Native Asset Building Initiative

480 likes | 631 Vues

Native Asset Building Initiative. May 30, 2013 Presented by Christy Finsel, AFI Resource Center For Further Information: Heather Wiley, Program Specialist, Assets for Independence, (202) 401-5633, Heather.Wiley@acf.hhs.gov

Native Asset Building Initiative

E N D

Presentation Transcript

Native Asset Building Initiative May 30, 2013 Presented by Christy Finsel, AFI Resource Center For Further Information: Heather Wiley, Program Specialist, Assets for Independence, (202) 401-5633, Heather.Wiley@acf.hhs.gov Christina Clark, Program Specialist, Administration for Native Americans, (202) 401-5399, Christina.Clark@acf.hhs.gov

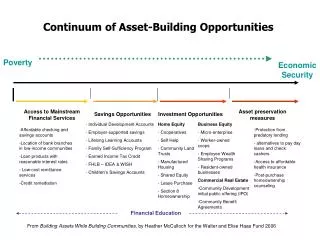

What is Asset Building? Asset building is an anti-poverty strategy that helps low-income people move towards greater self-sufficiency by accumulating savings and purchasing long-term assets. A comprehensive asset building approach includes strategies such as financial education, credit and debt repair, federal benefits maximization, outreach on Earned Income Tax Credits (EITC) and other federal tax benefits, getting the unbanked to bank, and encouraging savings and Individual Development Accounts (IDAs). 2

Asset Building Tools • There are a variety of tools we can use to build assets. • These tools can help us build a number of assets at the same time (integrated asset building). Christy Finsel, January 8, 2010.

Examples of Asset Building Tools • Earned Income Tax Credits/Voluntary Income Tax Assistance • Financial education • Job training/job creation • Internships • Child savings accounts • Retirement plans • Education • Land purchase • Small business development • Native language programs • IDAs Christy Finsel, January 8, 2010.

What is an Individual Development Account (IDA)? IDAs are matched savings accounts held by low-income individuals for designated purposes. As part of a structured program, regular savings in these accounts are matched by funding from private and public sources. By rewarding individuals for saving, IDA programs encourage people to develop savings habits, to manage their savings wisely, and to use them to acquire economic assets that will appreciate over time-such as to purchase a home, to engage in post-secondary education or to start a business. 5

What is the Native Asset Building Initiative (NABI)? The Native Asset Building Initiative (NABI) is a joint funding opportunity, offered through a partnership between the Office of Community Services (OCS) Assets for Independence (AFI) program and ANA's Social and Economic Development Strategies (SEDS) program. The Initiative's goal is to build capacity for Native communities to offer financial literacy, asset building, and related services to more families. 6

NABI and IDAs: An Essential Piece for Any Project Submitted under the NABI Funding Opportunity Announcement Must be the IDA Program How does an AFI IDA work? • Save earned income: AFI IDA participants contribute earned income to a special matched savings account, known as the Individual Development Account (IDA). • Receive match funds: For every dollar a participant saves in his/her IDA account, he/she is matched any where from $1 to $8. • The match funds come from AFI funding and non-Federal funding. • Participants can receive match funds up to $2,000 per individual, or $4,000 per household from the AFI grant award and at least an equal amount from non-Federal funds. • Purchase an Asset: After saving earned income in the IDA for at least 6 months, participants can use their IDA savings and match funds to purchase a first-time home, start or expand a business, or pursue postsecondary education. 7

Additional Asset Development Services In addition to the IDA account, NABI funds can be used to support the following comprehensive asset development services: • Financial Education: Financial literacy, debt management, credit building, and credit repair services. • Support for Earned Income : Workforce development and job placement services, entrepreneurial education, Volunteer Income Tax Assistance. • Home Ownership Assistance: Homebuyer and home ownership education classes. • Secondary Education Assistance: FAFSA completion, college application assistance. • Program Support: Curriculum adaptation and development, staff training and certification. 8

