Understanding Present and Future Value: The Essentials of Cash Flow Analysis

This comprehensive guide delves into the concepts of present and future value, emphasizing the power of compounding interest and cash flow analysis. Learn how to calculate future values (FV) to determine how much you'll have in the future based on various investment rates and time frames. Discover the significance of present value (PV) in discounting future cash flows, understanding opportunity costs, and valuing cash flows over time. Additionally, learn about annuities, perpetuities, and the internal rate of return (IRR) as key concepts for effective financial decision-making.

Understanding Present and Future Value: The Essentials of Cash Flow Analysis

E N D

Presentation Transcript

Present and Future Value Translating cash flows forward and backward through time

Future Value • Money invested earns interest and interest reinvested earns more interest • The power of compounding

Future Value Problems Solve for any variable, given the other three • FV: How much will I have in the future? • P: How much do I need to invest now? • r: What rate of return do I need to earn? • T: How long will it take me to reach my goal?

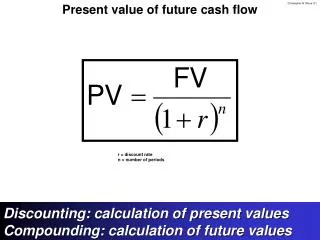

Present Value • Discounting future cash flows at the “opportunity cost” (cost of capital, discount rate, minimum acceptable return) • A dollar tomorrow is worth less than a dollar today

Present Values can be Added • Cash flows further out are discounted more • Discount factors are like prices (exchange rates)

Calculating PV of a Stream (Beware) • Calculator assumes first CF you give it occurs now (Time 0) • Excel assumes first CF you give it occurs one year from now (Time 1)

Different Compounding Periods • m = # of compounding periods in a year • APR = actual rate x m (APR is annualized) • EAR = the annually compounded rate that gives the same proceeds as APR compounded m times

Semiannual Compounding • m = 2 • APR = 10% • EAR = 10.25%

Quarterly Compounding • m = 4 • APR = 10% • EAR = 10.38%

Monthly Compounding • m = 12 • APR = 10% • EAR = 10.47%

Daily Compounding • m = 365 • APR = 10% • EAR = 10.516%

Continuous Compounding • m = • APR = 10% • EAR = 10.517%

Annuities • All cash flows are the same, so we can factor out the constant payment C and calculate the sum of the discount factors

Special Case: Perpetuity • If all the cash flows are the same each period forever, the sum of the discount factors converges to 1/r

Perpetuity Example • Let C = $100 and r = .05 • $100 per year forever at 5% is worth:

Other Perpetuity Examples • British Consol Bonds • Canadian Pacific 4% Perpetual Bonds • Endowments • How much can I withdraw annually without invading principal?

Growing Perpetuity • Suppose the initial payment C grows at a constant rate g per period (where g < r) • This growing stream still has a finite present value:

Growing Perpetuity Example • Suppose the initial payment is $100 and that this grows at 3% per year while the discount rate is 5% • The value of this growing perpetuity is:

Other Growing Perpetuity Examples • Stock price = present value of growing dividend stream (see Class #7) • M&A: How to estimate terminal value • How fast do earnings grow after the end of the analysis period?

Finite Annuity=Difference Between Two Perpetuities C C C C C C C C 0 1 2 3 4 5 6 7 8 C C C C

Annuity Example • What’s the value of a 4-year annuity with annual payments of $40,000 per year (@5%)?

Other Annuity Applications • Lottery winnings • Lease & loan contracts • Home mortgages • Retirement savings/ income

Home Mortgages • 30-year fixed rate mortgage: 360 equal monthly payments • Most of early payments goes toward interest; principal repayment gradually accelerates • At any point: outstanding balance = present value of remaining payments

More Annuity Problems Saving, Retirement Planning, Evaluating Loans and Investments

Net Present Value (NPV) • Best criterion for corporate investment: • Invest if NPV > 0

NPV with a Single, Initial Investment Outlay • I = initial investment outlay • Ct= project cash flow in period t • r = discount rate (shareholders’ opp. cost) • T = project termination period

Implications of NPV > 0 • Project benefits exceed cost (in PV terms) • Project is worth more than it costs • Project market value exceeds book value • Project adds shareholder value

NPV More Generally • Treat inflows as +, outflows as – • NPV = PV of all cash flows • Investment may occur throughout project life

Internal Rate of Return • IRR sets value of benefits = investment • IRR sets NPV = 0 • IRR is the rate of return company expects on investment I

NPV > 0 Implies IRR > r • If NPV > 0, IRR must exceed r • Investing when NPV > 0 implies company expects to earn more than shareholder’ opp. Cost • Equivalent: Invest when NPV > 0 or when IRR>I