Uploaded by

anevay

0 SLIDES

231 VUES

0LIKES

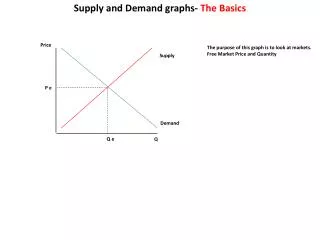

Price

DESCRIPTION

Price. AS Business Studies Marketing. Cost-based pricing. Cost plus pricing The business assesses the cost per unit and adds an amount on top (profit margin) of the calculated cost Unit Cost $10 50% mark up on the cost Selling Price . Cost Plus Pricing Exercise.

Download

1 / 0

Télécharger la présentation

Price

An Image/Link below is provided (as is) to download presentation

Download Policy: Content on the Website is provided to you AS IS for your information and personal use and may not be sold / licensed / shared on other websites without getting consent from its author.

Content is provided to you AS IS for your information and personal use only.

Download presentation by click this link.

While downloading, if for some reason you are not able to download a presentation, the publisher may have deleted the file from their server.

During download, if you can't get a presentation, the file might be deleted by the publisher.

E N D

Presentation Transcript

-

Price

AS Business Studies Marketing - Cost-based pricing Cost plus pricing The business assesses the cost per unit and adds an amount on top (profit margin) of the calculated cost Unit Cost $10 50% mark up on the cost Selling Price

- Cost Plus Pricing Exercise Unit Cost $250 20% mark up on the cost Selling Price Unit Cost $750 33.3% mark up on the cost Selling Price Unit Cost $400 75% mark up on the cost Selling Price

- Target Pricing The price is determined by a required rate of return on a certain level of output or sales A business sets a target on 100,000 units Total Cost of 100,000 units $1,000,000 Required return 30% Total Return Price per unit (1,300,000/100,000)

- Target Pricing Exercise Total Cost of 50,000 units $250,000 Required return 50% Total Return Price per unit ( / ) Total Cost of 100,000 units $1,800,000 Required return 25% Total Return Price per unit ( / ) Total Cost of 50,000 units $600,000 Required return 33.3% Total Return Price per unit ( / )

- Full Cost (Absorption Cost) Pricing The company attempts to calculate a unit cost for the product and adds a profit margin Output 10,000 Fixed Cost $100,000 Variable Cost $10 Total Variable Cost Total Cost of Production Average Cost (Unit Cost) Profit margin of 25% Selling price

- Full Cost Pricing Exercise Output 10,000 Fixed Cost $100,000 Variable Cost $10 Total Variable Cost Total Cost of Production Average Cost (Unit Cost) Profit margin of 25% Selling price

- Full Cost Pricing Exercise Output 25,000 Fixed Cost $100,000 Variable Cost $4 Profit Margin (25%) Output 80,000 Fixed Cost $400,000 Variable Cost $7 Profit Margin (50%)

- Contribution Cost Pricing Pricing does not try to allocate the fixed costs to specific products A firm will calculate the variable cost per unit and add an extra amount (the contribution) for fixed costs If enough units are sold then sales revenue will cover all fixed costs Unit Cost $5 Fixed Cost $750,000 Contribution $2.50 Selling Price Sales required to cover all costs

- Contribution Cost Pricing Exercise Variable Cost $10 Fixed Cost $1,500,000 Contribution $5 Selling Price Sales required to cover all costs Variable Cost $7 Fixed Cost $300,000 Contribution $3 Variable Cost $6 Fixed Cost $1,200,000 Contribution $6

- Select and explain a suitable pricing strategy for the following products New Range of Televisions Cinema Tickets New Fashion Magazine Rolex Watches Pepsi Cola

- What determines Prices? Costs of Production Number and strength of competitors in the market Price Elasticity of Demand Branding/ Firm reputation or image Whether the product does or does not have a USP How much the consumer is willing to pay

- Evaluate what is the most important factor in determining the price of Marlboro Cigarettes

- Answering the essay question Introduction: Key Terms Main body: Analyse each factor that determines price and relate to Marlboro. Each factor should be one paragraph. E.g. The costs of production are an important consideration for any business that is making a pricing decision. If the price Marlboro sets for its product does not cover the cost of producing it then with each sale the company will return a loss and will quickly fail. The difference between the cost of producing one unit and the selling price represents the firms profit margin. Evaluation: Answer the initial question. This should be the identification of the most important factor(s) with clear reasoned judgement for your choice

More Related