Download

1 / 67

670 likes | 811 Vues

Learn the concepts of future and present value, rates of return, and amortization schedules. Understand compounding and discounting methods to calculate financial values. Explore ways to find values using tables, calculators, spreadsheets, or algebraic solutions.

E N D

CHAPTER 7Time Value of Money • Future value • Present value • Rates of return • Amortization

Time lines show timing of cash flows. 0 1 2 3 i% CF0 CF1 CF2 CF3 Tick marksat ends of periods, so Time 0 is today; Time 1 is the end of Period 1; or the beginning of Period 2.

Time line for a $100 lump sum due at the end of Year 2. 0 1 2 Year i% 100

Time line for an ordinary annuity of $100 for 3 years. 0 1 2 3 i% 100 100 100

Time line for uneven CFs -$50 at t = 0 and $100, $75, and $50 at the end of Years 1 through 3. 0 1 2 3 i% -50 100 75 50

What’s the FV of an initial $100 after 3 years if i = 10%? 0 1 2 3 10% 100 FV = ? Finding FVs is compounding.

After 1 year: FV1 = PV + INT1 = PV + PV(i) = PV(1 + i) = $100(1.10) = $110.00. After 2 years: FV2 = PV(1 + i)2 = $100(1.10)2 = $121.00.

After 3 years: FV3 = PV(1 + i)3 = $100(1.10)3 = $133.10. In general, FVn = PV(1 + i)n.

Four Ways to Find FVs • Solve the equation with a regular calculator. • Use tables. • Use a financial calculator. • Use a spreadsheet.

Algebraic Solution FVn = PV(1 + i)n. FV3 = 100(1 + .10) 3 FV3 = 100(1.331) = 133.10

Solution Using Tables FVn = PV(FVIF i,n). FV3 = 100(FVIF 10%, 3) Use FVIF table from pages A-6 & 7, Table A3 FV3 = 100(1.331) = 133.10

Financial Calculator Solution Financial calculators solve this equation: There are 4 variables. If 3 are known, the calculator will solve for the 4th. FVn = PV(1 + i)n.

Here’s the setup to find FV: INPUTS 3 10 -100 0 N I/YR PV PMT FV 133.10 OUTPUT Clearing automatically sets everything to 0, but for safety enter PMT = 0. Set: P/YR = 1, END

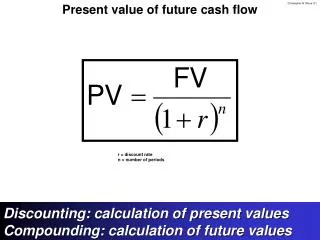

What’s the PV of $100 due in 3 years if i = 10%? Finding PVs is discounting, and it’s the reverse of compounding. 0 1 2 3 10% 100 PV = ?

( ) 1 1 + i FVn (1 + i)n PV = = FVn . ( ) 1 1.10 Solve FVn = PV(1 + i )n for PV: n PV = $100 = $100(PVIFi,n) Table A1 = $100(0.7513) = $75.13. So the (PVIF 10%,3) = .7513 3

Financial Calculator Solution INPUTS 3 10 0 100 N I/YR PV PMT FV -75.13 OUTPUT Either PV or FV must be negative. Here PV = -75.13. Put in $75.13 today, take out $100 after 3 years.

If sales grow at 20% per year, how long before sales double? Solve for n: FVn = $1(1 + i)n; $2 = $1(1.20)n ln 2 = ln 1.2n .693147=.18232n 3.801 = n Use calculator to solve, see next slide.

If sales grow at 20% per year, how long before sales double? Solve for n: FVn = PV(FVIF i,n); $2 = $1(FVIF 20,n) 2.00 = (FVIF 20,n) n between 3 and 4 years 1.728 and 2.0736 Use calculator to solve, see next slide.

INPUTS 20 -1 0 2 N I/YR PV PMT FV 3.8 OUTPUT Graphical Illustration: FV 2 3.8 1 Year 0 1 2 3 4

Compound GrowthHow do you find the compound growth rate for your company to analyze sales growth ? Can use either PV or FV formula, use FV 1062021 (1 + i )9 = 5284371 (1 + i )9 = 5284371/1062021 (1 + i)9 = 4.976 (1 + i) = 4.976 .111 (1 + i) = 1.195 i = .195 or 19.5%

Tabular Solution Use PV formula and table A-1 5284371 (PVIF i,9) = 1062021 PVIF i,9 = 1062021/5284371 PVIF i,9 = .20097 Use table A-3, for 9 Periods, find .20097 i is between 18% and 20%

Calculator Solution, Compound Growth INPUTS 9 -1062021 0 5284371 N I/YR PV PMT FV 19.51 OUTPUT

What’s the difference between an ordinaryannuity and an annuitydue? Ordinary Annuity 0 1 2 3 i% PMT PMT PMT Annuity Due 0 1 2 3 i% PMT PMT PMT

What’s the FV of a 3-year ordinary annuity of $100 at 10%? 0 1 2 3 10% 100 100 100 110 121 FV = 331

Algebraic Solution FVA =( PMT)* ( 1 +i)n – 1 I FVA =( 100)* ( 1 + .1)3 – 1 .1 FVA =( 100)* 1.331 – 1 = 100 * 3.31 = .1 FVA = 331.00

Tabular Solution FVA i,n =( PMT) * (FVIFA i,n ) Use Table A-4 on pages A-8 & 9 FVA 10%,3 =( 100) * (FVIFA 10%,3) FVA 10%,3 =( 100)* 3.31 = FVA 10%,3 = 331.00

Financial Calculator Solution INPUTS 3 10 0 -100 331.00 N I/YR PV PMT FV OUTPUT Have payments but no lump sum PV, so enter 0 for present value.

