Understanding Market Equilibrium: Demand, Supply, and Price Interaction

This unit explores market equilibrium, a state where the quantity supplied equals the quantity demanded. We examine scenarios of excess demand, where buyers want more than sellers can supply, and excess supply, where sellers produce more than buyers want. Key concepts include the market mechanism, the invisible hand, and the effects of price adjustments on demand and supply. Using real-world examples, such as the housing boom and the car market, we visualize equilibrium through supply-demand diagrams and illustrate how markets strive towards equilibrium in response to fluctuations.

Understanding Market Equilibrium: Demand, Supply, and Price Interaction

E N D

Presentation Transcript

The World Changes everyday…. • Take one random day: Monday April 7, 2008 • Nike announced the Hyperdunk • Copper prices went over $8,600/ton • The EPA announced $74 million in grants to help communities clean-up polluted industrial sites • The population of China grew by about 22,000 people

What we look at in this unit • What happens when buyers want more than sellers are prepared to produce? • Or when seller produce more than buyers are prepared to consume? • We will look at market equilibrium • We will look at how buyers and sellers react to shifts that push markets away from equilibrium. • We will look at the basics of elasticity of demand and supply.

The Case of Excess Demand • A market has excess demand if buyers want more than sellers are prepared to supply at the current market price. • Examples: Housing boom of 2003-2005 – bidding wars were created and houses started selling for more than the asking price. • The employment market for nurses – combination of an aging population & unwillingness to raise wages

The Case of Excess Supply • Markets occasionally suffer from excess supply – when suppliers are willing to sell more at the market price than buyers are prepared to pay for. • Examples: Restaurants with few customers tend to be a sign of overpriced bad food – resulting in thousands of restaurants going out of business each year.

The Invisible Hand • These situations tend to frustrate sellers and disappoint buyers. • How do markets react to a gap between quantity supplied and quantity demanded? • The difference is usually closed by the market mechanism or the invisible hand.

The Invisible Hand • The reason the mechanism is invisible is that no central planning agency has to issue explicit orders to close the supply-demand gap. • Buyers and seller act on their own. • Excess supply usually puts downward pressure on prices.

The Invisible Hand • A lower price simultaneously increases the quantity demanded and reduces the quantity supplied. • Similarly, excess demand usually puts upward pressure on prices. Quantity demanded decreases

Market Equilibrium • Most markets will eventually reach a market equilibrium. • This is when the quantity supplied and the quantity demanded are equal. • Prices move up or down; buyers change the amount they demand and seller adjust the quantity they supply.

Market Equilibrium • The price at which the quantity supplied equals the quantity demanded is the equilibrium price. • At the equilibrium price, there’s a match between how much buyers want and how much sellers are willing to supply. • Equilibrium quantity is the quantity supplied and demanded at the equilibrium price.

Market Equilibrium • Example: The market for hotel rooms would be at equilibrium if all hotel rooms were filled, but there were no potential guests standing outside in the cold with no place to sleep. • In reality, few markets are exactly at equilibrium price. • Most markets are naturally trying to achieve equilibrium and many are near equilibrium.

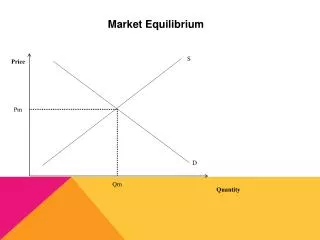

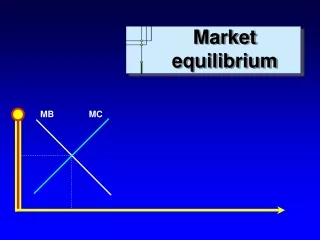

Basic Supply-Demand Diagram • Market equilibrium can be shown by drawing the market supply and demand curves on the same graph. • The price at which the two lines intersect is the equilibrium price. • At that price, quantity supplied is equal to quantity demanded: the equilibrium quantity.

Basic Supply-Demand Diagram • Figure 3.1

Basic Supply-Demand Diagram • This figure is perhaps the most famous and useful diagram in economics. • In this figure, the equilibrium price is P, and the equilibrium quantity is Q. • Think about it this way: buyers & sellers make decisions independently from each other.

Basic Supply-Demand Diagram • At the equilibrium price, it happens that the quantity picked by suppliers is equal to the quantity chosen by sellers. • Example: New vehicle market • Demand curve for new cars is downward sloping (consumers will buy if the price is low) • The supply curve for cars is upward-sloping: if dealers can get more $$ for each vehicle, manufacturers hire more workers, run the assembly lines longer, or bring in more vehicles from overseas.

