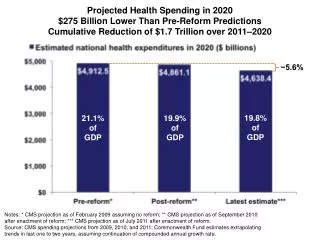

Download

1 / 10

100 likes | 202 Vues

Sections 5.6. Consider a loan being repaid with n periodic installments R 1 , R 2 , … R n which are not necessarily all equal. Then, the amount of the loan must be. n. . L = . v t R t. t = 1. An amortization schedule can be constructed from basic principles.

E N D

Sections 5.6 Consider a loan being repaid with n periodic installments R1 , R2 , … Rn which are not necessarily all equal. Then, the amount of the loan must be n L = . vtRt t = 1 An amortization schedule can be constructed from basic principles. A loan is being repaid at 7% effective interest with payments of $300 at the end of the first year, $280 at the end of the second year, $260 at the end of the third year, and so forth until the last payment of $80 is made at the end of the 12th year. Find (a) the amount of the loan and (b) the principal and interest in the 8th payment. (a) The amount of the loan is 300v + 280v2 + 260v3 + … + 100v11 + 80v12 = (240 + 60)v + (220 + 60)v2 + (200 + 60)v3 + … + (40 + 60)v11 + (20 + 60)v12 =

A loan is being repaid at 7% effective interest with payments of $300 at the end of the first year, $280 at the end of the second year, $260 at the end of the third year, and so forth until the last payment of $80 is made at the end of the 12th year. Find (a) the amount of the loan and (b) the principal and interest in the 8th payment. (a) The amount of the loan is 300v + 280v2 + 260v3 + … + 100v11 + 80v12 = (240 + 60)v + (220 + 60)v2 + (200 + 60)v3 + … + (40 + 60)v11 + (20 + 60)v12 = 12 – 7.94269 —————— 0.07 (Da)— 12| 20 + 60 = 20 + 60(7.94269) = a— 12| $1635.79 (b) The 8th payment is R8 = $160 The balance immediately after the 7th payment is B7 = p (Da)– 5| 20 + 60 a– 5|

A loan is being repaid at 7% effective interest with payments of $300 at the end of the first year, $280 at the end of the second year, $260 at the end of the third year, and so forth until the last payment of $80 is made at the end of the 12th year. Find (a) the amount of the loan and (b) the principal and interest in the 8th payment. (b) The 8th payment is R8 = $160 The balance immediately after the 7th payment is B7 = p (Da)– 5| 20 + 60 a– 5| The interest in the 8th payment is I8 = iB7 = p 20(5 – ) + 60(1 –v5) = a– 5| 20(5 – 4.10020) + 60(1 – 0.71299) = $35.22 The principal in the 8th payment is P8 = R8–I8 = 160.00 – 35.22 = $124.78

Consider a loan of amount L being repaid with n periodic installments R1 , R2 , … Rn which are not necessarily all equal. Also assume that each period the interest is paid directly to the lender and the remainder of the installment is deposited into a sinking fund. If the periodic interest rate on the loan is i, and the sinking fund earns periodic interest rate j, then the sinking fund deposit for the tth period is Rt– iL, and the amount of the loan L must be determined by L = (R1– iL)(1 + j)n – 1 + (R2– iL)(1 + j)n – 2 + … + (Rn– iL) = n Rt(1 + j)n – t – iL s – n|j t = 1 n n Rt(1 + j)n – t vjtRt L = = . t = 1 t = 1 1 + i 1 + (i – j) s – n| j a – n| j Multiply numerator and denominator by (1 + j)–n and then add and subtract 1 in the denominator.

