Current Asset Management

Current Asset Management. 7. Chapter Outline. What is current asset management Cash management and its importance Management of marketable securities Accounts receivable and inventory management Inventory management and policy decisions required Liquidity vis-à-vis returns.

Current Asset Management

E N D

Presentation Transcript

Chapter Outline • What is current asset management • Cash management and its importance • Management of marketable securities • Accounts receivable and inventory management • Inventory management and policy decisions required • Liquidity vis-à-vis returns

Cash Management • Financial managers actively attempt to keep cash (non-earning asset) to a minimum • It is critical to have sufficient cash to assuage emergencies • Steps to improve overall profitability of a firm: • Minimize cash balances • Have accurate knowledge of when cash moves in and out of the firm

Reasons for Holding Cash Balances • Transactions balances • Payments towards planned expenses • Compensative balances for banks • Compensate a bank for services provided rather than paying directly for them • Precautionary needs • Emergency purposes

Cash Flow Cycle • Ensure that cash inflows and outflows are synchronized for transaction purposes • Cash budgets is a tool used to track cash flows and ensuing balances • Cash flow relies on: • Payment pattern of customers • Speed at which suppliers and creditors process checks • Efficiency of the banking system

Cash Flow Cycle (cont’d) • Cash inflows are driven by sales and influenced by: • Type of customers • Customers’ geographical location • Product being sold • Industry • When the cash balance increases, the extra cash can be • Used for various payments to lenders, stockholders, government, etc • Used to invest in marketable securities • When there is a need for cash a firm can: • Sell the marketable securities • Borrow funds from short-term lenders

E-commerce and Sales • Benefits: faster cash flow • Credit card companies advance cash to the retailer within 7–10 days against retailer’s with a 30 day payment terms • Financial managers must pay close attention to the percentage of sales generated: • By cash • By outside credit cards • By the company’s own credit cards

Float • Difference between firm’s recorded amount and amount credited to the firm by a bank • Two types of float: • Mail float: Arises duet to the time it takes to deliver a check. • Clearing float: Arises due to the time it takes to clear a check once the payment is made • Both these floats do not exist anymore due to: • Electronic payments • Check Clearing for the 21st Century Act • Check Clearing for the 21st Century Act (Check 21) • Allows banks and others to electronically process a check

Improving Collections and Extending Disbursements • Improving collection: • Setting up multiple collection centers at different locations • Adopt lockbox system for expeditious check clearance at lower costs • Extending disbursement: • General trend: • Speedup processing of incoming checks • Slow down payment procedures • Extended disbursement float – allows companies to hold onto their cash balances for as long as possible

Cost-Benefit Analysis • Allows companies to analyze the benefits, received by investing on an efficiently maintained cash management program

Electronic Funds Transfer • Funds are moved between computer terminals without the use of a ‘check’ • Automated clearinghouses (ACH): Transfers information between financial institutions and between accounts using computer tape • International fund transfer is carried out through SWIFT (Society for Worldwide Interbank Financial Telecommunications) • Uses a proprietary secure messaging system • Each message is encrypted • Every money transaction is authenticated by a code, using smart card technology • Assumes financial liability for the accuracy, completeness, and confidentiality of transaction

International Cash Management • Factors differentiating international cash management from domestic based systems: • Differing payment methods and/or higher popularity of electronic funds transfer • Subject to international boundaries, time zone differences, currency fluctuations, and interest rate changes • Differing banking systems and check clearing processes • Differing account balance management and information reporting systems • Cultural, tax, and accounting differences

International Cash Management (cont’d) • Financial managers try to keep as much cash as possible in a country with a strong currency and vice versa • Sweep account: • Allows companies to maintain zero balances • Excess cash is swept into an interest-earning account

An Examination of Yield and Maturity Characteristics • Marketable securities

Marketable Securities • When a firm has excess funds, it should be converted from cash into interest-earning securities • Types of securities: • Treasury bills: Short-term obligations of the government • Treasury notes: Government obligations with a maturity of 1-10 years • Federal agency securities: Offerings of government organizations • Certificate of deposit: Offered by commercial banks, savings, and other financial institutions • Commercial paper: Represents unsecured promissory notes issued by large business organizations • Banker’s acceptances: Short-term securities that arise from foreign trade