Basic Supply-Demand Diagram • Figure 3.2 illustrates the 2006 market equilibrium in the new car and light truck market. • At an average price of $28,500, vehicle manufacturers were willing to supply 16.5 million vehicles to the market. • Buyers were willing to shell out $28,500 to take home 16.5 million vehicles.

Equilibrium in Numbers • Numerical examples of market equilibrium: • Go-karts are made mostly by Asian companies • Price range: $600 to $2,000+ • Max speed: 35-40 mph • Made for kids and adults • Quantity supplied and quantity demanded are price sensitive

Equilibrium in Numbers • Demand side: strictly a discretionary purchase; prices rises too much, buyers put off the purchase • Supply side: the same factories that make go-karts can also make a wide range of other products; scooters and golf carts • Easy to switch workers back and forth

Equilibrium in Numbers • Using Table 3.1 (Supply and Demand in the Go-Kart Market), determine the equilibrium price for go-karts. • What is the equilibrium quantity?

Market Shifts • Markets are continually bombarded by outside forces • The shifts that occur are called market shifts. • A demand shift is a market shift that affects buyers • Changes the amount buyers want to purchase at any given price.

Market Shifts • A supply shift affects sellers by either raising or lowering the amount they supply at any given price. • A market shift will change the market equilibrium. • Example: If the demand curve shifts to the left, that will temporarily create a situation of excess supply, which tends to drive the price until a new equilibrium is reached.

Supply Schedule for Helen’s Haircutting Salon • Price Per Haircut • (Dollars) • $ 5.00 • $10.00 • $15.00 • $20.00 • $25.00 • $30.00 • $35.00 • Quantity Supplied • (Haircuts Available in a Week) • 40 • 60 • 80 • 100 • 120 • 140 • 160 For any price of a haircut, this table reports how many haircuts are supplied.

How Price Affects Quantity Supplied • The market supply schedule adds up the quantity supplied by all the sellers in a market. • Example: Suppose there are 10 haircutting salons in town, all with the same supply schedule as Helen’s Salon. Then if the haircut is $20, there will be a total of 1,000 haircuts supplied (1000 haircuts x 10 stores).

The Law of Supply • Says that higher prices tend to increase the quantity supplied of a good or service, assuming nothing else changes. • If the price a business can get for its goods and services rises, it has an incentive to increase production.

The Law of Supply • The law of supply operates in global markets as well. • Suppose a department store chain is selling blue shirts imported from China. If the price of that kind of shirt goes up, the department store chain will order more shirts from its supplier in China. The Chinese factory will need a little time to respond because it must hire more workers and train them.

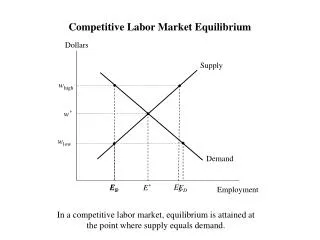

The Law of Supply • A key market where the law of supply generally holds true is the labor market. • The price of labor is the wage rate (what the worker is paid) • A higher wage rate will not have much effect on the labor supplied by people who are already working full-time.

The Law of Supply • However, higher wages do tend to increase the labor supply of people who are less committed to working. • Like the law of demand, the law of supply does not hold true in every circumstance. • In some cases, an increased price can lower supply. • Ex: If you need to work 200 hrs. at $10/hr. to earn $2,000; you will only need to work 100 hrs. if you wage increases to $20/hr.

Graphing the Supply Schedule • Just as we did with the demand schedule, we can plot the supply schedule for a market on a graph. • Going up the vertical axis are the various prices that could be charged. • Going across the horizontal axis is the quantity supplied.

Graphing the Supply Schedule • To plot the supply schedule, we start with the price on the vertical axis and move right horizontally until we come to the number supplied. • Plotting all the combinations on the supply schedule and then connecting the points gives us the supply curve. • The supply curve shows the link between the price & the quantity supplied.

Graphing the Supply Schedule • The result is an upward-sloping supply curve that starts at the lower left corner and goes to the upper right corner of the graph. • Real world supply curves are generally not straight.

Graphing the Supply Schedule • Insert Figure 2.2

New Markets • Demand & supply schedules describe how buyers and sellers behave in existing markets, but the number of markets is not fixed. • New markets are created every day to meet the changing needs of consumers and to take advantage of the changing capability of producers.

New Markets • New markets can provide new products or services, or bring in new buyers and sellers. • Some goods & services we buy today were not available 10, 20, or 30 years ago. • iPods, cell phones, Amazon.com, One Direction throw pillows, PS4, X-Box1, web design, etc. • As income rises in developing countries, new markets open up.