NABI: Benefits to Community • Help individuals save for and purchase assets more quickly than if they were saving on their own for an asset purchase such as a home. • Participants continue to develop their savings habits and increase their financial literacy. • Increased financial stability for families in community. • NABI funds cover the administration of an IDA project. • NABI funds cover costs for other related comprehensive asset building strategies. Christy Finsel, 2013. 9

Notes on NABI Awards • If applying for NABI, you should ask for an award that you can realistically draw down as you do not want to return unused ANA or AFI funds, if you can help it. • Also, NABI grantees, like AFI grantees, must have firm commitments of cash support from nonfederal sources, prior to applying for the grant and, if awarded, must deposit these nonfederal funds in a Project Reserve Fund for the duration of the grant award. An example is found below. Christy Finsel and AFI, 2010. 10

Asset Savings Goals/Allowable Uses • Purchasing a home or repairing a home that is recently purchased (to get it to code). You are considered a first-time home buyer if you haven’t owned a home within the past three years. • Starting a small business and paying for equipment, supplies, and other costs • Paying for post-secondary education/training, including necessary equipment such as books, computers, and so forth. (Please note: you can’t put AFI IDA funds into a 529 College Savings Plan) • In addition, AFI allows transfer of funds to enable a spouse or child to purchase any of these economic assets. 11

Example of the Funds To Administer an AFI Project • AFI awards leverage non-federal funds dollar for dollar. • So, if you have an AFI Award: $142,500 in Federal AFI funds • You’d need to have $142,500 in Non-Federal funds • The total funding secured would be $285,000. Christy Finsel, 2010. 12

Of the $285,000 Total Funding Secured 85% for Matching of Funding Sources 15% for Operations $42,750 total is available for operations. Of this $21,375 is AFI funding The other $21,375 is non-AFI funding • $242,250 total is available for match funds. • Of this $121,125 is AFI funding • The other $121,125 is non-AFI funding Christy Finsel, 2010. 13

SEDS Funds Determine What is Needed to Make the IDA Program Successful: • Staff/Staff Training • Curricula • Supplies • Advertising • Office Space/Utilities Christina Clark, ANA, 2013.

Example of a SEDS Budget Federal Funds $200,000 80% Non Federal Share $50,000 20% Administrative Assistant $30,000 Fringe $4,500 Office Space $10,000 Credit Builder Training $5,500 * Applicant match for the SEDS grant can be in-kind contributions • Project Director $65,000 • IDA Administrator $55,000 • Fringe Benefits $14,250 • Computers and Office Supplies $8,000 • Financial Literacy Curricula $7,000 • Financial Literacy Instructors $20,000 • Staff Training Event $12,000 • Youth IDAs $10,000 • Utilities $8,750 Christina Clark, ANA, 2013.

Who Can Apply for a NABI Grant? Eligible applicants include: • Federally recognized tribal governments or Alaska Native Villages, as defined in the Alaska Native Claims Settlement Act, that are joint applicants with a 501(c)(3) Native non-profit organization • Native 501(c)(3) non-profits serving Native Americans • Native non-profit organizations designated by the Secretary of the Treasury as Community Development Financial Institutions (CDFIs) or Native non-profit credit unions designated as low-income credit unions by the National Credit Union Administration (NCAU) – CDFIs and credit unions must demonstrate a collaborative relationship with a local community-based organization whose activities are designed to address poverty and the needs of community members for economic independence and stability 16

Who Can Apply Continued If a tribe has a 501(c)3 in their community, they would not have to partner with a 501(c)3 external to their community. An example of this is the Choctaw Nation, located in Durant, Oklahoma. They partnered with the Chahta Foundation, an existing 501(c)3 in their Nation. In this case, the Choctaw Nation is the direct grantee. Some Native communities are partnering with a network or consortium to access AFI funds. These networks or consortiums may be willing to be flexible when signing a Memorandum of Understanding (MOU) with a sovereign nation. Christy Finsel and Sharon Henderson. Effective Use of Assets for Independence (AFI) Funds by American Indian, Alaska Native, and Native Hawaiian Communities,for Assets for Independence, under review, January 2010. 17

