Chapter 5 Double-Entry System

Chapter 5 Double-Entry System. Main Points: 1.Introduction about Double-Entry System. 2. T account 3.Transaction Analysis and Record Time Allocated: 4 Periods. Learning Objectives. The students are required to -- understand and define double-entry system. have an idea about T account.

Chapter 5 Double-Entry System

E N D

Presentation Transcript

Chapter 5Double-Entry System Main Points: 1.Introduction about Double-Entry System. 2. T account 3.Transaction Analysis and Record Time Allocated: 4 Periods

LearningObjectives The students are required to -- • understand and define double-entry system. • have an idea about T account. • know how to do the transaction analysis and record.

Revision • 1. What is account? • 2. What are the commonly used accounts? • 3. What is current assets? • 4. What is long-term assets? • 5. What are the two types of liability accounts? • 6. What is owner’s equity accounts?

Revision • 7. Translate the following phrases into English: • 预付保险费 应收帐款 应收票据 • 应付帐款 办公设备 办公用品 • 累计折旧 折旧费用 预收影印费 • 煤气水电费 应付抵押 办公工资费用

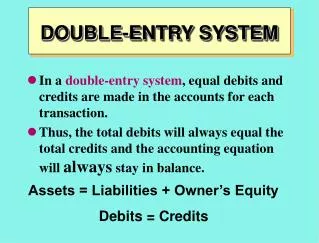

What? Warm-up 1.What is considered as the heart of modern accounting? --- The double-entry system is considered as the heart of modern accounting. 2. What is double-entry system? ---The double-entry is part of the language of business. It provides checks and balances to ensure that your books are always in balance.

Presentation In chapter four we have learnt accounts and we have an idea about the commonly used accounts which are assets accounts, liability accounts and owner’s equity accounts. And we know that accounting is actually a language. Because the purpose of any language is to convey information and so as accounting, it conveys transaction information and record them. And for accounting, the double-entry system is considered as the heart of it during medieval Europe. Why is it said as the heart of the modern accounting? Today we are going to have more idea about it in Chapter 5.

In-class Activities (1) Reading and Questions (P 32): 1. What is considered as the heart of modern accounting? ---The double-entry system is considered as the heart of modern accounting. 2.What are the two types of the double-entry system? ---One is a manual system the other is a computerized accounting system. What?

In-class Activities (1) 3. What do the accountants do for these two different types of double-entry system? --- For a manual system, transactions are recorded in the books and for a computerized accounting system, the transaction are entered into the computer. 4. What does the double-system provide? --- It provides checks and balances to ensure that your books are always in balance.

In-class Activities (1) 5. What does the double-entry system have? ---It has two journal entries: a debit and a credit and debits must always equal credits. 6. Why does double-entry accounting prevent some common bookkeeping errors? --- Because debits equal credits.

In-class Activities (1) 7. How many accounts at least does a transaction affect with double-entry accounting? Why? ---With double-entry accounting, every transaction affects at least two accounts, since there is at least one debit and one credit for each transaction. 8. What is the basic form of the double-entry system?

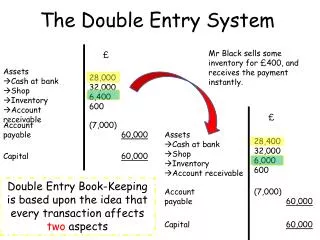

In-class Activities (1) --- The T account is the basic form of the double-entry system. 9. How many parts does the T account have? ---Basically it has three parts: a title, the debit and the credit, such as: Title of Account left or Right or Debit Side Credit Side

In-class Activities (1) 10. What are the rules for the increases and decreases of different? --- Suppose that the increase of assets is recorded by debit, and the decrease of assets is credited. Increase of liabilities and owner’s equity will be recorded by credit and the decrease of liabilities an owner’s equity will be debited. These rules are as follows:

In-class Activities (2) Transaction Analysis and Record(P33): The following transaction happened in George Ross Photocopy Company during March. Let us use these transactions to illustrate the double-entry system rules. 1. March 3: Mr. George started his photocopy company on March1 with$20,000 that was immediately deposited into the bank.

