OVERHEADS

Learn about different types of overheads, their classification, allocation methods, and absorption techniques in costing systems. Explore the redistribution of overheads and their impact on financial reporting.

OVERHEADS

E N D

Presentation Transcript

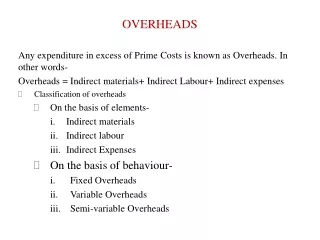

OVERHEADS Any expenditure in excess of Prime Costs is known as Overheads. In other words- Overheads = Indirect materials+ Indirect Labour+ Indirect expenses Classification of overheads On the basis of elements- Indirect materials Indirect labour Indirect Expenses On the basis of behaviour- Fixed Overheads Variable Overheads Semi-variable Overheads

On the basis of function- • Factory Overhead • Office & Administrative Overhead • Selling & Distribution Overhead. • Steps in Overhead costing- • Collection of overheads under standing order • Allocation of Overheads • Apportionment of Overhead • Absorption of Overhead • Over/Under absorption of overhead • Accounting for over/under absorption of overheads

Apportionment of overheads • Distinction between allocation and Apportionment • Apportionment of overheads- When costs are incurred for a particular cost centre then it is called allocation of overhead. • Apportionment of Overheads-On the other hand when costs are common to all department, then the costs are apportioned to the department on some equitable basis. • Basis of Apportionment Common ExpensesBasis of apportionment • Factory Rent, Rates& taxes Floor area Occupied • Insurance of Building Costs of building/Floor area

3) Depreciation of Building Cost of building/Floor area 4) Depreciation Of plant & Machinery Cost of Plant & machinery 5) Insurance of Stock Stock Value 6) Supervisor’s salary No of Workers 7) Canteen expenses/ Staff Welfare Exp No of Workers 8) Indirect Wages Direct Wages 9)Electric charges No of light point x wattages/ no of light point/Floor area 10) Stores Overhead Value of Material 11) General Expenses Working Hours/Direct wages. 12) Power H.P. of machine x Wattage H.P. of Machine

Re-distribution of Overheads: • Re-distribution of service department costs to production department. This may be • Direct service to Production Department • Reciprocal services • Methods of Re-distribution • Repeated method • Simultaneous equation.

Absorption of Overheads • Production Unit method • Direct material Costs Method • Direct labour Costs method • Percentage of Prime costs method • Labour Hour rate method. • Machine Hour rate method

Illustration: X.Ltd. has three production departments A, B and C and two service departments D and E. Following information relates to the month of January 2015: Rent-Rs 10000; Depreciation of machine- Rs 20000; Motive Power- Rs 3000; Indirect wages – Rs 23000; lighting- Rs 2400; Supervisor’s salary- Rs 16000. Additional Information: A B C D E Area Occupied (Sq. Ft) 2000 2500 3000 2000 500 Light points 10 15 20 10 5 Direct wages (Rs) 3000 2000 3000 1500 500 H.P. machine 60 30 50 10 -- No of workers 50 40 60 30 20 Value of Machines (Rs) 60000 80000 100000 5000 5000 Services rendered by department D and E to production department are in the ratio of 5:3:2 and 4:4:2 respectively

Statement Showing Distribution of Overheads Basis of di

ABSORPTION OF OVERHEADS • Absorption of overheads means estimation of overheads on some reasonable basis. • Various methods of overhead absorption are- (i) Percentage of Direct Material. (ii) Percentage of Direct Wages. (iii) Percentage of Prime Costs. (iv) Labour Hour Rate method. (v) Machine Hour Rate Method.

Estimated/ Budgeted Overhead Overhead absorption rate = ---------------------------------------- Absorption Base Overhead absorbed = Actual base x Absorption rate • Machine Hour Rate Method: It is basically an absorption rate of overheads under which factory overheads are absorbed in case where the production is pre-dominantly carried on through machines and the products are not uniform.

OVER/UNDER ABSORPTION OF OVERHEADS • Over Absorption- An over absorption occurs when overhead absorbed is more than the actual overheads incurred. • Under Absorption- an under absorption occurs when overhead absorbed is less than the actual overheads incurred. Treatment of Over/under absorption of Overheads • Transfer to Costing Profit & Loss account. • Carried to the next accounting year. • Adjusted the overhead absorption rate with a supplementary rate.

Overhead absorption for the departments Deptt A= Machine Hour x Machine hour rate = 14000 hrs x Rs 1.50 = Rs 21000 Deptt B = Direct Labour Hour x Hourly Rate = 3000 hrs x Rs 1.30 = Rs 3900 Deptt C = Direct Wages x Overhead % = Rs 6000 x 80% = Rs 4800 Deptt D = No. of Pieces x Overhead Rate = 950 x Rs 2.00 = Rs 1900