Examples of Those Who Might Apply for the NABI • Tribal colleges (you could use current sources of funding for scholarships as the match for a NABI application) • Native Community Development Financial Institutions (CDFIs) • Native Housing Authorities • Native nonprofits

Savings Match • Participants receive matching funds for money deposited into their IDA. • Match amount ranges from $1-$8 for each $1 of earned income saved. (About three-quarters of programs offer $2 to $3 in matching funds for each $1 saved in an IDA). • A maximum amount of $2,000 in Federal AFI funds may be used to match a participant’s IDA savings. Federal funds provided to match participant savings must be combined with an equal amount of nonfederal funds. 19

Arrangement with a Financial Institution AFI requires that participant IDA accounts must be maintained in one or more Federally-insured financial institutions (where one is not available, a State-insured institution). For your application, you will need a signed agreement with a financial institution. 20

Account Features and Arrangement with a Financial Institution • Account Ownership AFI requires that AFI-funded IDA accounts must be custodial or trust accounts. In such accounts, the IDA program manager has control over withdrawals. • Account Statements Monthly statements to the IDA or quarterly statements. IDA account manager access to information about the accounts to monitor the savings pattern. • Deposit Format Will you require electronic funds transfer or will you allow for deposits at branches and ATMs? 21

Managing the Project Reserve Fund • This fund holds the federal grant funds plus at least an equal amount of nonfederal funds that are committed to the AFI project. • This fund is a separate account that only holds your IDA project funds. • All funds-Federal and nonfederal funds that are deposited into this account are subject to the Office of Community Service rules for the AFI program. These rules state that not less than 85 percent of non-federal and federal funds in the Project Reserve Fund must be available to match participant IDA savings. Of the remaining 15 percent (to be used for project support), up to 13 percent may be used for administrative purposes and up to 2 percent for data collection and evaluation. Keep in-kind and other money in a separate account because anything put in the Project Reserve Fund is subject to the 85/15% rule. • It is recommended that you use a no-risk investment strategy for these funds such as a CD or high interest savings account. 22

Regarding Interest from the Project Reserve Account • The interest earned on the 85% of match funds can go to participants. There are various ways to calculate the interest (in real time based on what participant has saved or divided uniformly and distributed at the time when the participant is purchasing their asset). • Interest earned on the 15% can be used for program related activity. • You are to track and report the interest but AFI does not ask you to break down how you will distribute the interest. AFI, 2010. 23

A Financial Institution Will: • Set up interest-bearing custodial or trust savings accounts for IDA participants (hopefully, with no monthly fees and no minimum balance). • Establish the Reserve Account to hold both the nonfederal cash contribution and Federal funds in the name of the sponsoring organization. • Provide monthly (or quarterly) account statements to participants. • Provide monthly (or quarterly) account activity information to the sponsoring organization, on paper and/or electronically. • Offer other banking services to participants (checking accounts, mortgages, loans, other savings, or investment accounts). Some may provide fee-free banking but some won't, so look around for the best deal. • Assist in financial education. • Enhance visibility of program. • Contribute nonfederal cash support. 24

TANF-eligible in their state OR Meet both of the following two criteria Income: twice the poverty guidelines (about $44,000 for family of four) OR EITC eligible AND Net worth: maximum $10,000 (less one residence/one vehicle) Administrating agencies may apply additional eligibility rules NABI Participant Eligibility

Community and Organizational Assessment • What are the community needs in terms of asset building? What IDA asset purchases are the community interested in making? • What resources do you have already that you could bring to this project (staff, experience with an IDA project, community partners willing to offer financial education to your IDA participants, etc.?) • What is your organizational capacity to administer an IDA program? With additional funding from SEDS, could you build the capacity you need to administer an IDA program? • Who are your potential partners (financial institutions you already bank with, a Voluntary Income Tax Assistance site in your area, etc.)? Christy Finsel, 2010. 27

