Credit Default Swaps

Credit Default Swaps. Shane Kaiser. Credit Default Swaps. A credit default swap (“CDS”) is an over-the-counter credit derivative contract between two counterparties that was originally implemented to transfer credit-risk

Credit Default Swaps

E N D

Presentation Transcript

Credit Default Swaps Shane Kaiser

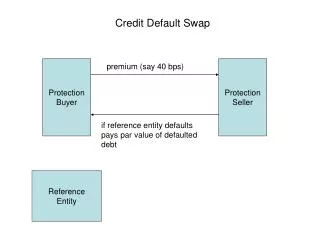

Credit Default Swaps • A credit default swap (“CDS”) is an over-the-counter credit derivative contract between two counterparties that was originally implemented to transfer credit-risk • The risk of default is transferred from the holder of the debt security to the seller of the swap. • Originally used by big banks as insurance against loans exposure, but has since grown to be used for things like making a profit on speculation

Credit Default Swaps • Two parties: protection buyer and protection seller • The “protection buyer” purchases a CDS from the “protection seller” by making periodic payments (typically either semiannually or quarterly), called a CDS premium, to the “protection seller”, and in return receives a payoff if an underlying financial instrument defaults or experiences a similar credit event. • Protection buyers typically buy $10 million in protection with a maturity period of 5 years.

History Source: International Swaps and Derivatives Association (“ISDA”)

Single Name Default Swap • The simplest and most common type of CDS • Only one reference entitythat can be any borrower, but is usually one of a few hundred widely traded companies • Commonly used by big banks to free up capital • Currently used by many hedge funds, because not much capital is required to purchase a swap

Portfolio Default Swaps • Nearly the same as Single Name Default Swaps, but reference around 50 to 100 (or more) underlying entities • Mostly all Portfolio Default Swaps have been replaced by index default swaps

Index Default Swaps • Unlike a regular credit default swap, an index default swap (or CDX) is a completely standardized credit security, there for Index Default Swaps can be more liquid and trade at a smaller bid-ask spread • Makes it cheaper to hedge a portfolio with a CDX than it would be to buy many single CDS

Pricing • Every underlying is give a certain amount of “basis points” (each representing .01%) • These basis points are dependent upon the stability/riskiness of the underlying credit • The riskier the underlying, the higher the basis points will be. • Reflect markets perception of the risk of default over the risk free rate, almost like a percentage chance of how likely the underlying will default before maturity

Pricing - Example • A CDS spread for Corporation A is 40 basis points • Thus a protection buyer buying $10 million in protection must pay the protection seller $40,000 annually ($10 million * 0.4%) till maturity or a credit default of the underlying occurs. • Payments are typically made semiannually with a maturity of 5 years, thus in this case the buyer will be paying the seller $20,000 each quarter for the next 5 years (assuming no credit event occurs) • The buyer would have lost $200,000 in this event

Payout • In the event of a credit event (eg, bankruptcy): • The protection buyer no longer needs to pay the seller (in this example it was $20,000 every six months) • The two parties wait 30 days after the credit event, and seewhere the senior debt of the underlying is trading on that 30th day • After those 30 days, the protection seller pays back the protection buyer the amount of protection purchased times, one minus the current price of the debt is trading

Payout -Example • If the protection buyer purchased $10 million in protection, and the underlying defaults, the payout seller waits 30 days after the default occurs to determine how much to pay the protected buyer. • If the senior debt is trading at $0.30 cents on the dollar on that 30th day then the pay out will be: • $10 million * (1 - $0.30) = $7 million dollar payout

Profitability • If the underlying goes into default, the protection buyer stops paying the seller that quarterly amount immediately, and receives payment in 30 days. • This can create extremely profitable situations • For example: • A protection buyer purchases $10 million in protection on an entity with 300 basis points (fairly risky company) and a maturity of 5 years • The underlying defaults in 12 months and the senior debt drops to $0.50 cents on the dollar • ($ 10 million * (1 - $0.50)) – ($10 million * 3%) = $4.7 million

Criticism/Controversy • “Like Robert Oppenheimer and his team of nuclear physicists in the 1940s, Brickell and his JPMorgan colleagues didn't realize they were creating a monster.” -Matthew Philips, MSNBC-Newsweek

Criticism/Controversy • Famous Cases in 2008: • AIG - defaulted on $14 billion worth of credit default swaps made with various investment banks, insurance companies and other entities, and needed the American government to bail them out • Bankruptcy of Lehman Brothers - due to subprime mortgage crisis Lehman Brothers declared bankruptcy, and caused nearly $400 billion to become payable to the buyers of CDS in Lehman Brothers

Criticism/Controversy • Original intent: • to spread risk and act as insurance on loan exposure • Unintended side affects: • Created more risk, with very little leverage and no regulation • Created more negative speculation • Became more of a money making scheme than a device to protect and hedge

Sources • http://www.newsweek.com/2008/09/26/the-monster-that-ate-wall-street.html • http://en.wikipedia.org/wiki/Credit_default_swap • http://www.investopedia.com/terms/c/creditdefaultswap.asp • http://www.isda.org/ • http://money.cnn.com/2009/03/16/markets/cds.bear.fortune/index.htm • http://www.ft.com/cms/s/0/25137702-972d-11dd-8cc4-000077b07658.html#axzz14sX36S7Q