Download

1 / 11

110 likes | 325 Vues

An Examination of Synthetic Short Selling Through Credit Default Swaps . Edward Pekarek, Esq. and Christopher Lufrano. Reading Questions. Define Collateralized Debt Obligations and Credit Default Swaps.

E N D

An Examination of Synthetic Short Selling Through Credit Default Swaps Edward Pekarek, Esq. and Christopher Lufrano

Reading Questions • Define Collateralized Debt Obligations and Credit Default Swaps. • How can an investor use a synthetic Credit Default Swap to “short” a Collateralized Debt Obligation? • What is a “naked” Credit Default Swap? • What specific steps did the U.S. government through the Federal Reserve and the U.S. Treasury undertake during the financial crisis to stabilize the derivative markets? • How can speculators use Credit Default Swaps to speculate on Sovereign Debt? • How did John Paulson implement a short sale strategy against the U.S. mortgage market? • What material misrepresentations did the S.E.C allege Goldman Sachs and its employee, Facrice Tourre, make to investors with regards to the ABACUS deal? • How was SEC v. Goldman Sachs, et al. resolved?

Collateralized Debt Obligations • Defined as a structured product that raises capital through the issuance of debt or equity securities and invests the funds in pooled credit assets • The assets are typically Asset-Backed Securities • Two Types: • Cash CDO • Synthetic CDO • The CDO is comprised of multiple layers called tranches that are distinguished by risk • The riskiest layer is the “equity” tranche

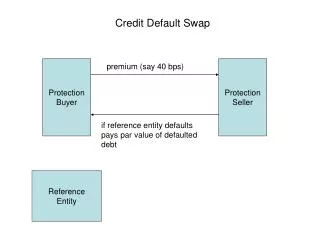

Credit Default Swaps • Defined as a bilateral contract, whereby the holder obtains a future right to be compensated upon the happening of a credit event • A credit event is a contractual condition typically negotiated between counterparties • CDS can be used to “synthetically” short or hedge, through the purchase of credit protection, a CDO in whole or part • i.e. an underlying tranche or Soveriegn Debt

The Paulson “Put” • John Paulson’s hedge fund wished to short the US housing market because it forecasted the market was overvalued in 2005-2006 • Paulson created strategic naked CDS exposure by purchasing credit protection against ABACUS and other similar Residential Mortgage Backed Securities (RMBS) • The strategy is akin to an option put because the buyer of the CDS does not own the underlying collateral just like the put purchaser does not own the underlying stock

U.S. Regulation of Derivatives • Key Sources of U.S. Securities Law: • Securities Act of 1933 • Securities Exchange Act of 1934 • The Securities Exchange Commission (SEC) • The Department of Justice (DOJ) • CDO and CDS are expressly excluded from the term “security” as defined in the Securities Act • Exchange Act Rule 3b-3 defines short sale as: • “Any sale of a security which the seller does not own or any sale which is consummated by the delivery of a security borrowed by, or for the account of, the seller.” 17 C.F.R. §240.3b-3.

Anti-Fraud Provisions • U.S. law fails to adequately attend to CDO and CDS, thus the SEC and DOJ invoked the broad anti-fraud provisions: • §17(a) and § 10(b) of the Securities Act, and • Rule 10b-5 of the Exchange Act • Rule 10b-5 states: • It shall be unlawful for any person, directly or indirectly, by the sue of any means or instrumentality of interstate commerce… • To employ any device, scheme, or artifice to defraud • To make any untrue statement of a material fact or to omit to state a material fact necessary in order to make the statements made, in the light of the circumstances under which they were made, not misleading, or • To engage in any act, practice, or course of business which operates or would operate as a fraud or deceit upon any person, • In connection with the purchase or sale of any security

SEC v. Goldman Sachs & Co, et al. – The Complaint • The SEC initiated a civil securities fraud action against Goldman Sachs & Co and Fabrice Tourre and alleged: • The defendants misled ACA Management LLC (ACA) by misrepresenting that Paulson was a “transaction sponsor” • The defendants failed to disabuse ACA of its misapprehension that Paulson would take a long position in the ABACUS equity tranche • The defendants misled CDO and CDS investors through ABACUS’ public marketing materials • Key element: MATERIALITY

The Goldman Settlement • Goldman agreed to settle the SEC charges for $550M (largest in SEC history) • Goldman consented to the entry of a final judgment without admitting or denying the fraud allegations in the Complaint • The Settlement allowed Goldman to arguably minimize damage to its reputation and prospective liability

Financial Reform • Dodd-Frank Wall Street Reform &Consumer Protection Act (2010) • Key reforms of CDO and CDS market: • Induce or require “standardized” derivatives to be cleared on exchanges and/or clearinghouse • Establish conditions to induce derivatives to be cleared like commodities and futures trades • Ensure adequate reserves are held against all OTC trades not centrally cleared • Require margin or collateral to support derivative positions • More transparent transaction prices and volumes

Conclusions • CDO and CDS speculation is widely believed to have caused the financial crisis from 2007-2009 • Goldman Sachs and other Wall Street firms were intimately involved in these markets • Appropriate reform measures in the credit, derivatives, and equities markets were clearly overdue • Only, time will tell whether these measures were effective in preventing subsequent market turmoil