Download

1 / 34

340 likes | 447 Vues

Explore Plott and Sunder's experiments on insider information, market dissemination, aggregation, and rational expectations hypothesis testing. Analyze information design, cash flows, profit recording, investor types, and efficacy of market mechanisms.

E N D

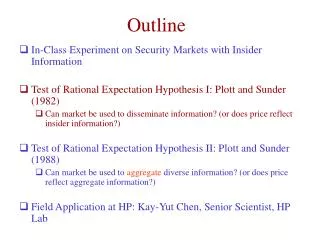

Outline • In-Class Experiment on Security Markets with Insider Information • Test of Rational Expectation Hypothesis I: Plott and Sunder (1982) • Can market be used to disseminate information? (or does price reflect insider information?) • Test of Rational Expectation Hypothesis II: Plott and Sunder (1988) • Can market be used to aggregate diverse information? (or does price reflect aggregate information?) • Field Application at HP: Kay-Yut Chen, Senior Scientist, HP Lab

Dissemination versus Aggregation • Dissemination • Three states: X, Y, Z. • At the beginning of the period, the state was drawn. • If the state was X, then half of the traders were told that the state was X (insiders) and the other half did not receive any clues. • Aggregation • Three states: X, Y, Z. • At the beginning of the period, the state was drawn. • If the state was X, then half of the traders were given that the state was not Y and the other half were told that the state was not Z.

Hypotheses • Prior-Information (PI) Hypothesis (Null): • Expectations are exogenous to the price formation process • Expectations are formed based on prior information • Insiders have an advantage • Rational Expectation (RE) Hypothesis: • Condition expectations on prices • Prices fully reveal state-of-nature q • Insiders do not have an advantage

Urn X and Urn Y: Imperfect Information in Market 1 I I I Urn X Urn Y

Dependent Variables • Price • Allocation • Profits • Efficiency

Price Determination • Expectations formed by either rational-expectation or prior information • Prices are determined by the implied demand and supply schedules in a double auction market mechanism

Profits • PI: Profits of insiders are greater than the profits of uninformed agents • RE: Profits of insiders and the uninformed agents converge to equality

PI versus RE: Allocation Distribution in All Markets • PI and RE make different predictions in 36 out of 61 periods • In 29 out of 36 periods, error from allocations predicted by the RE model is smaller • In 18 out of 36 periods, the RE model made no errors at all. The PI model made zero errors in only 2 out of 36 periods

Efficiency (E) and Trading Efficiency (TE) Getting closer to RE as time progresses

Activity of Insider in the Early Rounds • In four out of 5 markets relative activity of insiders decreases with time. • It seems the competing bids and offers among insiders during the opening stages of a period, reveals the state to the uninformed.