Developing Your IDA Project • There are a number of components to determine when designing an IDA program (target market, eligibility requirements, savings goals, match rate, savings period, etc.) • Besides financial education, what other comprehensive asset building strategies would you like to offer to your IDA participants (credit repair, connections to a Voluntary Income Tax Assistance site, FAFSA completion, job placement services, etc.)? Christy Finsel, 2010. 28

Determine your IDA partners, the roles and responsibilities of those working with your IDA project, and their capacity to participate in the project. Roles and Responsibilities 29

Securing Sources of Non-Federal Funds for a NABI Application Financial institutions and their foundations State and local governments Tribal governments United Way Foundations (local, regional, national) State/Local tax credits Special needs funding opportunities (Mental Health, Youth Programs, Disability Programs, and other nonfederal funding streams that target specific populations) Locally-based corporations/employers Places of worship Individuals/online donations Sponsoring organization funds Federal Home Loan Banks Community Development Block Grants Making the Business Case: http://www.idaresources.org/IDA_Fundraising 30

Raising Non-Federal FundsExamples from Native AFI Projects • National financial institutions, private/local financial institution, community development financial institutions, and credit unions • State funds • Alaska Mental Health Trust Fund (as in the case of the Cook Inlet Lending Center) • Tribal contributions • Citi Foundation, Bush Foundation, Scott Evans Foundation, and the Northwest Area Foundation Christy Finsel and Sharon Henderson. Effective Use of Assets for Independence (AFI) Funds by American Indian, Alaska Native, and Native Hawaiian Communities,for Assets for Independence, under review, January 2010 31

Additional Approved Funding Sources for a NABI Application • Indian Community Development Block Grant Program (ICBDG), Native American Housing Assistance and Self-Determination Act (NAHASDA), and Public Law 93-638 (the Indian Self-Determination and Education Assistance Act) are now allowed for use as non-federal match. Christy Finsel and Dan Van Otten, 2010.

Suggestions from AFI for Sources of Non-Federal Funds and Program Designs • Tribal Colleges leveraging scholarship or foundation funds for the non-federal match and partnering with Federal Work Study, allowing student participants to earn income for post-secondary education IDAs. • Tribal leaders forming Microenterprise Development Organizations and leveraging the USDA Rural Microentrepreneur Assistance Program with NABI to assist small business growth. • Leveraging NAHASDA's Indian Housing Block Grant (IHBG) and Title VI Loan Guarantee with established non profits housing agencies such as Habitat for Humanity with NABI to increase new housing opportunities. Heather Wiley, AFI, 2013.

Outputs are the direct products of a program’s activities. Outputs must be described in measureable or quantifiable terms that can be used to monitor and assess the proposed project’s progress. Outputs are often measured in terms of the volume of work accomplished. In an IDA project outputs often include: The number of participants enrolled in the project The number of participants who establish IDAs The number of participants who complete their financial literacy training Determining Your Outputs and Outcomes 34

Outcomes = Benefits/Results/Change • Outcomes are measurable results and benefits for the community and community members. • Outcomes are changes in conditions that are the result of project operation. • Examples of outcomes: • An increase in household incomes. • An increase in families living in affordable and uncrowded housing. • A decrease in unemployment rates. 35

Develop the Budget and Budget Justification • The project budget is one of the last components of project development. • Ensure that costs included in the budget are reasonable, realistic and relevant to the workplan. • Be sure that proposed expenditures comply with AFI and ANA SEDS requirements. 36

PROPOSAL CONTENT WEAKNESSES • Little or no evidence of community involvement in defining problems that will be addressed by the project, design of the project and evaluation of project benefits. • Little or no community-specific information or adequate description of and documentation regarding problems that are impacting the community that the project will address. • Project outcomes that are written in broad, descriptive terms with no measurable results and unclear timeframes for completion of key activities. • Incomplete documentation on critical issues (no discussion of contingency plans, for example). • No firm commitment of leveraged resources to the project for its implementation or to sustain it after the end of project funding or a detailed description of how the project will be sustained. 37

