Download

1 / 13

130 likes | 206 Vues

Learn from past financial trends and smart investing strategies to build wealth effectively. Discover asset diversification, investment vehicles, risk management, and wealth-building techniques for long-term prosperity.

E N D

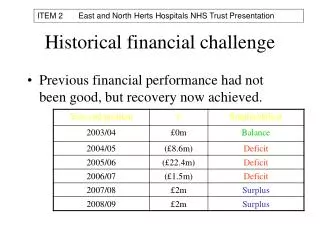

The opinions expressed here are those of Dr. Sutton and do not necessarily represent those of the ECE Department, the Volgenau School, George Mason University, the Commonwealth of Virginia or any other individual, living or dead. My daughter works for Edelman Financial Services. 2000-2010 = worst decade in history (wars, Depression, 12% inflation) Of past 18 decades, 16 were profitable with average 10% per year returns. For the full 18 decades: average return was 8.8% per year. For last 176 years: 130 had positive returns; 46 had negative returns (3:1). 15% of (fewer) negative returns were >20% 32% of (more) positive returns were > 20% 2009: Dropped 25% in first 10 weeks; 63% increase => yearly gain = positive 23%. Smart *investors* ended 2000-2010 “worst decade” with larger portfolios! Some Historical Financial Insights

$340,060 8%/year $266,427 $62,000 $20,000

Determine • Goals (long term; short term) • Annual/monthly income • Annual/monthly expenses (minimum) • Annual/monthly expenses (nice to have) • Savings: (2) – (3 or 4) [till it hurts]

Priorities • 6 to 12 months of expenses (Liquid) • Retirement account • Large goals account (house, car) • Kids college expenses (529 Plan) • Fun

Keys to Wealth building • Compounding • Diversification and Rebalancing • Buy low (during “crash”) • Sell high (on the way up; others are buying) • Consistency

Diversification (of assets) • Capitalization (small, mid, large) • Value (“discounted”) vs Growth (earnings) • International vs Domestic • Emerging vs established markets • Real Estate (not houses!) • Bond and Cash Reserves • Commodities, natural resources, gold, oil

Rebalancing and “Big Picture” • Stocks decrease rapidly; bonds stable • Sell bonds; buy stocks • Large caps increased; small caps decreased • Sell Large caps; buy small caps • Always look at *all* assets: retirement (yours/spouse) + non-retirement

Investment Vehicles (Retirement) • 401(k)/403(b)/TSP [pre-tax = “deductable”] • IRA–traditional – deductable (taxed at withdrawal) • IRA – traditional – non-deductable (don’t) • IRA – Roth (taxed investment $$; not taxed at withdrawal) • 401(k) – Roth • Annuity = “insurance”; fixed/variable; (don’t) • Tax deferred • Locked in till ~age 60 [Do not borrow] • Do not invest (all) in your company stock. Enron!

Investment Vehicles (“Taxable”) • Bank/Credit Union/Savings Account (inflation risk) • CD (inflation risk) • Fixed Income/Money Market (inflation risk; short term) • Stocks (individual; picking takes time and experience) • Bonds (US, state, municipal, company; interest rate risk) • Mutual Funds (~10%/year; long term; “market” risk) • Equity/Bond • Exchange Traded Funds (ETF) (? ~10%/year; long term) • Equity/Bond

Resources • ricedelman.com (and Ric Edelman books) • GPS (Guide to Portfolio Selection) • Jump$tart Coalition jumpstart.org • American Savings Education Council choosetosave.org/asec • National Endowment for Financial Education nefe.org

Investment Risk • Highest: Gold; Emerging Markets; Hedge;Penny • Higher: International Stock Funds; Growth Stocks; Blue Chip; High Yield Bonds; Equity Income Funds • Moderate: Common Stock; Corporate Bonds; Mutual Funds; ETF • Low: CD; US Bonds

Insurance • Health • Disability Income (Long term “can’t work”) • Long Term Care ($50K/year; do while “young”) • Life (Term vs Whole Life) • Renters/Home (Property and liability) • Umbrella (cheap liability)

Bits-n-pieces • Mortgage = loan with property as collateral • Always keep a large mortgage. Do not pay it off. • Changing jobs? Rollover 401(k) into IRA • Employer matching your contribution? Irrelevant! Contribute! • Credit cards: “old” is good • Credit Score: Pay on time; Have long term active credit cards; Watch total balance/total limit ratio; Have a loan record. • Rule of 72 => doubling