Download

1 / 44

440 likes | 623 Vues

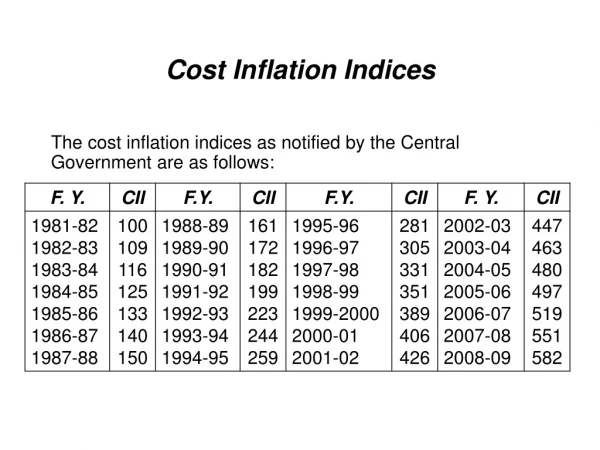

Cost Inflation Indices. The cost inflation indices as notified by the Central Government are as follows:. Computation of Capital Gains – short term and long term.

E N D

Cost Inflation Indices The cost inflation indices as notified by the Central Government are as follows:

Computation of Capital Gains – short term and long term Short term capital gains [S. 2(42B)] means capital gains arising from transfer of a short-term capital asset. Long term capital gains [S. 2(29B)] means capital gains arising from transfer of a long-term capital asset. Mode of Computation of Capital Gains [Section 48] *Cost of Acquisition (C.O.A) ** Cost of Improvement (C.O.I)

Notes: 1. Any sum paid on account of Securities Transaction Tax (STT) is not deductible in computing Capital Gains. 2. Indexed cost of acquisition or improvement shall be computed as follows :

If assessee acquires capital asset before 1.4.81 Note: COI before 1.4.81 is ignored.

Capital assets Summary Short term capital assets Long term capital assets Period of holding is 36 months or less Period of holding is more than 36 months Special cases: period of holding is more than 12 months Special cases: period of holding is 12 months or less 1.For computing the period of 36 months or 12 months, as the case may be, the date on which the asset was acquired is to be included while the date on which the asset is transferred is to be excluded. 2. Indexation on long term capital assets will not be allowed for bonds and debentures other than capital indexed bonds issued by the Government

Question- short term or long term capital asset Y purchases Debentures of a company on Mar 10, 2006.Debentures are listed on Cochin Stock Exchange with effect from Jan 1, 2008. Y transferred these debentures on Jan 5, 2009. We have to see the nature of capital asset on the date of transfer. As the debentures were listed on the date of transfer, the criteria of 12 months will be applicable. Hence it is a long term capital asset as the period of holding is more than 12 months.

Charge under the head ‘Capital Gains’ [section 45(1)] • Any profits or gains arising from the transfer of a capital asset is chargeable to tax as income of the previous year in which the transfer took place. • Two important conditions. • There is a capital asset. [The asset must be a capital asset at the time of transfer] • There is a ‘transfer’ of such capital asset.

Capital Asset [section 2(14)] According to Section 2(14), capital asset means property of any kind held by an assessee, whether or not connected with his business or profession, but does not include – • Any stock-in-trade, consumable stores or raw materials held for purpose of his business or profession. • Personal effects i.e. movable property held for personal use by assessee or his family member dependent on him. Exception of personal effects:(i.e following are capital assets) • Jewellery • Archaeological collections, • Drawings, Paintings, Sculptures and any work of art

Capital Asset [section 2(14)](contd) 3. Rural agricultural land i.e. Agricultural land in India not being a land situated _ Within the jurisdiction of a municipality or a cantonment board having a population of 10,000 or more according to the last preceding census; or _ In any notified area within 8 kms from the local limits of any municipality or cantonment board. 4. Gold Bonds issued by Central Government including the Gold Deposit Bonds issued under the Gold Deposit Scheme, 1999. 5. Special Bearer Bonds, 1991.

Question- Capital asset or not A.C installed at assessee’s residence • not a CA because it is personal and moveable A.C installed at business premises • CA because though it is moveable, it is not personal. A.C for a dealer in AC • not a CA because it is a stock in trade for the assessee.

Transfer [section 2(47)]: Transfer, in relation to capital asset, includes – a. sale, exchange or relinquishment of the asset; b. extinguishment of any rights therein; c. compulsory acquisition thereof under any law; d. maturity or redemption of zero coupon bond; e. conversion or treatment of such asset by the owner into stock in trade of business carried on by him; f. Any transaction involving allowing of possession of an immovable property to be taken or retained in part performance of a contract of the nature referred u/s 53A of Transfer of Property Act, 1882. g. any transaction (whether by way of acquiring shares in, or by way of becoming a member of, a co-operative society, company or other AOP or by way of any arrangement or agreement or in any other manner) that has the effect of transferring or enabling the enjoyment of, any immovable property.

