The Double Entry System

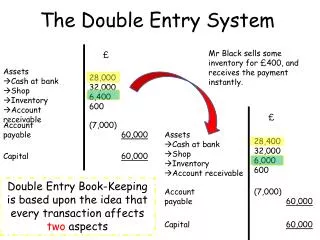

Mr Black sells some inventory for £400, and receives the payment instantly. . £. £. The Double Entry System. Assets Cash at bank Shop Inventory Account receivable. Assets Cash at bank Shop Inventory Account receivable. 28,400 32,000 6,000 600. 28,000 32,000 6,400 600.

The Double Entry System

E N D

Presentation Transcript

Mr Black sells some inventory for £400, and receives the payment instantly. £ £ The Double Entry System • Assets • Cash at bank • Shop • Inventory • Account receivable • Assets • Cash at bank • Shop • Inventory • Account receivable 28,400 32,000 6,000 600 28,000 32,000 6,400 600 Account payable Account payable (7,000) 60,000 (7,000) 60,000 Double Entry Book-Keeping is based upon the idea that every transaction affects two aspects Capital Capital 60,000 60,000

The accounts for double entry An ‘account’ is a record of all transactions in particular departments in a business.

The accounts for double entry • If a business buys stationary valued at £40 and pays for it using cash, then two things have happened. • The value in the business’s cash account will have decreased by £40 • The value in the business’s stationary account has increased by £40 Example: Paid cash for a van costing £3,000 Van comes IN to the Business (debit the van account) The cash goes OUT of the business (credit the cash account) IN OUT Dr Cr

The accounts for double entry Example: Paid cash for a van costing £3,000 Van comes IN to the Business (debit the van account) The cash goes OUT of the business (credit the cash account) VAN account Cash account Dr Cr Dr Cr Cash £3,000 Van £3,000 The owner starts the business with £10,000 in cash. Cash account Capital account Dr Cr Dr

Equipment is bought on credit from ‘B.B Company’ for £1,250 Equipment account B.B Company account Dr Cr Dr Cr You have paid the B.B Company the £1,250. B.B Company account Cash account Dr Cr Dr Cr

Now complete the double accounting work sheet Cut the margins Stick in book

Homework – Make and complete accounts using the following information. Jan 1 – Started Business with £30,000 in bank Jan 5 – Bought stock of goods paying £2,770 cheque Jan 7 – Bought a van, £4,800 cheque Jan 9 – Sold goods for £680 cash Jan 10 - Bought desk & chair for the office for £110 cash Jan 15 – Sold goods for £500 cheque Jan 22 - Paid £92 cash for motor expenses Jan 29 Sold goods for £325 cash Jan 30 – Bought more goods, paid £1090 cheque