Slides for Part IV-A

Slides for Part IV-A. Introduction to Forecasting. Outline: What is forecasting? Why use forecasting techniques? Applications of forecasting methods Types of forecasting models Time series vs. cross-sectional data. . Introduction to Forecasting. Initial points:

Slides for Part IV-A

E N D

Presentation Transcript

Slides for Part IV-A Introduction to Forecasting • Outline: • What is forecasting? • Why use forecasting techniques? • Applications of forecasting methods • Types of forecasting models • Time series vs. cross-sectional data.

Introduction to Forecasting • Initial points: • The economics profession is held in low regard in some quarters, partly because there is the widespread perception (if not reality) that economists fail in their most meaningful or potentially useful task, which is to produce accurate forecasts of GDP, inflation, housing starts, stock market movements, interest rates, employment, car sales, imports, . . . . • Econometric forecasting has been, to some extent, “oversold.”

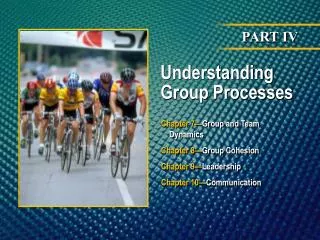

Which way is the stock market headed, Professor? If I could see the future, I would be on the plane to Las Vegas

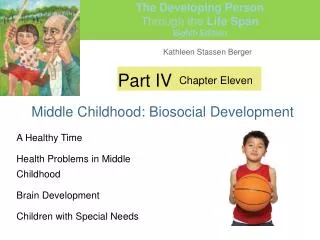

ActualPredicted S & P 500, Index of Total Return

Why use forecasting? • Virtually every significant business decision (e.g., decisions to place orders for raw materials, semi-finished articles, or finished goods, borrowing decisions, hiring decisions, decisions to close plants, decisions to open new stores or production facilities, decisions to purchase capital goods, or decisions about near-term production flows) are necessarily based on views of decision-makers about the future course of variables which affect their business. Thus, decision-makers are compelled to form expectations--indeed, to make a forecast-- about future business conditions. • Econometric forecasting, for all its shortcomings, beats the alternatives.

A review of forecasting applications • Operations planning and control. Firms use forecasting for inventory and production management, and sales force management,. • Strategic decision making. Forecasting is helpful to decision-making with respect to the development of new products, entry into new geographic markets, and so on. • Cost estimation: In making bids for construction projects or the delivery of capital goods such as turbine generators, aircraft, or ships, firms must forecast the prices of raw materials , semi-finished articles, and so forth.

Marketing. Decision-makers rely heavily on forecasts about the responsiveness of consumers or buyers to various marketing schemes such as couponing, rebates, tie-ins, low APR financing, volume discounts, and so on. • Fiscal and Monetary Policy. Federal Reserve officials, Congress, and the President rely on forecasts of output, employment, inflation, and other macroeconomic variables to develop monetary policy initiatives, tax policy, and government spending policy. • Financial Market Speculation: Money managers (professional and otherwise) rely on forecasts of firms’ earnings and movements of composite indices (such as the DOW, NASDAQ, or Russell 2000) in formulating their portfolio strategies.

Investment, capacity planning. Decisions to add or subtract capacity depend on long-term forecasts of market conditions. What are the trends in market size and market share? • Business and Government Budgeting. Government appropriations are conditioned upon estimates of revenues from income taxes, excise taxes, etc. The Department of Treasury uses forecasting techniques to assess if a particular tax initiative is “revenue neutral,” “revenue enhancing,” or “revenue decreasing.” • Demography: Demographers use forecasting techniques to forecast population growth around the world, changes in the age composition of the population, and changes in other demographic characteristics of the population.

Uses and misuses of forecasting • S&K note that many professional forecasters are “momentum” followers--i.e., they will tend to extrapolate recent conditions into the near future--and hence miss significant changes in conditions--this habit produces substantial forecast errors. • Professional forecasters would rather “fail conventionally” than “succeed unconventionally.” This factor produces a tendency toward a convergence of forecasts among professional forecasters.

S&K note that comparatively small forecast errors (that is , from point estimates) can have significant negative consequences for decision-makers. • Example:Suppose that the growthof demand for electricity for a powercompany was forecast to be 6 percent per year but turned out to be 4 percent per year. Building capacity to meet the forecast would generate excesscapacity and the error would be compounded over time.

Types of forecasting models • Sherman & Kolk (S&K) distinguish between two types of models: • Qualitative modelsThese models are constructed using surveys of “experts” in specific areas such as residential construction , petroleum/natural gas, aluminum, banking, or the auto industry. • Quantitative models:There are two types ofquantitative models—time series models, which are based exclusively ontime series data;andcausal models.Causal models are based on the analysis of time series data or cross-sectional data.

Time -series data: historical data--i.e., the data sample consists of a series of daily, monthly, quarterly, or annual data for variables such as prices, income , employment , output , car sales, stock market indices, exchange rates, and so on. Cross-sectional data: All observations in the sample are taken from the same point in time and represent different individual entities (such as households, houses, etc.)

With time series models,we seek to uncover trendsin past data and then project them into the future Time series models include: • “Naïve” extrapolation • Simple moving average models • Complex moving average models (such as ARMA and ARIMA) • The multiplicative time series model • Exponential smoothing

Y =f(X) Causal models This class of models entails the estimation of causal relationships (as suggested by theory, usually) between a dependent variable and one or more independentor explanatory variables.The principaltool of causal forecasting is regressionanalysis.

To forecast the demand for coal, we insert forecastedvalues of FIS, FEU, etc. into this equation Example: The Demand for Coal COAL = 12,262 + 92.43FIS + 118.57FEU -48.90PCOAL + 118.91PGAS • COAL is monthly demand for bituminous coal (in tons) • FIS is the Federal Reserve Board Index of Iron and Steel production. • FEU the FED Index of Utility Production. • PCOAL is a wholesale price index for coal. • PGAS is a wholesale price index for natural gas. Source: Pyndyck and Rubinfeld (1998), p. 218.