Job Order Costing

Job Order Costing. Chapter 4. 2/14/05. Job Order Costing. How much does it cost to build a PT Cruiser? Accumulates direct and indirect costs to build a product by job or production order Assigns direct costs such as material and labor

Job Order Costing

E N D

Presentation Transcript

Job Order Costing Chapter 4 2/14/05

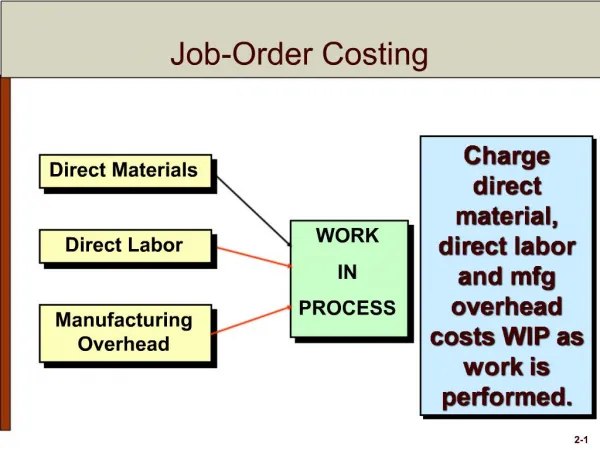

Job Order Costing • How much does it cost to build a PT Cruiser? • Accumulates direct and indirect costs to build a product by job or production order • Assigns direct costs such as material and labor • Allocates indirect costs (overhead) such as heat and lighting, depreciation and rent, maintenance, supervision, property tax, insurance, etc

Cost System Objectives • Provide managers with information for running the business • The cost system should be tailored to the underlying operations, and not vice versa • Costs to run the Cost System should not out weigh the benefits • Cost systems accumulate costs to facilitate decision making

Describe the building-block concepts of costing systems. Learning Objective 1

Building-Block Conceptsof Costing Systems Cost object (Job or product) Direct costs of a cost object (Material, Labor) Indirect costs of a cost object (material, labor, and other)

Building-Block Conceptsof Costing Systems Cost Assignment Direct Costs Cost Object Cost Tracing Indirect Costs Cost Allocation

Building-Block Conceptsof Costing Systems Cost pool (A grouping of individual cost items, i.e., overhead) Cost allocation base (A factor used to allocate costs to a cost objective, i.e., product, department)

Distinguish between job costing and process costing. Learning Objective 2

Job-Costing andProcess-Costing Systems Job-costing system Process-costing system (See exhibit 4-1) Distinct units of a product or service, i.e. Car, airplane Masses of identical or similar units of a product or service, i.e., potato chips

Outline a seven-step approach to job costing. Learning Objective 3

Seven-Step Approachto Job Costing Step 1: Identify the chosen cost object. Step 2: Identify the direct costs of the job. Step 3: Select the cost-allocation bases. Step 4: Identify the indirect costs.

Seven-Step Approachto Job Costing Step 5: Compute the rate per unit. Step 6: Compute the indirect costs. Step 7: Compute the total cost of the job.

General Approach to Job Costing A manufacturing company is planning to sell a batch of 25 special machines (Job 650) to a retailer for $114,800. Step 1: The cost object is Job 650. Step 2: Source? Direct costs are: Direct materials = $50,000 Direct manufacturing labor = $19,000

General Approach to Job Costing Step 3: The cost allocation base is machine-hours. Job 650 used 500 machine-hours. 2,480 machine-hours were used by all jobs. Step 4: Manufacturing overhead costs were $65,100. (depreciation, indirect material and labor, maintenance, insurance, utilities, taxes, etc.)

General Approach to Job Costing Step 5: Actual indirect cost rate is $65,100 ÷ 2,480 = $26.25 per machine-hour. Step 6: $26.25 per machine-hour × 500 hours = $13,125

General Approach to Job Costing Step 7: Direct materials $50,000 Direct labor 19,000 Factory overhead 13,125 Total $82,125

General Approach to Job Costing What is the gross margin of this job? Revenues $114,800 Cost of goods sold 82,125 Gross margin $ 32,675 What is thegross margin percentage? $32,675 ÷ $114,800 = 28.5%

Source Documents – see Exhibit 4-3 Job cost sheet (Records all costs associated with the job) Materials requisition record (records direct and indirect material) Labor time record (Records direct and indirect labor)

Distinguish actual costing from normal costing. Learning Objective 4

Costing Systems Actual costing is a system that uses actual costs to determine the cost of individual jobs. It allocates indirect costs based on the actual indirect-cost rate(s) times the actual quantity of the cost-allocation base(s). Problem: Since we don’t know actual costs until the end of the year, how do we allocate costs during the year?

Costing Systems Normal costing is a method that allocates indirect costs based on the budgeted indirect-cost rate(s) times the actual quantity of the cost allocation base(s). The budgeted rate is used during the year and adjusted to actual at year end.