What’s the PV of this ordinary annuity? 0 1 2 3 10% 100 100 100 90.91 82.64 75.13 248.68 = PV

Algebraic Solution 1 . PVA =( PMT)* 1 – (1 + i)n i 1 . PVA =( 100) * 1 – (1 + .1)3 .1 PVA =( 100)* 1 - .7513 = 100 * 2.48685 = .1 PVA = 248.69

Tabular Solution PVA i,n =( PMT) * (PVIFA i,n ) Use Table A-2 on pages A-4 & 5 PVA 10%,3 =( 100) * (PVIFA 10%,3) PVA 10%,3 =( 100)* 2.4869 = PVA 10%,3 = 248.69

INPUTS 3 10 100 0 N I/YR PV PMT FV OUTPUT -248.69 Have payments but no lump sum FV, so enter 0 for future value.

Find the FV and PV if theannuity were an annuity due. 0 1 2 3 10% 100 100 100 Easiest way, multiply results by (1 + i).

Algebraic Solution 1 . PVAD i,n =( PMT)* 1 – (1 + i)n * (1 + i) i 1 . PVAD 10%,3 =( 100) * 1 – (1 + .1)3 * (1 + .1) .1 PVAD 10%,3 =( 100)* 1 - .7513 * (1.1) = .1 100 * 2.48685 * (1.1)= PVAD 10%,3 = 273.55

Tabular Solution PVAD i,n =( PMT) * (PVIFA i,n )* (1 + i) Use Table A-2 on pages A-4 & 5 PVAD10%,3 =( 100) * (PVIFA 10%,3) * (1 + i) PVAD 10%,3 =( 100)* 2.4869 * 1.1 = PVAD 10%,3 = 273.55

Switch from “End” to “Begin.” Then enter variables to find PVA3 = $273.55. INPUTS 3 10 100 0 -273.55 N I/YR PV PMT FV OUTPUT Then enter PV = 0 and press FV to find FV = $364.10.

What is the PV of this uneven cashflow stream? 4 0 1 2 3 10% 100 300 300 -50 90.91 247.93 225.39 -34.15 530.08 = PV

Input in “CFLO” register: CF0 = 0 CF1 = 100 CF2 = 300 CF3 = 300 CF4 = -50 • Enter I = 10, then press NPV button to get NPV = $530.09. (Here NPV = PV.)

The Power of Compound Interest A 20-year old student wants to start saving for retirement. She plans to save $3 a day. Every day, she puts $3 in her drawer. At the end of the year, she invests the accumulated savings ($1,095) in an online stock account. The stock account has an expected annual return of 12%.

How much money by the age of 65? 45 12 0 -1095 1,487,261.89 INPUTS N I/YR PV PMT FV OUTPUT If she begins saving today, and sticks to her plan, she will have $1,487,261.89 by the age of 65.

How much would a 40-year old investor accumulate by this method? 25 12 0 -1095 146,000.59 INPUTS N I/YR PV PMT FV OUTPUT Waiting until 40, the investor will only have $146,000.59, which is over $1.3 million less than if saving began at 20. So it pays to get started early.

How much would the 40-year old investor need to save to accumulate as much as the 20-year old? 25 12 0 1487261.89 -11,154.42 INPUTS N I/YR PV PMT FV OUTPUT The 40-year old investor would have to save $11,154.42 every year, or $30.56 per day to have as much as the investor beginning at the age of 20.

Will the FV of a lump sum be larger or smaller if we compound more often, holding the stated I% constant? Why? LARGER! If compounding is more frequent than once a year--for example, semiannually, quarterly, or daily--interest is earned on interest more often.

Rules for Non-annual Compounding 95% of the time, the method for adjusting for non-annual compounding is: Divide i by m, m being the # of compounding periods in a year. Multiply n by m

FV of $100 after 3 years under 10% semiannual compounding? Quarterly? m*n i æ ö Nom FV = PV 1 . + ç ÷ è ø n m 2*3 0.10 æ ö FV = $100 1 + ç ÷ è ø 3S 2 = $100(1.05)6 = $134.01. FV3Q = $100(1.025)12 = $134.49.

0 1 2 3 10% 100 133.10 Annually: FV3 = $100(1.10)3 = $133.10. 0 1 2 3 4 5 6 0 1 2 3 5% 100 134.01 Semiannually: FV6 = $100(1.05)6 = $134.01.

Exam Question (Example) Your uncle has given you a choice between receiving $20,000 today on your 18th birthday, or waiting until your 25th birthday and receiving $40,000. If you would invest in a junk bond fund if you took the $20,000, expecting to average 10% per year, compounded semiannually, which would you prefer?

Exam Question (Example) See board for timeline. Algebraic solution: FV = PV(1 + i/m)n*m FV = 20,000 (1 + .1/2)7 * 2 FV = 20,000 ( 1.9799) = 39,598.63 Prefer the $40,000 in 7 years.

Exam Question (Example) Tabular solution: PV = FV(PVIF i/2,n*2) PV = 40,000 (PVIF 10/2,7*2) Table A-1 PV = 40,000 ( .505) = 20,202 Prefer the $40,000 in 7 years (same conclusion.

Financial Calculator Solution 14 10 ? 0 40,000 -20,202.72 INPUTS N I/YR PV PMT FV OUTPUT Could have solved for FV inputting PV calcuation: P/Y set to 2

We will deal with 3 different rates: iNom = nominal, or stated, or quoted, rate per year. iPer = periodic rate. EAR = EFF% = . effective annual rate