Implicitly we have assumed that the sinking fund deposit each period is positive. In cases where at least one sinking fund deposit is negative, we must recognize that this implies that the amount of the loan has been increased (i.e., this additional amount is borrowed at rate i, not at rate j). A loan is being repaid at 8% effective interest with payments of $300 at the end of the first year, $280 at the end of the second year, $260 at the end of the third year, and so forth until the last payment of $80 is made at the end of the 12th year. However, each payment is divided into an amount to pay the interest on the loan directly to the lender, and an amount deposited into a sinking fund earning 7% effective interest to be used to pay back the loan amount. Find the amount of the loan. n The numerator must be the loan amount calculated in the previous problem. (Da)— 12|0.07 vjtRt 20 + 60 a— 12|0.07 L = = t = 1 = 1 + (i – j) 1 + (0.08 – 0.07) a – n| j a— 12|0.07

A loan is being repaid at 8% effective interest with payments of $300 at the end of the first year, $280 at the end of the second year, $260 at the end of the third year, and so forth until the last payment of $80 is made at the end of the 12th year. However, each payment is divided into an amount to pay the interest on the loan directly to the lender, and an amount deposited into a sinking fund earning 7% effective interest to be used to pay back the loan amount. Find the amount of the loan. n The numerator must be the loan amount calculated in the previous problem. (Da)— 12|0.07 vjtRt 20 + 60 a— 12|0.07 L = = t = 1 = 1 + (i – j) 1 + (0.08 – 0.07) a – n| j a— 12|0.07 $1635.79 = $1515.42 1 + (0.01)(7.94269)

Jones borrows $10,000 from Smith and agrees to repay the loan with 10 equal annual installments of principal together with the interest on the unpaid balance at an effective rate of 5%. At the end of five years, Smith sells the right to receive future payments to Collins at a price which produces a yield rate of 6% effective for Collins over the remaining 5 years. Find the price which Collins should pay. Balance 8000 7000 6000 5000 4000 3000 2000 1000 0 10,000 9000 Time 0 1 2 3 4 5 6 7 8 9 10 Principal Paid 1000 1000 1000 1000 1000 1000 1000 1000 1000 1000 Interest Paid 500 450 400 350 300 250 200 150 100 50 At the end of the 5th year, the present value of the remaining payments is (Da)– 5|0.05 50 + 1000 a– 5|0.05 At the end of the 5th year, the price which Collins should pay to produce a yield rate of 6% effective for Collins is

Jones borrows $10,000 from Smith and agrees to repay the loan with 10 equal annual installments of principal together with the interest on the unpaid balance at an effective rate of 5%. At the end of five years, Smith sells the right to receive future payments to Collins at a price which produces a yield rate of 6% effective for Collins over the remaining 5 years. Find the price which Collins should pay. At the end of the 5th year, the present value of the remaining payments is (Da)– 5|0.05 5000 = 50 + 1000 a– 5|0.05 At the end of the 5th year, the price which Collins should pay to produce a yield rate of 6% effective for Collins is (Da)– 5|0.06 = 50 + 1000 a– 5|0.06 5 – 4.21236 —————— 0.06 50 + 1000(4.21236) = $4868.73

Jones borrows $20,000 from Smith at a rate of 12% effective and agrees to repay the loan with a series of 25 installments at the end of each year, so that each installment is followed by one which is 1% greater. Find the amount of principal repaid in each of the first two installments. Letting R1 , R2 , … , R25 represent the installments, we have 25 1.01 —— 1.12 1 – ————— 0.12 – 0.01 R1 = $2379.50 B0 = 20000 = R1 Observe how the principal repaid in the first installment is negative, which implies that I1 = P1 = B1 = (0.12)20000 = 2400 the first payment is not large enough to cover the interest, and more money is being borrowed thereby adding to the balance. 2379.50 – 2400 = – 20.50 20000 – (– 20.50) = 20020.50

Jones borrows $20,000 from Smith at a rate of 12% effective and agrees to repay the loan with a series of 25 installments at the end of each year, so that each installment is followed by one which is 1% greater. Find the amount of principal repaid in each of the first two installments. Observe how the principal repaid in the first installment is negative, which implies that I1 = P1 = B1 = (0.12)20000 = 2400 the first payment is not large enough to cover the interest, and more money is being borrowed thereby adding to the balance. 2379.50 – 2400 = – 20.50 20000 – (– 20.50) = 20020.50 (1.01) 2379.50 = 2403.295 Observe how the principal repaid in the second and future installments is positive, which implies that the balance is decreased and will continue to decrease. R2 = I2 = P2 = B2 = (0.12)20020.50 = 2402.46 2403.295 – 2402.46 = 0.835 20020.50 – 0.835 = 20019.665 Look at Example 5.14 (page 177) in the textbook.