Normal Costing Assume that the manufacturing company budgets $60,000 for total manufacturing overhead costs and 2,400 machine-hours. What is the budgeted indirect-cost rate? $60,000 ÷ 2,400 = $25 per hour How much indirect cost was allocated to Job 650? 500 machine-hours × $25 = $12,500

Normal Costing What is the cost of Job 650 under normal costing? Direct materials $50,000 Direct labor 19,000 Factory overhead 12,500 Total $81,500

Track the flow of costs in a job-costing system. Learning Objective 5

Transactions (See pages 108 – 114) Purchase of materials and other manufacturing inputs Conversion into work in process inventory Conversion into finished goods inventory Sale of finished goods

Transactions $80,000 worth of materials (direct and indirect) were purchased on credit. Materials Control Accounts Payable Control 1. 80,000 1. 80,000

Transactions Materials costing $75,000 were sent to the manufacturing plant floor. $50,000 were issued to Job No. 650 and $10,000 to Job 651. $15,000 of indirect materials were issued. What is the journal entry?

Transactions Work in Process Control: Job No. 650 50,000 Job No. 651 10,000 Factory Overhead Control 15,000 Materials Control 75,000

Transactions Materials Control 1. 80,000 2. 75,000 Work in Process Control 2. 60,000 Manufacturing Overhead Control 2. 15,000 Job 650 2. 50,000

Transactions Total manufacturing payroll for the period was $27,000. Job No. 650 incurred direct labor costs of $19,000 and Job No. 651 incurred direct labor costs of $3,000. $5,000 of indirect labor was also incurred. What is the journal entry?

Transactions Work in Process Control: Job No. 650 19,000 Job No. 651 3,000 Manufacturing Overhead Control 5,000 Wages Payable 27,000

Transactions Wages Payable Control 3. 27,000 Work in Process Control 2. 60,000 3. 22,000 Manufacturing Overhead Control 2. 15,000 3. 5,000 Job 650 2. 50,000 3. 19,000

Transactions Assume that depreciation for the period is $26,000. Other manufacturing overhead incurred amounted to $19,100. What is the journal entry?

Transactions Manufacturing Overhead Control 45,100 Accumulated Depreciation Control 26,000 Various Accounts 19,100 What is the balance of the Manufacturing Overhead Control account?

Transactions $62,000 of overhead was allocated to the various jobs of which $12,500 went to Job 650. Work in Process Control 62,000 Manufacturing Overhead Control 62,000

Transactions The cost of Job 650 is: Job 650 2. 50,000 3. 19,000 6. 12,500 Bal. 81,500

Transactions Job 650 was sold for $114,800. What is the journal entry? Accounts Receivable Control 114,800 Revenues 114,800 Cost of Goods Sold 81,500 Finished Goods Control 81,500

Transactions What is the balance in the Finished Goods Control account? $104,000 – $81,500 = $22,500

Transactions Direct Materials Used $60,000 + Direct Labor and Overhead $84,000 – Cost of Goods Manufactured $104,000 = Ending WIP Inventory $40,000

Transactions Cost of Goods Manufactured $104,000 – Ending Finished Goods Inventory $22,500 = Cost of Goods Sold $81,500

Account for end-of-period underallocated or overallocated indirect costs using alternative methods. Learning Objective 6

End-Of-Period Adjustments Manufacturing Overhead Actual Manufacturing Overhead Applied Bal. 65,100 Bal. 62,000 Underallocated indirect costs (Actual costs greater than Applied) Overallocated indirect costs (Applied costs greater than actual)

End-Of-Period Adjustments How was the allocated overhead determined? Allocated overhead was calculated as follows: 2,480 machine-hours × $25 budgeted rate = $62,000 If actual overhead incurred was $65,100, then $65,100 – $62,000 = $3,100 (underallocated)

End-Of-Period Adjustments Actual manufacturing overhead costs of $65,100 are more than the budgeted amount of $62,000. Actual machine-hours of 2,480 are more than the budgeted amount of 2,400 hours.

End-Of-Period Adjustments Approaches to disposing underallocated or overallocated overhead: 1. Adjusted allocation rate approach 2. Proration approaches 3. Immediate write-off to Cost of Goods Sold approach (use only if adjustment amount is immaterial)

Adjusted AllocationRate Approach Actual manufacturing overhead ($65,100) exceeds manufacturing overhead allocated ($62,000) by 5%. 3,100 ÷ 62,000 = 5% Actual manufacturing overhead rate is $26.25 per machine-hour ($65,100 ÷ 2,480) rather than the budgeted $25.00.

Adjusted AllocationRate Approach The manufacturing company could increase the manufacturing overhead allocated to each job by 5%. Manufacturing overhead allocated to Job 650 under normal costing is $12,500. $12,500 × 5% = $625 $12,500 + $625 = $13,125, which equals actual manufacturing overhead.

Adjusted Allocation Rate • Problem: This method would reallocate costs back to each job during the year on an actual basis. • You have already issued financial statements quarterly based on the allocation method. • You would have to restate all your prior costs! You can’t do that.

Proration Approach Basis to prorate under- or overallocated overhead: – total amount of manufacturing overhead allocated (before proration) • Determine the amount of manufacturing overhead • included in WIP, FG and COGS • Divide by total cost in each account to get the % • Multiply the % times the over/under allocated $ • Adjust WIP, FG and COGS for the above amounts

Proration Approach “A” Assume the following manufacturing overhead component of year-end balances (before proration) (Steps 1 & 2) Work in Process $23,500 38% Finished Goods 26,000 42% Cost of Goods Sold 12,500 20% Total $62,000 100%