In-class Activities (2) Analysis: Assets increased. Owner’s equity increased. Increases in assets are recorded by debits. Increases in owner’s equity are recorded by credits. Increase in assets is recorded by a debit to Cash. Increase in owner’s equity is recorded by a credit to George Ross, Capital. Dr. Cash $20,000 Cr. George Ross, Capital $20,000

In-class Activities (2) 2. March 7: Purchased photocopy equipment for $2,000 with cash. Analysis: Assets increased. Assets decreased. Increases in assets is recorded by a debit to Photocopy Equipment. Decrease in assets is recorded by a credit to Cash. Dr. PhotocopyEquipment $2,000 Cr. Cash $2,000

In-class Activities (2) 3. March 7: Purchased office equipment from Hougas Equipment Co. for $5,300, paying $2,300 in cash and agreeing to pay the rest next month. Analysis: Assets increased. Assets decreased. Liabilities increased. Increases in assets are recorded by debits. Decreases in assets are recorded by credits. Increases in liabilities are recorded by credits. Increase in assets is recorded by a debit to Office Equipment.

In-class Activities (2) Decrease in assets is recorded by a credit to Cash. Increase in liabilities is recorded by a credit to Accounts Payable. Dr. Office Equipment $5,300 Cr. Cash $2,300 Accounts Payable 3,000

In-class Activities (2) 4. March8: Purchased on credit photocopy supplies for $2,300 and office supplies for $800 from Tim Supply Co. Analysis: Assets increased. Liabilities increased. Increases in assets are recorded by debits. Increases in Liabilities are recorded by credits. Increase in assets is recorded by debits to Photocopy Supplies and Office Supplies. Increase in liabilities in recorded by a credit to Accounts Payable.

In-class Activities (2) Dr. Photocopy Supplies $2,300 Office Supplies 800 Cr. Accounts Payable $3,100 5. March 8: Paid $600 in cash for a one-year insurance policy with coverage effective from March 1. Analysis: Assets increased. Assets decreased. Increases in assets are recorded by debits. Decreases in assets are recorded by credits. Increase in assets is recorded by a debit to Prepaid Insurance. Decrease in assets is recorded by a credit to Cash.

In-class Activities (2) Dr. Prepaid Insurance $600 Cr. Cash $600 6. March 9: Paid Tim Supply Co. $3,100 of the amount owed by check. Analysis: Assets decreased. Liabilities decreased. Decreases in assets are recorded by credits. Decreases in liabilities are recorded by debits. Decrease in liabilities is recorded by a debit to Account Payable. Decrease in assets is recorded by a credit to Cash.

In-class Activities (2) Dr. Accounts Payable $3,100 Cr. Cash $3,100 7. March 10: Performed a service by printing brochures for a garment dealer and agreed to collect the fee at the beginning of the next month, $6,000. Analysis: Assets increased. Owner’s equity increased. Increases in assets are recorded by debits. Increases in owner’s equity are recorded by credits. Increase in assets is recorded by a debit to Accounts Receivable. Increase in owner’s equity is recorded by credit to Photocopy Fess Earned.

In-class Activities (2) Dr. Accounts Receivable $6,000 Cr. Photocopy Fees Earned $6,000 8. March 14: Accept $1,300 as an advance fee for copying works to be done for an advertising agency. Analysis: Assets increased. Liabilities increased. Increases in assets are recorded by debits. Increases in liabilities are recorded by credits. Increase in assets is recorded by a debit to Cash. Increase in liabilities is recorded by a credit to Unearned Photocopy Fees.

