Job Order Costing

17. Job Order Costing. Describe cost accounting systems used by manufacturing businesses. 1. Describe the use of job order cost information for decision making. Describe and illustrate a job order accounting system.

Job Order Costing

E N D

Presentation Transcript

17 Job Order Costing

Describe cost accounting systems used by manufacturing businesses. 1 Describe the use of job order cost information for decision making. Describe and illustrate a job order accounting system. Describe the flow of costs for a service business that uses a job order cost accounting system. 4 2 3 Learning Objective 1 Learning Objective 1 Job Order Costing 3-1 3-1 After studying this chapter, you should be able to: Insert Chapter Objectives Describe the nature of the adjusting process. Describe the nature of the adjusting process. 17-2

1 Describe cost accounting systems used by manufacturing businesses. 17-3

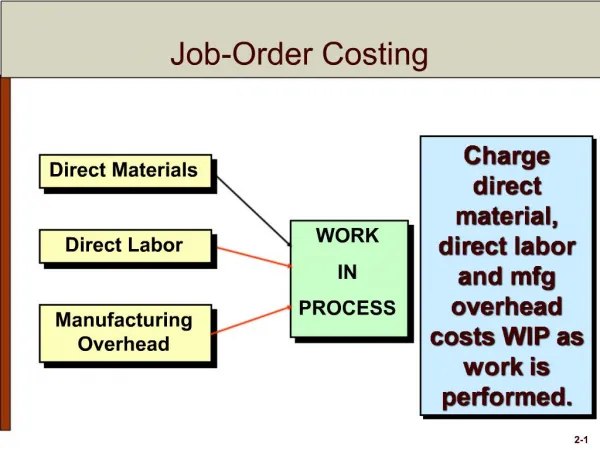

1 Cost Accounting System Overview A job order cost system provides product costs for each quantity of product that is manufactured. Each quantity of product that is manufactured is termed a job. Manufacturers that use a job order cost system are sometimes called job shops.

Exhibit 1 1 Summary of Legend Guitars’ Manufacturing Operations (continued)

Exhibit 1 1 Summary of Legend Guitars’ Manufacturing Operations (continued)

1 Cost Accounting System Overview A process cost system provides product costs for each manufacturing department or process. Process cost systems are often used by companies that manufacture units of a product that are indistinguishable from each other and are manufactured using a continuous production process.

2 Describe and illustrate a job order cost accounting system. 17-8

2 Exhibit 2 Flow of Manufacturing Costs

2 In a job order cost accounting system, perpetual inventory controlling accounts and subsidiary ledgers are maintained for materials, work in process, and finished goods inventories as shown below:

2 Materials Receiving Report No. 196 Invoice The receiving report and the invoice are used to record the receipt of the merchandise and to control the payment for purchased items.

2 Exhibit 3 Materials Information and Cost Flows a. To Materials Requisitions

2 Materials Information and Cost Flows (continued) Exhibit 3 From Materials Ledger Account Materials Requisitions b. b. Job Cost Sheets b. b.

2 Receiving Report No. 196 Invoice 750 units of No. 8 Maple Wood The journal entry to record the supplier’s invoice related to Receiving Report 196 is as follows:

2 The storeroom releases materials for use in manufacturing when a materials requisition is received. Job cost sheets make up the work in process subsidiary ledger.

2 A summary of the materials requisitions is used as a basis for the journal entry recording the materials used for the month. For the requisition of direct materials, the following entry is made:

2 Example Exercise 17-1 Issuance of Materials On March 5, Hatch Company purchased 400 units of raw materials at $14 per unit. On March 10, raw materials were requisitioned for production as follows: 200 units for Job 101 at $12 per unit, and 300 units for Job 102 at $14 per unit. Journalize the entry on March 5 to record the purchase and on March 10 to record the requisition from the materials storeroom. 17-17

Mar. 5 Materials……………………………… 5,600 Accounts Payable………………. 5,600 $5,600 = 400 × $14 10 Work in Process…………………….. 6,600* Materials………………………….. 6,600 * Job 101 $2,400 = 200 × $12 Job 102 4,200 = 300 × $14 Total $6,600 Follow My Example 17-1 For Practice: PE 17-1A, PE 17-1B 2 Example Exercise 17-1 (continued) 17-18

2 Factory Labor When employees report for work, they may use clock cards or in-and-out cards. When employees work on an individual job, they use time tickets.

2 Exhibit 4 Labor Information and Cost Flows

2 A Closer Look at Job 72 On December 26, 2010, S. Andrews spent eight hours on Job 72 at an hourly rate of $15 for a cost of $120 (8 hrs. × $15). A total of 500 hours was spent by all employees who worked on Job 72 during December, for a total cost of $7,500.

to Job Cost Sheet 2 Exhibit 4 Labor Information and Cost Flows (a closer look) December Job 72 (500 hours) for a total cost of $7,500 (continued)

2 Exhibit 4 Labor Information and Cost Flows (continued) from Time Sheets The same procedure is followed for Job 71.

2 A total of 500 hours was spent by employees on Job 72 during December for a total cost of $7,500. A summary of the time tickets is used as the basis for the following journal entry:

Work in Process………………………………………… 20,000* Wages Payable…………………………………….. 20,000 *$12,800 (800 hrs. × $16) + $7,200 (600 hrs. × $12) Follow My Example 17-2 For Practice: PE 17-2A, PE 17-2B 2 Example Exercise 17-2 Example Exercise 18-2 Direct Labor Costs During March, Hatch Company accumulated 800 hours of direct labor costs on Job 101, and 600 hours on Job 102. The total direct labor was incurred at a rate of $16 per direct labor hour for Job 101 and $12 per direct labor hour for Job 102. Journalize the entry to record the flow of labor costs into production during March. 17-25

