Option Pricing Model

Option Pricing Model. Stephen Yan-leung Cheung Professor of Finance (Chair) Department of Economics and Finance City University of Hong Kong March 1, 2001. Two Main Pricing Models. Black-Scholes Model Binomial Model. 1. Black-Scholes Model. Option value is a function of: Stock price

Option Pricing Model

E N D

Presentation Transcript

Option Pricing Model Stephen Yan-leung Cheung Professor of Finance (Chair) Department of Economics and Finance City University of Hong Kong March 1, 2001

Two Main Pricing Models • Black-Scholes Model • Binomial Model

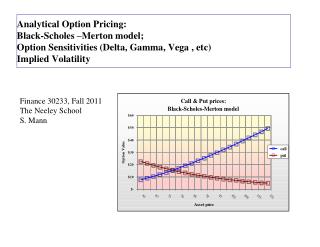

1. Black-Scholes Model • Option value is a function of: • Stock price • Strike price • Risk-free rate • Time to maturity of the option • Volatility • Dividends expected during the life of the option

1. Black-Scholes Model • What is meant by volatility? • It is the standard deviation of the stock return over a period of time.

1. Black-Scholes Model • Take observations P1, P2,……Pn over a period, where Pi is the closing price of stock • Stock return (Ri) is the proportionate change Ri = ln (Pi/Pi-1) • The historical volatility is the standard deviation of Ri (annualized)

1. Black-Scholes Model • Problems: • What is the “right” period for estimation? • Should be the most recent period that is generally commensurate with the expected option life.

1. Black-Scholes Model • Problems: • What is the “right” interval to calculate the stock return? • For annualized volatility, weekly return should be enough.

1. Black-Scholes Model • Problems: • What is the “right” price to calculate the stock return? • Weekly closing price or weekly highest price.

1. Black-Scholes Model • Problems: • New issues? • Historical volatility of similar company of the same industry.

2. Binomial Model • Another useful & popular technique for pricing a stock option is binomial pricing model • Assumption has to be made on the possible changes of stock price over the life of the option • The two methods give similar approximation and the same result under some circumstances

Biases in the Black-Scholes Model • Assumptions: • Stock price distribution • Volatility is constant • Large jumps in stock price Empirical result shows these problems seem to be less pronounced as an option’s life increases