NABI Summary • NABI combines complementary funding streams from two ACF offices, OCS-AFI and ANA-SEDS, to fund a single project that implements a comprehensive asset building strategy. • The comprehensive asset building strategy must include an Individual Development Account (IDA) component. • The IDA component consists of an AFI IDA participant contributing earned income to a savings account, receiving match savings contributions, and making an asset purchase. • Match contribution funds must come from both the AFI grant and non-Federal cash contributions. • The comprehensive asset building strategy may also include financial education, credit repair, tax services, workforce development, and other activities that support financial self sufficiency and asset accumulation. • SEDS funds may be used to fund the additional asset building strategies, as well as program administration costs. 38

FOA Information • The 2013 Funding Opportunity Announcement (FOA) will be posted on Grants.gov. • To see the 2012 FOA, please go to: http://www.acf.hhs.gov/grants/open/foa/view/HHS-2012-ACF-ANA-NO-0322 40

A Few Notes Regarding Submitting a NABI Application ACF requires electronic submission of applications at www.Grants.gov. Applicants that do not have an Internet connection or sufficient computing capacity to upload large documents to the Internet may contact ACF for an exemption that will allow these applicants to submit an application in paper format. Information on requesting an exemption from electronic application submission is found in Section IV.2. Application Submission Options. 41

Regarding Submitting a NABI Application All applicants must have a DUNS number (www.dnb.com) and be registered with the System for Award Management (SAM, www.sam.gov) and maintain an active SAM registration until the application process is complete, and should a grant be made, throughout the life of the award. Finalize a new, or renew an existing, registration at least two weeks before the application deadline. This action should allow you time to resolve any issues that may arise. Failure to comply with these requirements may result in your inability to submit your application or receive an award. Maintain documentation (with dates) of your efforts to register or renew at least two weeks before the deadline. See the SAM Quick Guide for Grantees at: https:// www.sam.gov /sam /transcript /SAM_Quick_Guide_Grants_Registrations-v1.6.pdf. 42

ACF Application Upload Requirements This Fiscal Year (FY 2013) ACF has implemented a new application upload requirement. Each applicant applying electronically via www.grants.gov is required to upload only two electronic files, excluding Standard Forms and OMB-approved forms. No more than two files will be accepted for the review, and additional files will be removed. Standard Forms and OMB-approved forms will not be considered additional files. Please see Section IV.2 Content and Form of Application Submission for detailed information on this requirement. 43

If your community is ready to learn more about the Native Asset Building Initiative, here are some further resources:

Support for NABI Grantees • There is technical assistance (TA) available through ANA and AFI. For further information about ANA TA, go to: http://www.acf.hhs.gov/programs/ana/assistance/applicant-training-technical-assistance. For TA from AFI, contact Heather Wiley at Heather.Wiley@acf.hhs.gov or (202) 401-5633. • Some NABI grantees have hired Native asset building consultants to provide them with TA. • There are several Native asset building coalitions nationally that provide free training and technical assistance to Native communities designing and implementing IDAs. Some of these Native coalitions also provide peer-learning calls and opportunities for face-to-face roundtable discussions to share Native IDA best practices and models. • There are loose peer networks of Native IDA practitioners nationally who share sample documents. Christy Finsel, 2013. 45

Helpful Contacts AFI Resource Center: AFI Resource Center Office of Community Services 370 L'Enfant Promenade, S.W. 5th Floor, West Washington, DC 20447 Telephone: 1-866-778-6037 E-mail: info@idaresources.org AFI Program Website: www.acf.hhs.gov/assetbuilding AFI Resource Center Website: www.idaresources.org ANA Help Desk: Administration for Native Americans 370 L'Enfant Promenade SW Aerospace Building, 2nd Fl-West Washington, DC 20447 Telephone: 1-877-922-9262 Email:NativeAssetBuilding@acf.hhs.gov ANA Website: http://www.acf.hhs.gov/programs/ana/index.html 46

NABI Specific Contacts Christina Clark, Program Specialist, Administration for Native Americans, (202) 401-5399, Christina.Clark@acf.hhs.gov Heather Wiley, Program Specialist, Assets for Independence Program, (202) 401-5633, Heather.Wiley@acf.hhs.gov