Transfer [section 2(47)](contd) -:Case Laws:- 1. Reduction in face value of shares and consequent payment to the shareholder towards such reduction amounts to ‘transfer’, as it results in extinguishment of right in the shares held by the shareholder. – Kartikeya Sarabhai v. CIT [1997] 228 ITR 163 (SC). 2. Surrender of Preference Shares on redemption thereof amounts to ‘transfer’ as there is relinquishment by the shareholder of his rights in Preference Shares. – Anarkali Sarabhai v. CIT [1997] 224 ITR 422 (SC).

Transactions not regarded as transfer (sec 47) 1. Transfer of capital asset by way of gift or under a will or irrevocable trust. 2. Transfer of capital asset in total or partial partition of HUF.

Transactions not regarded as transfer (contd 1) 1Lakh Cost=0 5 Lakh 1.10.06 1.1.09 B C Sell Gift 1.10.90 Capital gains for B: A FVC = 5,00,000 Indexed COA = 1,12,139 1,00,000 * 582 (08-09) 519 (06-07) 3,87,861 (-) Option of taking FMV as on 1.4.81 is available if the previous owner acquired capital asset before 1.4.81

Transactions not regarded as transfer (contd 2) Cost=0 Cost=0 B C D Gift Gift Sell Who is the previous owner for C? A Previous owner means the last previous owner who actually paid for the asset. Hence Previous owner for C will be A from where cost and period Of holding will be taken.

Transactions not regarded as transfer sec 47 (contd 4) 3.Transfer of capital asset by holding company to its 100% subsidiary company or vice versa provided the transferee company is an Indian company.

Withdrawal of exemption sec 47A If any of the following events occur within 8 years from the date of transfer, the capital gains so exempted will be chargeable to tax in the year in which transfer took place • 1.The holding company does not continue to hold the whole of the share capital of the subsidiary company. • 2. The transferee company converts the capital asset into stock in trade.

Section 47 read with section 47A 1 lakh 03-04 5 lakhs Without attracting section 47A S 08-09 1990-91 sells Capital gains for S H FVC = 5 Lakhs (-) COA = 1 Lakh 4 Lakhs

Section 47 read with section 47A(contd) 1 lakh 03-04 5 lakhs After attracting section 47A S 3 lakhs 08-09 90-91 sells Capital gains for S Capital gains for H H FVC = 5 Lakhs FVC = 3 Lakhs COA = 3 Lakh COA = 1 Lakh 2 Lakhs 2 Lakhs

Steps for computing capital gain • 1)Identify whether the given asset is a capital asset or not as per section 2(14) • 2) Identify whether the given transaction is a taxable transfer or not as per section 2(47) read with section 47. • 3) Find out whether the CA is LT or ST. • 4) In certain situations, while counting the POH of capital asset, we include POH of previous owner also. Section 2(42A) • 5) In certain situations, while calculating the COA of capital asset, we consider cost to the previous owner.Section 49. • 6) However indexation of COA will always start from the current assessee.

Intangible Assets Cost of acquisition and cost of improvement in case of certain intangible assets

Conversion of capital asset into stock in trade sec 45(2) • 1.If a capital asset is converted into stock in trade, it is considered as a transfer as per section 2(47) in the year of conversion.However the resulting capital gain is taxable in the year of transfer of the converted stock. • 2. The period of holding of the converted asset should be calculated from the actual date of purchase of capital asset till the date of conversion.Indexation of COA and COI will also be till the year of conversion.

Conversion of capital asset into stock in trade sec 45(2)(contd 2) • 3. FMV on the date of conversion is considered as the full value of consideration for calculating capital gains. The same FMV is considered as purchase price of stock for calculating income from business.

Compulsory acquisition of capital asset • Where asset has been compulsorily acquired under any law or the consideration for transfer is determined by RBI or Central Govt, it is regarded as transfer. • However the resulting capital gains will be taxable in the year of receipt of initial compensation or part thereof • The POH will be calculated till the year of compulsory acquisition. Further COA and COI will be indexed till the year of transfer and not till the year of receipt of compensation.

Compulsory acquisition of capital asset (contd 2) • When enhanced compensation is received capital gains will be taxable in the year of receipt of enhanced compensation. • Capital gains will be ST or LT depending on the nature of original asset. • No COA and COI will be allowed as deduction as it has already been allowed once. But litigation expenses is allowed as expense on transfer.

