financial aid not otherwise available • Review requirements • Bond commission • Legislature explained