Download

1 / 5

50 likes | 152 Vues

IDBI Bank offers car loans with attractive interest rates & for upto 7 years. Calculate your eligibility and get a free EMI quote for your dream car.

E N D

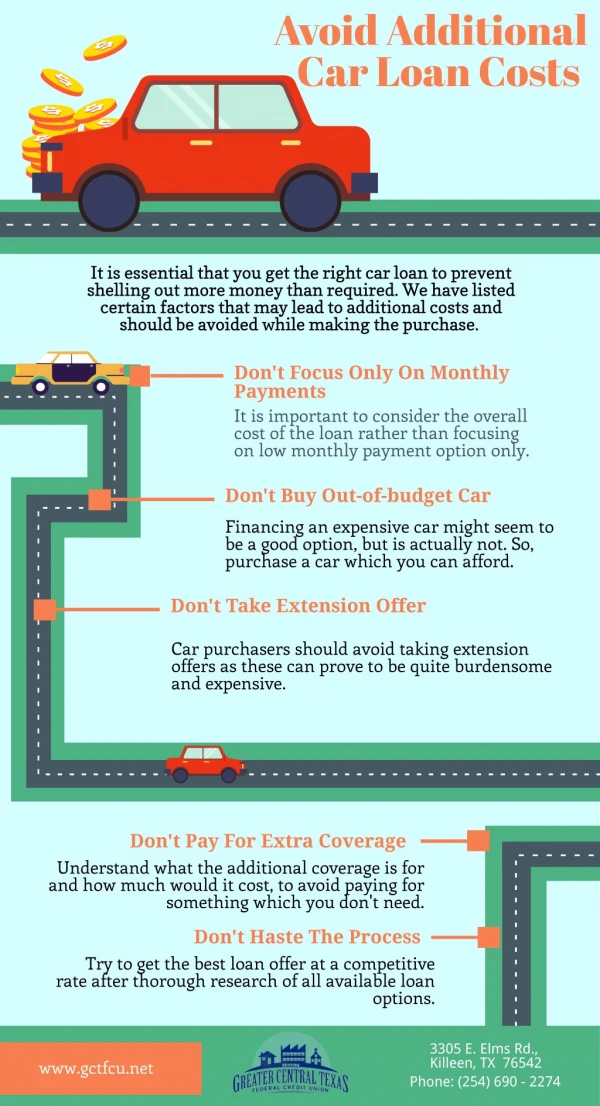

Pitfalls to Avoid When Buying A Car and Applying For Car Loan You walk into the office of the business manager with a swagger just like Vin Diesel. Why wouldn’t you? You have just made a sweet deal over your favourite car with successful price negotiation. Revel in the pride for a few seconds and then stop. It isn’t over. You could still be taken for a ride (pun intended). Purchasing a car is not as simple as handing over the money and taking the car. It involves paperwork, insurance deals, fine prints, hidden costs and a few other trolls lurking within the posh offices of the dealers and behind the smiles of the well- groomed executives of the car showrooms. Beware! A). Negotiate on the final payment. Do not settle for the offer that the dealer makes to you. Remember that the car salespersons work on commission. They will try to sell you the car at the highest cost possible for the car and with a

heavy rate of interest. It would be wise to negotiate for everything, from the cost to the interest rate to the EMIs. B). Knowledge is power. Become aware of your financial status and credit score to take charge of the negotiation process. Do not set foot in a car dealer’s office till you are fully aware of your financial capacity. Put your monthly expenses, down to the pin, in writing. Assess your income and expenditure, keeping contingency account intact. You can approach CIBIL to know your credit score. Check for the rates of interest offered in the market. Understand where you stand financially before you negotiate any deal on the car. This will also prevent you from not being taken in by the projected glitz and glamour and overspending.

C). Make the appropriate choice between cash rebate and low rate of interest. It cannot be emphasized enough that you need to be fully aware of your finances and know how to manage them before applying for any type of loan. This helps when you are offered a choice between cash rebate and a low rate of interest. Cash rebate means when a dealer offers you a lesser purchase price on the car but with no change in rate of interest. Thus, you can choose whether to buy a car for Rs. 3 lakhs at rate of interest of 12% or pay Rs. 2,70,000/- for the car at rate of interest of 14%. D). Buy the accessories and add-ons separately. When you buy add-ons and accessories, it adds to the salesperson’s commission. Check if you really need them. For instance, since most cars come with comprehensive warranties, you do not need to buy

another one. You can buy other accessories like window tinting, alarm systems, pin-striping and such others on your own at a much lesser cost. Also, say ‘No’ to health and life insurance offered by the dealer. Bottom line: Ask yourself (for every accessory) ‘do I really need this and if I do, can I get it cheaper elsewhere?’ E). Do not go for longer tenure as you may end up paying more than the car is worth and where the rate of interest is more than the monetary value of the car. This is a common mistake made by those who are uninformed about their finances and loan repayment terms when applying for a car loan. In a bid to meet usual monthly expenses, customers opt for a longer tenure with lower interest rate and EMI. Keep in mind that at the end

of the loan tenure, you will have paid more interest than what the car is worth. Thus, it is wiser to think in terms of the price of the car than the monthly expenses. Another way to beat them is to make a large down payment and taking a smaller loan. F). When buying a car from the manufacturer’s financial firm, be aware of the ‘dealer’s mark-up’. It means that even if you are getting a discount on the price of the car, you will have to pay a higher rate of interest for it. A part of this interest is a commission for the dealers. Source: http://blog.loanbaba.com/pitfalls-to-avoid-when-buying-a-car- and-applying-for-car-loan/