Download

1 / 22

220 likes | 408 Vues

Job Order Costing. Management Accounting. Process costing. Used when a company uses many units of a single item Think of our example from yesterday (Chairs/Tables)

E N D

Job Order Costing Management Accounting

Process costing • Used when a company uses many units of a single item • Think of our example from yesterday (Chairs/Tables) • Unit Product Cost (Total Cost) = Total Manufacturing Costs (Fixed + Variable or Direct + Indirect) Divided by (/) Total Units Produced

Job Order Costing • When a company makes more than one product each job needs to be analyzed separately • Think of our second example of Product A and Product B • Often the allocation of Overheads (Indirect or Fixed Costs) will differ between products, remember product A and Product B

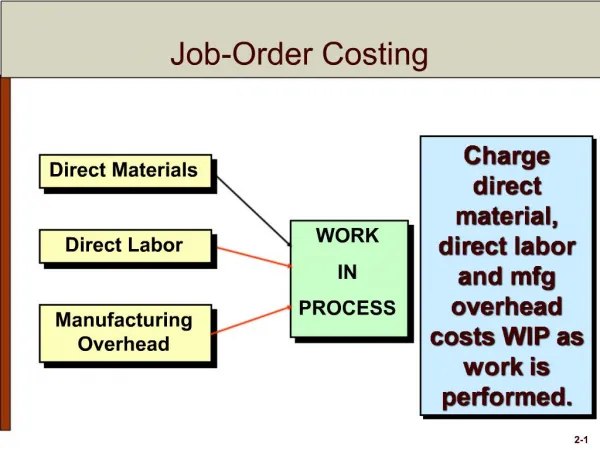

Accounting for Jobs • Generally each job will have its own Job Card (Job Cost Sheet/Job Bill) • The Job Card will collect all of the costs, both Direct and Indirect • Therefore you have to be able to measure all of the costs

Example Job Card • Turn to page75 and you will see how a job card is set out • At the top of the Job Card there is a lot of details about the Job’s point of reference • Secondly there is a breakdown of all of the components of the costs, these are familiar to you I am sure. • Finally there is a summary and a total for the cost of the whole job

Example • Copy the format of the Job Card onto a piece of paper and enter this information • The Job Number is 1234 • The Department is Pressing • The Item is a Saucepan • The Date initiated is today • The job is not completed yet • And we don’t know yet about units completed

Direct Materials for our Saucepan • The Saucepan requires a body made of steel and a lid made of glass and plastic • Each saucepan requires $10 of steel • Each Sauce pan requires $3 of glass • Each Saucepan requires $1 of plastic • Look at page 74 and you will see a Bill Of Materials

Completing a bill of Materials • Copy beneath the Job Cost Sheet the format of the Bill Of Materials • Requisition number is 5678 • Date is today • Job Number to be charged is 1234 • Department is Pressing • Enter the Data as required

Entering Data onto the Job Sheet • Take the total Direct Material cost and enter this into the Job Cost Sheet

Measuring Direct Materials • If you look on Page 74 you will see a Time Ticket (Time Sheet) • Copy this format onto a piece of paper • Time ticket number is 159 • Date is today • Employee is Tim Skyrme • Station is Lectern

Direct Labor Ctd • I take 3 hours to make the Steel into a pan • I take one hour to mould the plastic • I take a further half hour to attach the plastic to the glass • I am paid $3 an hour • Enter this information into the Time Ticket

Apply the Manufacturing Overheads • To allocate overheads we must choose an allocation basis • Remember what we did with floor space and machine hours yesterday with our tables and chairs • This time we are going to use a Predetermined Overhead Rate

Predetermined Overhead Rate • Our Company has predicted that total Fixed Costs (Indirect Costs) are going to be $100,000 for the year • It has also predicted that in total there are going to be 50,000 labor hours in the year • Therefore it has set its Predetermined Overhead Rate at …….. $2 per hour

Calculating the Indirect Costs • We know that our Predetermined Overhead rate is $2 per hour worked • Therefore we simply multiply this by the hours worked to produce the Cost Object • Enter this now on the Job Sheet

Problems with the application of Overheads • The information used to calculate the Predetermined Rate is an Estimation • Overheads are not easy to predict and as such they are either • Underapplied OR • Overapplied

An Example • Two Companies A Plc and B Plc • Both make the same product but A Plc calculates its Predetermined Overhead Rate according to Labor Hours, B Plc calculates according to Machine Hours

Actual Manufacturing Overheads = $50,000 Basis of Allocation = $5 per machine Hour Actual Machine Hours 10,500 Overapplication of $2500 Actual Manufacturing Overheads = $50,000 Basis of Allocation = 130% of Direct Materials Actual Direct Materials $30,000 Under Application of $11,000 A PLC B PLC

Reasons for Over or Under Application • Costs are often difficult to predict • The setting or prediction of costs is known as Budgeting • Budgeting is something we are going to come on to in to in later lectures

Standard Costs • When we attribute Direct and Indirect (Fixed and Variable Costs) we assume that these costs remain the same • Think Back to what we learnt about cost behavior • Often Fixed Costs are not flat, they are stepped, Often Variable Costs are not linear, there are economies of scale, or diseconomies of scale

Tutorial • We are going to do some Job Costings and then we are going to look at some variances and discuss how we can find out why and where these happened • Variance Analysis is an important job for the management accountant