1. Capital gains in case of transfer of asset on which depreciation has been allowed under Section 32(1)(ii) in respect of ‘block of assets’ [Section 50] : The capital gains shall be computed as follows : Block of assets ceases to exist or WDV becomes negative or both[Section 50(1)]: Capital Gains in case of Depreciable Assets [section 50 & 50A]

Capital Gains in case of Depreciable Assets [section 50 & 50A] 2. Transfer of capital assets of Power sector units on which depreciation allowed u/s 32(1) (i) [Section 50A]: (a) If WDV of the asset exceeds Moneys Payable on transfer of such assets: Terminal depreciation under Section 32(1) (iii) = WDV of such asset – Moneys Payable (b) If Moneys Payable exceeds WDV of the asset: Then, if - Moneys payable doesn’t exceed actual cost : Balancing charge u/s 41(2) = Money Payable – WDV Moneys payable exceeds Actual Cost : Balancing Charge u/s 41(2) = Actual Cost – WDV; and Short-term/Long-term Capital Gains = Moneys Payable – Actual Cost

CASES WHERE BENEFIT OF INDEXATION IS NOT AVAILABLE EVEN IN CASE OF LONG-TERM CAPITAL ASSETS: 1. Transfer of a bond or a debenture other than capital indexed bonds issued by the Government. 2. Transfer of undertaking or division in a slump sale under Section 50B. 3. Transfer of shares/debentures of an Indian company purchased by a non - resident in foreign currency. 4. Transfer of units purchased in foreign currency by an assessee covered under Section 115AB. 5. Transfer of bonds or shares purchased in foreign currency by an assessee covered u/s 115AC. 6. Transfer of global depository receipts by a resident employee of an Indian company u/s 115ACA. 7. Transfer of securities by foreign institutional investors under Section 115AD. 8. Transfer of a foreign exchange asset by a non-resident Indian under Section 115D.

Cases where Fair market Value shall be treated as full value of consideration 1.In case of conversion of capital asset into stock in trade. 2.Transfer by way of distribution of capital assets by a firm or AOP 3.In case of barter exchange 4. Assets distributed in kind in case of liquidation of a company.It is taxable in the hands of shareholder as sale consideration.

EXEMPTIONS IN RESPECT OF CAPITAL GAINS AVAILABLE ONLY TO INDIVIDUAL AND/OR HUF ASSESSEES [Section 54, 54B and 54F]

Exemptions in respect of capital gains available only to individual and/or HUF assessees [section 54, 54B and 54F] Note: Important points on exemption under Section 54 and 54F – Purchase/Construction of a Portion: Purchase or consideration of a portion of the house is eligible for exemption – CIT v. Chandanben Maganlal [2000] 245 ITR 182 (Guj.). E.g. If an assessee purchases 15% undivided share in a house property, exemption will be available. However, mere construction by way of extension of old existing house is not eligible for exemption. CIT v. Pradeep Kumar [2006] 153 Taxman 138 (Mad.) Purchase of co-owner’s interest : In case of property owned by co-owners, the payment made by one co-owner to get the full ownership by release of the interest of other co-owners amounts to ‘purchase’ by such co-owner and is eligible for exemption. CIT v. Aravinda Reddy [1979] 120 ITR 46 (SC). Registration not pre-condition: If assessee has purchased house and acquired its possession and control, he will be eligible for exemption even if such purchase is not registered as per Registration Act, 1908.

Exemptions in respect of capital gains available to all assessees [section 54D, 54EC, 54G and 54GA]

Transfer of depreciable assets held for more than 36 months – Exemption u/s 54EC available: Section 50 nowhere mentions that the depreciable assets are short term capital assets but only states that capital gains arising from transfer of depreciable asset shall be deemed to be arising out of transfer of short term capital asset. Section 54EC is independent section and exemption therein is available if there is a transfer of long term capital asset and consideration is invested in specified assets within time limit. Therefore, depreciable assets held for more than 36 months are long-term capital assets and capital gains arising therefrom will be eligible for the benefit envisaged u/s 54EC – CIT v. Assam Petroleum Industries P. Ltd. [2003] 131 Taxman 699 (Gau.) Extension of time in case of compulsory acquisition [Section 54H] : Where transfer of original assets referred to in Sections 54, 54B, 54D, 54EC and 54F, is by way of compulsory acquisition under any law, the period for acquiring new asset referred to in those sections or the period available under those sections for depositing or investing the amount of capital gain in relation to such compensation, which is not received on the date of the transfer, shall be reckoned from the date of receipt of such compensation.