Download

1 / 13

150 likes | 395 Vues

This chapter explores the concept of asymmetric information in transactions, where one party holds more information than the other. It discusses two main issues: adverse selection, where informed parties exploit unobserved characteristics (e.g., unhealthy individuals buying life insurance), and moral hazard, where actions of informed individuals change behavior (e.g., insured drivers taking more risks). Screening and signaling methods, such as reputation and product differentiation, are examined as solutions to mitigate the effects of asymmetric information. Additionally, we address how pricing strategies can reflect varying information levels.

E N D

Asymmetric Information Perloff Chapter 19

Asymmetric Information • When two parties to a transaction have different information. • Adverse Selection • When an informed person has an advantage through an unobserved characteristic. • Eg a disproportionately large number of unhealthy people buy life insurance. • Moral Hazard • When an informed person has an advantage through an unobserved action. • An insured car driver drives faster.

Equalising information • Screening • Obtaining information about hidden characteristics. • Insurance. • Costly. • Signalling • Use of public information to indicate the nature of private information. • Restaurant.

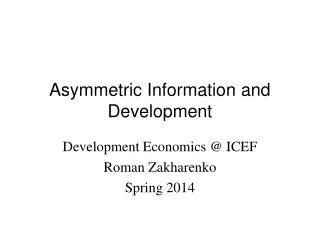

Market for lemons and good cars (a) Market for Lemons (b) Market for Good Cars L S Price of a lemon, $ E Price of a good car, $ G 2,000 D 1,750 2 S f F * 1,500 * 1,500 D D 1,250 1 S e L 1,000 D 750 0 1 ,000 0 1 ,000 Lemons per year Good cars per year

Laws Product liability laws, Consumer screening The use of a mechanic, Reputation, Third party comparisons, ‘Which’ reports, Standards and certification, Kite marks, Signalling by firms Brand names to differentiate product. Preventing the occurrence of lemon markets

Price Discrimination Through Asymmetric Information • Charge a different price according to willingness to pay. • Some consumer’s may falsely believe a product is of a higher quality. • Own label product.

Tourist Trap Model • Pure competitive market: • All firms charge the same price. • A higher price results in zero demand. • Imperfect information in a competitive market. • Know the prices charged by shops but not specific price charged by a specific shop. • Competitive price is p*. • Firm can charge p*+e. • e is less than cost of finding another shop.

Monopoly price in a ‘tourist trap’ • Suppose all firms charge p*+e • Same reasoning implies all firms can raise price to p*+2e • This argument can continue to be applied until all firms charge the monopoly price. • At this price further price increases result in a loss of profit. • In a market where finding prices is costly the equilibrium price is the monopoly price. • If firms are allowed to advertise prices so that search costs disappear the competitive price results.

Employee safety with asymmetric information • Employees in safer industries pay lower wages than in unsafe. • Safety statistics are reported at industry levels, not the firm level.

Education as a signal • Low ability people will not graduate. • Have to accept lower unskilled wage. • High ability people will go to college if difference between skilled and unskilled wage exceeds cost of education • Two equilibrea are possible • Pooling • When costs of education exceed the wage differential and everyone is paid the same. • Seperating • When it pays to go to college.

Unique or multiple equilibrea Pooling equilibrium c, Cost per diploma, $ c = w – w 20,000 h l Pooling or separating equilibrium x y 15,000 z 5,000 c = – — — — — 1 q w – w h l Separating equilibrium 0 1 1 1 – – 4 2 , Share of high-ability workers q