Download

1 / 16

170 likes | 346 Vues

Unit Two: Market Equilibrium. Topic: Market Equilibrium. Learning Targets. I will be able to define market, market equilibrium, and price. I can determine market equilibrium quantity and price. I can determine what will happen to market equilibrium if supply or demand changes.

E N D

Unit Two: Market Equilibrium Topic: Market Equilibrium

Learning Targets • I will be able to define market, market equilibrium, and price. • I can determine market equilibrium quantity and price. • I can determine what will happen to market equilibrium if supply or demand changes. • I will understand what happens if the market is not in equilibrium. • I will understand how and why the government set prices in the market. • I will know the effects of government-set prices.

Market • Def: the interaction of consumers and producers; creates the price and quantity of a good or service for buyers and sellers. • In this class, we examine a perfectly competitive market where the good being sold is homogenous (the same) among producers. • All producers will sell at the market price.

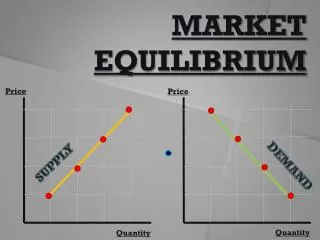

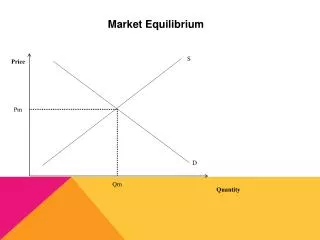

Market Equilibrium • Def: price and quantity where QS=QD (where the supply and demand curves intersect). Hot dogs P S P1 D Q Q1

Market Equilibrium • Price helps allocate scarce resources among competing uses (scarcity); consumers use demand to tell producers where they want the resources to go.

Questions • What happens to equilibrium price and quantity if supply increases? • What happens to equilibrium price and quantity if demand increases?

Changes in Supply or Demand Hot dogs Hot dogs P P S S P2 S2 P1 P1 P2 D2 D D Q1 Q2 Q Q1 Q2 Q Increase in S P ↓ Q ↑ Increase in D P ↑ Q ↑

Questions 3. What happens to equilibrium price and quantity if supply decreases? 4. What happens to equilibrium price and quantity if demand decreases?

Changes in Supply or Demand Hot dogs Hot dogs P P S2 S S P2 P1 Pe P2 D D2 D Q1 Q2 Q2 Q1 Q Q Decrease in S P ↑ Q ↓ Decrease in D P ↓Q ↓

Tip… • When demand changes, price and quantity will change in the same direction as demand. • When supply changes, price and quantity will move in opposite directions with quantity moving in the same direction as supply.

Disequilibrium • Def: market failure that occurs when QS ≠ QD OR when not all costs or benefits are reflected in the supply and demand curves.

Questions • What happens if the price is above equilibrium? • What happens if the price is below equilibrium?

Price Above Equilibrium Hot dogs S P Price above equilibrium QS>QD…we have a surplus! P1 D QD Q1 QS Q

Price Below Equilibrium Hot dogs S P QD > QS; we have a shortage! P1 Price below equilibrium D Q1 QS QD Q

Government Price Controls • Sometimes government sets prices in order to “help” some sector of the economy. • Gov’t will set price above equilibrium (price floor) in order to help producers. • This creates a surplus. • Gov’t will set price below equilibrium (price ceiling) in order to help consumers. • This creates a shortage.

Externalities • Def: market failures that occur when an added cost or added benefit are not shown on the supply or demand curves. • Positive externality: an additional benefit is being received by people who do not pay for the good or service. • Ex. Flu shots and other vaccinations • Negative externality: an additional cost is paid by someone other than the producer. • Ex. Pollution and traffic