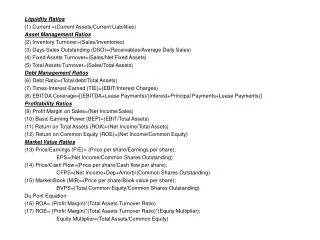

Management of Accounts Receivable • Accounts receivable as an investment • Should be based on the level of return earned equals or exceeds the potential gain from other investments • Credit policy administration • Credit standards • Terms of trade • Collection policy

Credit Standards • Determine the nature of credit risk based on: • Prior records of payment and financial stability, current net worth, and other related factors • 5 Cs of credit: • Character • Capital • Capacity • Conditions • Collateral

Credit Standards (cont’d) • Dun & Bradstreet Information Services (DBIS): • Produces business information analysis tools • Publishes reference books • Provides computer access to information • The Data Universal Number System (D-U-N-S) is a unique nine-digit code assigned by DBIS to each business in its information base

Terms of Trade • Stated term of credit extension: • Has a strong impact on the eventual size of accounts receivable balance • Creates a need for firms to consider the use of cash discounts

Collection Policy • A number if quantitative measures applied to asses credit policy • Average collection period • Ratio of bad debts to credit sales • Aging of accounts receivable

An Actual Credit Decision Accounts receivable = Sales = $10,000 = $1,667 Turnover 6 • Brings together various elements of accounts receivable management

Inventory Management • Inventory has three basic categories: • Raw materials • Work in progress • Finished goods • Amount of inventory is affected by sales, production, and economic conditions • Inventory is the least of liquid assets – should provide the highest yield

Level versus Seasonal Production • Level production • Maximum efficiency in manpower and machinery usage • May result in high inventory buildup • Seasonal production • Eliminates inventory buildup problems • May result in unused capacity during slack periods • May result in overtime labor charges and overused equipment repair charges

Inventory Policy in Inflation (and Deflation) • Inventory position can be protected in an environment of price instability by: • Taking moderate inventory positions • Hedging with a futures contract to sell at a stipulated price some months from now • Rapid price movements in inventory may also have a major impact on the reported income of the firm

The Inventory Decision Model • Carrying costs • Interest on funds tied up in inventory • Cost of warehouse space, insurance premiums, and material handling expenses • Implicit cost associated with the risk of obsolescence and perish-ability • Ordering costs • Cost of ordering • Cost of processing inventory into stock

Economic Ordering Quantity EOQ = 2SO ; C Where, S = Total sales in units O = Ordering cost for each order C = Carrying cost per unit in dollars Assuming: EOQ = 2SO = 2 X 2,000 X $8U = $32,000 = 160,000 C $0.20 $0.20 = 400 units

Safety Stocks and Stock Outs • Stock out occurs when a firm is: • Out of a specific inventory item • Unable to sell or deliver the product • Safety stock reduces such risks • Increases cost of inventory due to a rise in carrying costs • This cost should be offset by: • Eliminating lost profits due to stockouts • Increased profits from unexpected orders

Safety Stocks and Stock Outs (cont’d) • Assuming that; Average inventory = EOQ + Safety stock 2 Average inventory = 400 + 50 2 The inventory carrying costs will now increase by $50 Carrying costs = Average inventory in units × Carrying cost per unit = 250 × $0.20 = $50

Just-in-Time Inventory Management • Basic requirements for JIT: • Quality production that continually satisfies customer requirements • Close ties between suppliers, manufactures, and customers • Minimization of the level of inventory • Cost Savings from lower inventory: • On average, JIT has reduced inventory to sales ratio by 10% over the last decade

Advantages of JIT • Reduction in space due to reduced warehouse space requirement • Reduced construction and overhead expenses for utilities and manpower • Better technology with the development of electronic data interchange systems (EDI) • EDI reduces re-keying errors and duplication of forms • Reduction in costs from quality control • Elimination of waste

Areas of Concern for JIT • Integration costs • Parts shortages could lead to lost sales and slow growth • Un-forecasted increase in sales: • Inability to keep up with demand • Un-forecasted decrease in sales: • Inventory can pile up • A revaluation may be needed in high-growth industries fostering dynamic technologies