Download

1 / 24

240 likes | 380 Vues

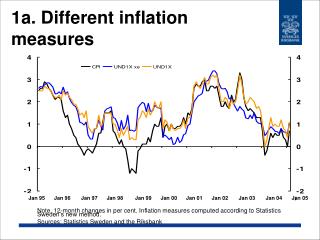

Evaluating alternative measures of Core Inflation for Argentina. Laura D’Amato Juan Sotes Paladino and Lidia Sanz BCRA VIII Annual Seminar, Central Bank of Brazil August 2006. Motivation. Argentina: return to active monetary policy after more than ten years under a hard peg

E N D

Evaluating alternative measures of Core Inflation for Argentina Laura D’Amato Juan Sotes Paladino and Lidia Sanz BCRA VIII Annual Seminar, Central Bank of Brazil August 2006

Motivation • Argentina: return to active monetary policy after more than ten years under a hard peg • Have an adequate assessment of inflation trend crucial for monetary policy decisions • But CPI inflation influenced by transitory movements on relative prices • Core Inflation as a monetary phenomenon (Silver, 2006) • How to separate signal of inflation from temporary noise

Motivation • Problem: dramatic change in RER due to large depreciation of the peso in January 2002 • Change in relative prices rather permanent • Strong initial impact of nominal depreciation on “core inflation” followed by very different paths of tradable and non-tradable goods prices • The cross section distribution of CPI components’ price changes suffered sharp alterations due to abrupt depreciation of the currency

Cross-section distribution of CPI components’ price changes (2002-2004)

Cross-section distribution of CPI components’ price changes (2005-2006)

Cross-section distribution of CPI components’ price changes (2002-2004)

Outline • Core Inflation as a signal extraction problem • Exclusion-based methods • Limited influence estimators • Evaluation • Conclusions

Core Inflation as a signal extraction problem Persistence-based reweighting • Blinder (1997): Core Inflation as the persistent component of CPI • Cutler (2001) reweigh the CPI using persistence based weights • Two weighting vectors: Jan-93/Jan04 and Jan-93/Oct-00

Core Inflation as a signal extraction problem Persistence based reweighting: Results • Food items, usually excluded, have high weight (meat, diary products and eggs) • Regulated Services lose weight due to sporadic changes in prices • Items with high imports component are excluded • Have to revise persistence weights

Core Inflation as a signal extraction problem Volatility-based reweighting • Marques, Neves y Sarmento (2000): weights based on standard deviation of price changes of CPI components relative to mean CPI inflation

Exclusion-based methods Systematic criteria: • Exclude Items simultaneously less persistent and more volatile and according to: • Variance of relative price changes (whole period) • Marginal contribution of each item to the volatility of CPI inflation • Ordering according to Principal Components Analysis

Exclusion-based methods Systematic criteria: Criterion i : 11.7% of CPI components excluded, basically items with high imports component Criteria ii and iii: exclusion of almost all Regulated Services Items (14% of CPI)

Limited influence estimators Brian and Cechetti (1997): • Cross-section distribution of CPI components’ price changes non-normal and with heavy tails • Strong case for the use of robust estimators of the first moment of cross-section distribution • Cross-sectional distribution of 65 components of CPI • Truncate at the 7.5%. 15% and 20% level • Underestimates CPI inflation • Frequency of exclusion informative about volatility of CPI components’ price changes. Can use as exclusion criterion

Evaluation If interested on Core Inflation for prediction: • Granger Causality • Poor results: only volatility-based index performs adequately • Marques et al (2001): Core inflation as an atractor • In Argentina CPI is I(0) • only persistence- based index performs rather well

Conclusions • Persistence and volatility based indicators better performance for prediction • Exclusion indicators and limited influence estimators can be useful to have an assessment of current “core inflation” • Trimmed means probably useful when cross section distribution of price changes is unstable • Correct bias of trimmed means (Silver 2006) • Having more observations of new monetary regime more work needed. • Recalculate persistence weights • Principal component analysis for post-crisis period