In-class Activities (2) Dr. Cash $1,300 Cr. Unearned Photocopy Fees $1,300 9. March 19: Performed a service by printing price lists for Ward Fashion Company and collected a check of $3,400. Analysis: Assets increased. Owner’s equity increased. Increases in assets are recorded by debits. Increases in owner’s equity are recorded by credits. Increase in assets is recorded by a debit to Cash. Increase in owner’s equity is recorded by a credit to Photocopy Fees Earned. Dr. Cash $ 3,400 Cr. Photocopy Fees Earned $3,400

In-class Activities (2) 10. March 24: George Ross withdrew $980 from the business for personal living expenses. Analysis: Assets decreased. Owner’s equity decreased. Decreases in asset are recorded by credits. Decreases in owner’s equity are recorded by debits. Decrease in owner’s equity is recorded by a debit to George Ross, Withdrawals. Decrease in assets is recorded by a credit to Cash. Dr. George Ross, Withdrawals $980 Cr. Cash $980

In-class Activities (2) 11. March 29: Received and paid the utility bill of $230. Analysis: Assets decreased. Owner’s equity decreased. Decrease in assets are recorded by Decreases in owner’s equity are recorded by debits. Decrease in owner’s equity is recorded by a debit to Utility Expense. Decrease in assets is recorded by a credit to Cash. Dr. Utility Expense $230 Cr. Cash $230

In-class Activities (2) 12. March 31: Received a telephone bill, $120. Analysis: Liabilities increased. Owner’s equity decreased. Increases in liabilities are recorded by credits. Decreases in owner’s equity are recorded by debits. Decrease in owner’s equity is recorded by a debit to Telephone Expense. Increase in liabilities is recorded by a credit to Accounts Payable. Dr. Telephone Expense $120 Cr. Accounts Payable $120

In-class Activities (3) Use T account to describe these transactions as the following: Cash 3/3. $20,000 3/7. $2,000 3/14 1,300 3/7. 2,300 3/19 3,400 3/8. 600 3/9. 3,100 3/24. 980 3/29 230 Bal. $15,490

In-class Activities (3) Accounts Payable 3/9. $3,100 3/7. $3,000 3/8. 3,100 3/31. 120 Bal. $3,120

In-class Activities (3) Unearned Photocopy Fees 3/14. $1,300 Bal. $1,300 • Accounts Receivable • 3/10 $6,000 • Bal. $6,000

In-class Activities (3) Photocopy Supplies 3/8. $2,300 Bal. $2,300 George Ross, Withdrawals 3/24. $980 Bal. $980

In-class Activities (3) Office Supplies 3/8. $8,00 Bal. $8,00 Photocopy Fees Earned 3/10. $6,000 3/19. $3,400 Bal. $9,400

In-class Activities (3) Prepaid Insurance 3/8. $600 Bal. $600 Utility Expense 3/29. $230 Bal. $230

In-class Activities (3) Photocopy Equipments 3/7. $2,000 Bal. $2,000 Telephone Expense 3/31. $120 Bal. $120

In-class Activities (3) Office Equipment 3/7. $5,300 Bal. $5,300

Further Practice 1. Exercise One on P37. Write proper words to fill in the following blanks. Try to find these words from the text. 2. Exercise Two on P38. Open the following T accounts: Cash; Repair Supplies; Repair Equipment; Accounts Payable; Skowron Yong, Capital; Skowron Young, Withdrawals; Repair Fees Earned; Salary Expense; and Rent Expense. Record the following Transactions for the month of August directly in the T account.

Further Practice 3. Exercise Three on P38. Tom Vega, after receiving his degree in computer science, began his own business called A Star System Company. He completed the following transactions soon after starting the business. Make entries to record these transactions. 4. Exercise Four on P38. Discuss the questions with your partners. 1) Some students believe debits are good and credits are bad, is it right? Why? 2) Why is the increase of expense recorded in the debit side?

Homework 1. Review Chapter 5 to get further understanding. 2. Finish the exercises in this chapter. 3. Prepare for the dictation for unit5. 4. Preview Chapter 6.