2 Factory Overhead Cost Factory overhead includes all manufacturing costs except direct materials and direct labor. Factory overhead costs are derived from a variety of sources including the following: • Indirect materials • Indirect labor • Factory power • Factory depreciation

2 The factory overhead of $4,600 incurred in December for Legend Guitars would be recorded as follows:

Follow My Example 17-3 Factory Overhead…………………………………………. 8,300 Materials………………………………………………... 800 Wages Payable………………………………………… 3,400 Utilities Payable……………………………………….. 1,600 Accumulated Depreciation………………………….. 2,500 For Practice: PE 17-3A, PE 17-3B 2 Example Exercise 17-3 Example Exercise 18-2 Factory Overhead Costs During March, Hatch Company incurred factory overhead as follows: indirect materials $800, indirect labor $3,400, utilities cost $1,600, and depreciation $2,500. Journalize the entry to record the factory overhead incurred during March. 17-28

2 Allocating Factory Overhead Factory overhead costs are allocated to the jobs using a common measure related to each job. The measure used to allocate factory overhead is frequently called an activity base, allocation base, or activity driver.

2 Predetermined Factory Overhead Rate To provide current job costs, factory overhead may be allocated or applied to production using a predetermined factory overhead rate. Estimated Total Factory Overhead Costs Predetermined Factory Overhead Rate = Estimated Activity Base

2 Management estimates factory overhead costs to be $50,000 and the activity base to be 10,000 direct labor hours. The predetermined overhead rate is calculated in Slide 32.

Predetermined Factory Overhead Rate $50,000 = 10,000 direct labor hours Predetermined Factory Overhead Rate = $5 per direct labor hour 2 Predetermined Factory Overhead Rate Estimated Total Factory Overhead Costs = Estimated Activity Base

2 Exhibit 5 Applying Factory Overhead to Jobs

2 Exhibit 5 A Closer Look at Job 72 Job 72 required 500 direct labor hours. Because the number of direct labor hours is the cost driver, we use 500 as the basis for determining overhead. (continued)

2 Exhibit 5 A Closer Look at Job 72 (continued) 500 hours × $5

2 Slides 34 and 35 focused on Job 72. The textbook shows two jobs that were worked on in December. When overhead is applied to both jobs, the entry is for $4,250 ($1,750 + $2,500).

2 • If the applied overhead is less than the actual overhead incurred, the factory overhead account will have a debit balance and is underapplied factory overhead or underabsorbed factory overhead. • If the applied overhead is more than the actual overhead incurred, the factory overhead account will have a credit balance and is overapplied factory overhead or overabsorbed factory overhead.

2 Overapplied and Underapplied Factory Overhead Underapplied balance Overapplied balance

2 Example Exercise 17-4 Applying Factory Overhead Hatch Company estimates that total factory overhead costs will be $100,000 for the year. Direct labor hours are estimated to be 25,000. Determine (a) the predetermined factory overhead rate, (b) the amount of factory overhead applied to Jobs 101 and 102 in March using the data on direct labor hours from Example Exercise 17-2 (Slide 25), and (c) prepare the journal entry to apply factory overhead to both jobs in March according to the predetermined overhead rate. Click this button to go to Slide 25. Enter “39” and press “Enter” to return to this slide. 17-39

Job 101 $3,200 = 800 hours × $4.00 per hour • Job 102 2,400 = 600 hours × $4.00 per hour • Total $5,600 Follow My Example 17-4 For Practice: PE 17-4A, PE 17-4B 2 Example Exercise 17-4 (continued) (a) $4.00 = $100,000 ÷ 25,000 direct labor hours • Work in Process……………………………….. 5,600 • Factory Overhead…………………………. 5,600 17-40

2 Disposal of Factory Overhead Balance An ending debit balance (underapplied overhead) in the factory overhead account is disposed of by the following entry:

2 Disposal of Factory Overhead Balance An ending credit balance (overapplied overhead) in the factory overhead account is disposed of by the following entry:

2 Disposal of Factory Overhead Balance The journal entry to eliminate Legend Guitars’ underapplied overhead balance of $150 at the end of the calendar year would be:

2 Work in Process During the period, Work in Process is increased (debited) for the following: • Direct material cost • Direct labor cost • Applied factory overhead cost

2 Job Cost Sheets and the Work in Process Controlling Account Exhibit 6

2 At the end of the accounting period (December 31) the total costs for Job 71 are determined and the following entry is made:

2 Example Exercise 17-5 Job Costs At the end of March, Hatch Company had completed Jobs 101 and 102. Job 101 is for 500 units, and Job 102 is for 1,000 units. Using the data from Example Exercise 17-1, 17-2, and 17-4, determine (a) the balance on the job cost sheets for Jobs 101 and 102 at the end of March, and (b) the cost per unit for Jobs 101 and 102 at the end of March. EE 17-1 (Slide 17) To return to this slide, type “47” and press “Enter.” EE 17-2(Slide 25) EE 17-4(Slide 39) 17-47

Follow My Example 17-5 For Practice: PE 17-5A, PE 17-5B 2 Example Exercise 17-5 (continued) a. Job 101 Job 102 Direct materials $ 2,400 $ 4,200 Direct labor 12,800 7,200 Factory overhead 3,200 2,400 Total costs $18,400 $13,800 • Job 101 $36.80 = $18,400 ÷ 500 units • Job 102 $13.80 = $13,800 ÷ 1,000 units 17-48

2 Finished Goods and Cost of Goods Sold The Finished Goods account is a controlling account for the subsidiary finished goods ledger or stock ledger. Each account in the finished goods ledger contains cost data for the units manufactured, units sold, and the units on hand.

2 Exhibit 7 Finished Goods Ledger Account